Level-Funded or Fully Insured Group Health?

Author: Justin Bishop · May 28, 2026 · 10 min read

If you run a 5-to-50 employee business in Atlanta and you've shopped group health insurance in the last two years, you've probably been quoted on both fully insured and level-funded plans. The carriers and brokers throw the terms around like everyone knows what they mean. Most owners don't.

The short version: fully insured plans charge a fixed monthly premium and the carrier absorbs all claims risk. Level-funded plans look similar on the surface but shift some of the claims risk back to your business — in exchange for a refund if your group's claims come in low. The bet is on your group's health.

For a healthy young workforce in Atlanta, level-funded can save 15-25% per year. For a workforce with a few high-claim members, level-funded can cost more, sometimes much more. The carrier's quote alone won't tell you which one fits your business — the underlying claims math will.

This post walks through the structural difference, the 2026 cost math for Atlanta groups, when each fits, and the questions every small business owner should ask before signing.

I'm Justin Bishop, an independent broker in Atlanta. I quote level-funded and fully insured plans for Georgia small businesses weekly. Here's the honest breakdown.

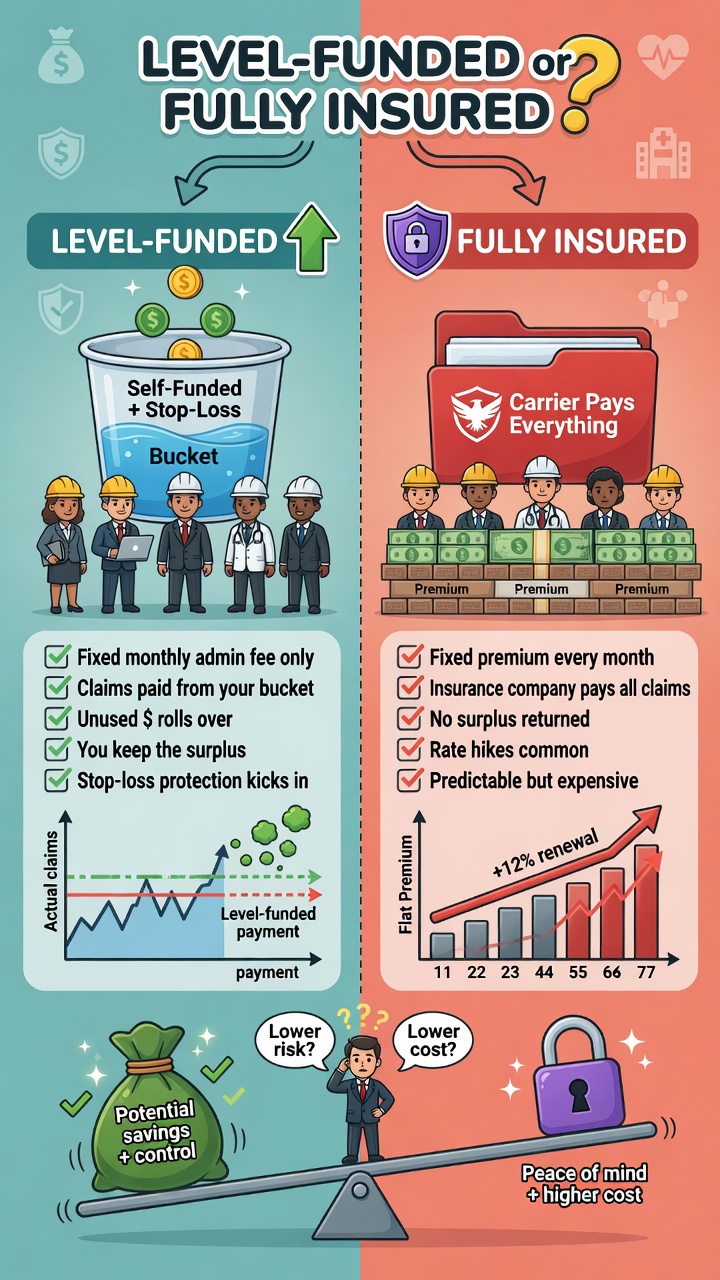

The 30-Second Version

Fully insured: carrier sets the premium, keeps all claims risk. Predictable monthly cost. Renewal increases depend on the carrier's whole risk pool, not just yours.

