My Employee Just Quit. How Long Do They Stay on Group Health?

Author: Justin Bishop · May 10, 2026 · 7 min read

It happens to every Atlanta small business eventually: an employee resigns, gets fired, or has their hours cut. The first practical question that comes up — usually within 24 hours — is "how long do they stay on our group health plan, and what do we have to do about it?"

The answer depends on three things: how many employees you have, what kind of separation event triggered it, and whether the employee elects continuation. The rules are different for businesses with 20+ employees (federal COBRA) versus businesses with 2-19 employees (Georgia Mini-COBRA), and there's also a marketplace alternative most former employees would actually be better off using.

I'm Justin Bishop, an independent broker in Atlanta. Small business owners ask me this question weekly. Here's the honest, practical breakdown.

The 30-Second Version

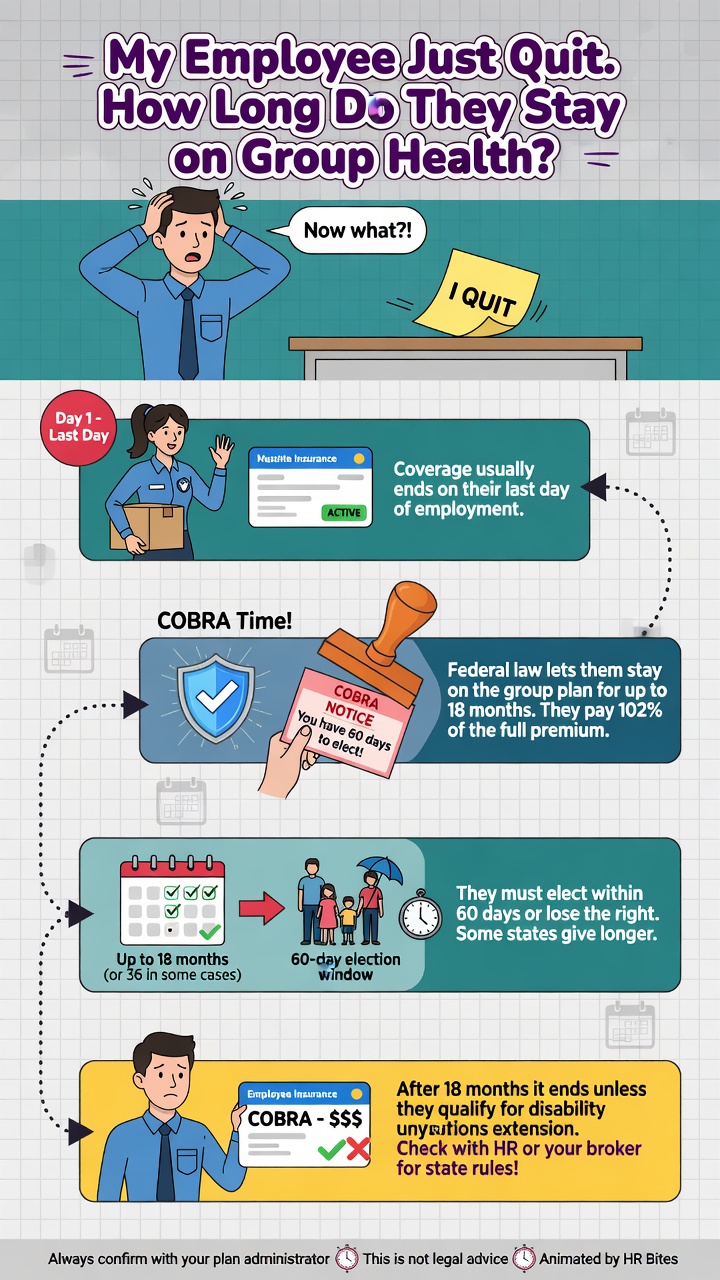

If you have 20+ employees: Federal COBRA applies. The departing employee can stay on the plan for up to 18 months at the full premium plus a 2% admin fee. You're required to offer it.

If you have 2-19 employees: Georgia Mini-COBRA applies. The departing employee can stay on the plan for up to 3 months at the full premium plus an admin fee. You're required to offer it if your group plan is fully insured (most are).

In either case, the marketplace is usually a better deal for the former employee. Job loss triggers a 60-day Special Enrollment Period on Georgia Access, often with subsidies that make marketplace coverage 50-80% cheaper than COBRA.

You (the employer) are required to send a written election notice within 14 days of the qualifying event in either case. Skipping this triggers DOL/state penalties.

The cleanest path: send the election notice on time, let the employee decide between COBRA/Mini-COBRA and the marketplace, and stay out of the decision.

Federal COBRA: For Employers With 20+ Employees

The Consolidated Omnibus Budget Reconciliation Act (COBRA) is the federal law that requires employers with 20 or more full-time-equivalent employees to offer continuation coverage when an employee separates.

What COBRA does:

Lets the former employee (and dependents) stay on your group plan for up to 18 months

They pay the full premium plus a 2% administrative fee (you're not subsidizing it anymore)

Coverage is identical to what they had as an employee — same network, same benefits, same deductible

Some qualifying events extend coverage to 29 months (disability) or 36 months (divorce, dependent aging out)

What COBRA actually costs the former employee:

A typical group plan you were splitting 70/30 with the employee suddenly costs them the entire 100% — usually $400-900/month for single coverage, $1,200-2,500/month for family

Most laid-off workers are stunned by the bill the first time they see it

What you (the employer) have to do:

Notify the carrier or COBRA administrator within 30 days of the qualifying event

Send a COBRA election notice to the employee within 14 days (44 days if you handle COBRA admin in-house)

Wait for the employee's election (they have 60 days to decide)

If they elect, continue coverage and collect premium payments through your COBRA administrator

Most employers with 20+ employees pay a third-party COBRA administrator $5-15 per employee per month to handle this paperwork. The penalty for failing to send the election notice on time can be $110/day per qualified beneficiary plus IRS excise tax of $100/day. Don't skip this.

Georgia Mini-COBRA: For Employers With 2-19 Employees

Federal COBRA only applies to employers with 20+ employees. For smaller businesses, Georgia has its own state law called Georgia Mini-COBRA (technically codified in O.C.G.A. § 33-24-21.1).

What Georgia Mini-COBRA does:

Lets the former employee stay on your group plan for up to 3 months

They pay the full premium plus an administrative fee (typically 2%)

Applies only if your group plan is fully insured (most small group plans in Georgia are; level-funded and self-funded plans are NOT subject to Mini-COBRA)

Same coverage as their employee policy

What you (the employer) have to do:

Notify the carrier within 14 days of the qualifying event

Send a written notice to the employee informing them of their Mini-COBRA rights

Continue coverage if the employee elects and pays

The 3-month limit is much shorter than federal COBRA's 18 months — by design, because Georgia legislators figured small businesses couldn't reasonably manage longer continuation administratively.

For Atlanta small businesses, Mini-COBRA is mostly a short bridge while the former employee figures out a longer-term coverage solution (usually the marketplace).

The Marketplace Alternative (Why Most Employees Should Skip COBRA)

This is the part most employers don't realize — and it's the single most useful thing you can tell a departing employee.

Job loss triggers a 60-day Special Enrollment Period on the Georgia Access marketplace. During that window, your former employee can enroll in any individual marketplace plan, often with significant premium tax credits if their projected income for the rest of the year qualifies.

For most laid-off Atlanta workers, the marketplace beats COBRA on price by 50-80% because:

COBRA requires paying the full group premium (no subsidy)

Marketplace plans are subsidized based on the new (lower) projected income after job loss

A laid-off worker projecting $30,000-50,000 annual income usually qualifies for substantial subsidies

The full breakdown from the employee perspective: How to Get Health Insurance If I Just Lost My Job.

Your role as the employer: still send the COBRA/Mini-COBRA election notice on time. Don't skip it. But it's perfectly fine — and a kindness to the former employee — to mention that they should also look at marketplace options before electing COBRA.