Level-funded: business pays a level monthly amount, but it's split into claims fund + stop-loss insurance + admin fees. If claims come in under projection, you get a refund. If they come in over, stop-loss protects you up to a ceiling.

Tax/regulatory difference: level-funded is technically a self-funded plan with stop-loss. That means it's regulated under ERISA, not Georgia state insurance law — fewer mandates, more flexibility.

Who wins on level-funded: young, healthy workforces (median age under 40), groups with low historical claims, businesses with stable cash flow that can absorb a bad month.

Who wins on fully insured: older workforces, groups with a few known high-claim members, businesses that need 100% predictable monthly costs, businesses with cash flow that can't absorb claim swings.

2026 Atlanta typical pricing: $500-700/month per employee fully insured for a 10-person group; $400-600/month per employee level-funded for the same group if claims stay favorable.

The trap: most Atlanta brokers quote level-funded based on lowest projected cost and don't model the bad-case scenario. The bad case matters.

How Fully Insured Plans Actually Work

A fully insured group health plan is the traditional model. You pay a monthly premium to a carrier (Anthem, UnitedHealthcare, Cigna, Humana, etc.). The carrier handles everything: claims processing, network access, customer service, and the financial risk of paying out medical claims.

The financial structure:

Carrier sets a monthly premium based on the group's age, location, plan design, and industry

Premium is locked for 12 months (with some exceptions for mid-year demographic changes)

All claims, however high they go, are the carrier's responsibility

At renewal, the carrier looks at the broader risk pool and adjusts your premium accordingly

What you pay: the monthly premium, period. No surprise bills, no claims true-up.

What renewal looks like: carriers in Georgia have been issuing 8-15% renewal increases for fully insured small group plans in 2026, regardless of how your specific group's claims performed. You can shop other carriers to find a better rate, but you can't unilaterally bring your renewal down based on your group's good claims year.

Who fully insured plans fit best:

Groups with older average age (45+) where claim probability is higher

Groups with at least one known high-claim member (chronic condition, expecting baby, recent surgery history)

Businesses with tight or seasonal cash flow that need every monthly cost to be predictable

Businesses that don't want to think about claims management or stop-loss math

How Level-Funded Plans Actually Work

A level-funded plan looks like a fully insured plan on the surface — you write one check per month for a steady, predictable amount. The difference is what happens to that check.

Your monthly payment is split into three buckets:

Claims fund: money set aside to pay employee medical claims. This is yours, not the carrier's. If your group has a low-claim month, that money stays in the fund.

Stop-loss insurance premium: protects you against catastrophic claims. There are typically two layers — individual stop-loss (caps your exposure on any one employee's claim) and aggregate stop-loss (caps your exposure on total group claims).

Administrative fees: what the carrier (or third-party administrator) charges to run the plan, process claims, provide network access, etc.

What you pay: the level monthly amount, same as a fully insured plan.

What happens at the end of the plan year: the carrier reconciles the claims fund. If your employees used less healthcare than projected, you get the difference back as a refund — typically 30-60 days after plan year end. If they used more than projected, stop-loss insurance covered the excess and you don't owe anything additional.

The "level" in level-funded means your monthly cash outflow is steady — but the underlying economics are working in your favor (or not) every month.

Who level-funded plans fit best:

Groups with younger average age (under 40) and historically low claims

Workforces in lower-risk industries (professional services, tech, agencies, restaurants with mostly young staff)

Businesses that have enough financial cushion to absorb a bad claims year if it happens (rare, but possible)

Owners willing to engage with claims data quarterly (most carriers provide reporting)

The Atlanta Cost Math for 2026

Here's what real pricing looks like for a typical 10-employee Atlanta group with a 35-year-old average age:

Fully insured Bronze-equivalent plan:

$480-580 per employee per month

10 employees × $530/mo (mid-range) = $5,300/month / $63,600 annually

Locked for 12 months

Renewal could be +8-15% regardless of claims experience

Level-funded Bronze-equivalent plan, same group:

$400-500 per employee per month "level rate"

10 employees × $450/mo (mid-range) = $4,500/month / $54,000 annually

Plus potential refund at year-end if claims come in low

If claims run as projected: level-funded saves $9,600/year vs fully insured.

If claims run 20% under projection: level-funded saves the $9,600 PLUS returns ~$5,000-8,000 in refund. Total savings: $14,600-17,600.

If claims run 20% over projection: stop-loss kicks in and you don't owe additional. You still saved the $9,600 in baseline premium vs fully insured. Net: still ahead.

Where level-funded loses: if your claims projection was wildly off because the carrier underwrote you to a younger profile than your group really is, or if your group experiences claims so concentrated that you didn't hit aggregate stop-loss but spent your full claims fund. In that scenario, level-funded breaks even or slightly behind fully insured.

The honest answer for most healthy Atlanta small groups: level-funded comes out ahead 70-80% of the time. The other 20-30% of the time it's a wash or slightly behind. The structural risk is real but manageable.

The Tax and Regulatory Difference Most Brokers Don't Mention

Fully insured plans are regulated under Georgia state insurance law. That means:

All Georgia state-mandated benefits apply (specific coverage requirements, network adequacy rules, etc.)

Premium tax of about 2.25% in Georgia is built into the cost

Subject to state rate review

Level-funded plans are technically self-funded plans with stop-loss insurance attached. That means they're regulated under ERISA (federal) rather than Georgia state law. The practical effects:

Exempt from many state mandates — some Georgia-mandated benefits don't have to be included, giving you a slightly leaner plan design

No state premium tax on the claims fund portion (only on the stop-loss premium)

More plan design flexibility — can customize cost-sharing in ways fully insured plans can't

Different appeal process if a claim is denied (federal ERISA process vs Georgia state)

For most small business owners, the ERISA vs state regulation difference is invisible. But it does mean level-funded plans typically have slightly more flexibility in plan design — a Bronze-equivalent level-funded plan might offer benefits or cost-sharing structures that aren't available on the matching fully insured plan.

What Carriers Offer Level-Funded in Georgia for 2026

The level-funded landscape in Georgia changed significantly in 2024-2026. As of 2026, the main carriers offering level-funded plans to small Atlanta groups are:

Anthem Blue Cross Blue Shield of Georgia — strongest network, level-funded available at 2-100 employee group size

UnitedHealthcare — competitive level-funded products, especially for tech and professional services

Cigna — level-funded available with All Savers product

Aetna — level-funded available, narrower in some Atlanta ZIP codes

Allstate Benefits (formerly National General) — competitive on price, smaller network

Trustmark — niche level-funded carrier with flexible plan design

Each carrier has different stop-loss layers, different refund timing, and different underwriting appetites. A 12-person agency in Buckhead will get materially different quotes from each carrier — and the cheapest quote isn't always the best.

For the carrier-level breakdown of the ACA-compliant fully insured menu in Georgia, see Best Georgia Small Group Health Insurance Carriers for 2026

How to Actually Choose

The decision flow I walk Atlanta clients through:

Question 1: What's your group's average age?

Under 35 → level-funded is usually the right answer

35-45 → level-funded if claims history is clean, fully insured if not

45+ → fully insured usually wins unless you have specific reason to think your group is healthier than average

Question 2: Do you have any known high-claim members?

Yes (chronic condition, recent major medical event, expecting baby) → fully insured. The certainty matters more than the savings.

No → level-funded is on the table

Question 3: Can your business absorb a bad claims year?

Yes (cash reserves, profitable, stable cash flow) → level-funded is fine even in bad case

No → fully insured. Predictability is worth the premium.

Question 4: How much do you care about administrative simplicity?

"I want to write one check and never think about it" → fully insured

"I'm willing to look at quarterly claims reports if it saves real money" → level-funded

Question 5: Have you compared the actual quotes side by side? This is where most brokers shortcut the process. They quote one product and stop. Getting both fully insured and level-funded quotes from at least 3 carriers each gives you the real picture.

Common Mistakes Atlanta Small Business Owners Make

Patterns I see when reviewing competitor quotes:

Picking level-funded based on lowest projected cost without modeling the bad-case scenario. The carrier's projection assumes "average" claims for your demographics. If your group's actual claims run hot, you can spend your full claims fund without hitting aggregate stop-loss. Always ask for the bad-case modeling.

Not asking about individual stop-loss levels. Individual stop-loss caps your exposure on any one employee's claim. A $50,000 individual stop-loss means one employee's high-cost year doesn't break the fund. Levels typically range $25K-$100K and the difference is material.

Letting the carrier auto-renew level-funded without re-shopping. Just like fully insured, level-funded plans should be shopped at renewal. Carriers know which clients are passive and price accordingly.

Switching from level-funded to fully insured at the wrong time. If you have a bad claims year on level-funded, the temptation is to flip back to fully insured at renewal. But the next year's fully insured premium will be priced off your now-known claims, often higher than it would have been if you'd never gone level-funded.

Ignoring the refund timing. Level-funded refunds typically come 30-60 days after plan year end. Plan your cash flow accordingly.

Comparing only premium and ignoring plan design differences. A "Bronze level-funded" plan and a "Bronze fully insured" plan from the same carrier can have different deductibles, OOP maxes, and network depth. Compare apples to apples.

Forgetting workers' comp is separate. Whichever group health route you pick, workers' comp is required in Georgia at 3+ employees and is not bundled with either plan type.

Frequently Asked Questions

Is level-funded the same as self-funded? Technically level-funded IS self-funded — but with stop-loss insurance attached and a "level" monthly payment structure. True self-funding (for larger groups, typically 100+ employees) means you pay claims as they come in with no stop-loss, which carries materially more risk than level-funded.

What happens to the refund if I switch carriers next year? The refund still belongs to you. If claims came in low this plan year, the refund is paid out 30-60 days after plan year end regardless of whether you renewed with that carrier or switched.

Can my employees tell the difference between level-funded and fully insured? Usually no. They use the same ID card, the same network, the same claims process. The structural difference is between you and the carrier, not between your employees and their care.

Do level-funded plans have COBRA? Yes. Both plan types are subject to federal COBRA (for employers with 20+ employees) and Georgia Mini-COBRA (for smaller employers). The mechanics of keeping former employees on group coverage are the same.

Can I offer level-funded to some employees and fully insured to others? No — the plan structure applies to the whole group. You can offer different plan tiers (Bronze, Silver, Gold) within either structure, but not mix the underlying funding model.

How long does setup take? Most carriers can implement either plan type with 30-45 days notice before the plan effective date. Mid-year transitions are possible but uncommon — most groups renew on a January 1 or July 1 cycle.

What if my business is 2-4 employees? Level-funded is typically only available at 5+ enrolled employees. Smaller groups are usually fully insured, or look at ICHRA as a third option.

Does the broker get paid differently on the two plan types? Broker commission structures vary by carrier and plan, but most independent brokers (myself included) earn similar commissions on either type. The right plan for your business shouldn't be influenced by what pays the broker more.

The Bottom Line

Level-funded group health plans save Atlanta small businesses 15-25% per year when claims run as projected or better — which happens 70-80% of the time for healthy, younger workforces. When claims run hot, stop-loss insurance protects you from catastrophic exposure, but you can still end up break-even or slightly behind fully insured.

If neither level-funded nor fully insured fits your business profile, ICHRA is the third path. See Should My Atlanta Small Business Switch to ICHRA in 2026? for the audit framework

Fully insured plans cost more on a typical month but eliminate all surprises. For older workforces, groups with known high-claim members, or businesses with tight cash flow, that predictability is worth the premium.

The right answer depends on your group's actual demographics, claims history, financial position, and risk tolerance — not on which product the first broker who called you happens to lead with. Getting both quotes from at least 3 carriers is the only way to see the real picture.

If you want a side-by-side comparison for your specific situation — including bad-case modeling and stop-loss layer analysis — book a 15-minute call with me. I'll quote both products from multiple carriers, model the scenarios, and tell you which one actually fits your business. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out Can a 2-Person LLC Get Group Health?, What Does Group Health Insurance Cost in Atlanta in 2026?, or Do I Have to Provide Health Insurance to My Employees in Georgia? — all parallel small business decisions.

For tech startups specifically, see What Health Insurance Should Atlanta Tech Startups Offer? — covers the private medically underwritten alternative most PEOs don't quote.

"For law firms specifically, see What Health Insurance Should Atlanta Law Firms Offer? — the hybrid approach often beats either pure level-funded or pure fully insured.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not tax, legal, or financial advice. Group health plan structures, carrier underwriting criteria, stop-loss levels, and ERISA compliance rules change.