Qualifying Events Beyond "Quitting"

COBRA and Mini-COBRA aren't just for resignations. Several events trigger continuation rights:

Voluntary quit (the one most owners think of first)

Involuntary termination for any reason except gross misconduct

Reduction of hours that drops the employee below the eligibility threshold (e.g., going from 35 hours/week to 25 hours/week below the 30-hour ACA threshold)

Death of the employee (dependents can elect for up to 36 months under federal COBRA)

Divorce or legal separation (the spouse can elect for up to 36 months under federal COBRA)

Dependent aging out (a child reaching age 26 can elect their own COBRA for up to 36 months)

In all these cases, the qualifying event triggers the employer's notification obligation. The clock starts on the qualifying event date — not on when the employee tells you they want to elect.

What You (the Employer) Have to Do — A Checklist

Within 30 days of the qualifying event:

Notify your group health carrier or COBRA administrator of the qualifying event

Provide the employee's last day of employment, type of qualifying event, and election deadline date

Within 14 days of receiving notice (or 44 days if you administer COBRA in-house):

Send the COBRA election notice to the former employee at their last known address

The notice must include: rights under COBRA, premium amount, election deadline, payment deadline, and contact info for questions

For Mini-COBRA: send a Georgia-specific notice with the 3-month duration explained

After the employee elects (if they elect):

Continue group coverage as long as premiums are paid on time

Collect monthly premium payments through your COBRA administrator

Terminate coverage when the COBRA period ends (18 months federal / 3 months Georgia Mini), the employee stops paying, or they qualify for new group coverage elsewhere

For most Atlanta small businesses, outsourcing COBRA/Mini-COBRA administration to a third-party administrator is worth the $5-15/employee/month. The penalties for missing deadlines or notice requirements are far worse than the admin fee.

Common Employer Mistakes

Patterns I see weekly:

Forgetting to send the election notice on time. $110/day penalty per qualified beneficiary is a real risk. Set a calendar reminder the day the qualifying event happens.

Sending the notice by email only. COBRA notices should be sent via first-class mail (or hand-delivered with signature). Email-only notice doesn't count under federal regulations.

Confusing federal COBRA with Georgia Mini-COBRA. If you have 19 employees, you're under Mini-COBRA, not federal COBRA. Different durations, different notice requirements, different penalties. Know which one applies.

Trying to deny COBRA for "cause" terminations. Federal COBRA only allows denial for gross misconduct — a high bar. Most employer terminations don't qualify. Offer COBRA unless your employment attorney specifically advises otherwise.

Not coordinating with the new carrier if you switch group plans mid-COBRA-period. The COBRA participant's coverage transitions with the new plan. Coordinate with both carriers.

Charging too much for the admin fee. Federal COBRA caps the admin fee at 2% of the premium. Some employers accidentally charge more. Stick to the 2% cap.

Forgetting that Mini-COBRA doesn't apply to self-funded or level-funded plans. If you've moved off a fully insured plan, Mini-COBRA may not be required. Verify with your benefits attorney.

Frequently Asked Questions

What if the employee doesn't pay the COBRA premium on time? Federal COBRA gives a 30-day grace period for late payments. After that, you can terminate coverage and notify the carrier. Document everything.

Can I offer to pay part of the COBRA premium as a severance benefit? Yes — many Atlanta employers do this for involuntary terminations. The employer-paid portion is generally tax-deductible to the business. The premium subsidy can be 30-100% of the COBRA cost for a defined period (typically 1-6 months).

What if my employee quits and immediately starts a new job with new group coverage? COBRA and Mini-COBRA still apply at the qualifying event date — you still owe the election notice. But once the employee enrolls in the new employer's plan, COBRA coverage is no longer needed. The employee can decline COBRA or terminate it once new coverage starts.

Does Georgia Mini-COBRA apply to retirees? Yes — voluntary retirement is a qualifying event. The employee can elect Mini-COBRA for the standard 3-month period. Many retirees use this as a bridge to Medicare if they're 64-and-some-months when they retire.

What's the difference between COBRA and Cal-COBRA / state-specific extensions? Some states (California, Connecticut, New York, etc.) have state laws that extend federal COBRA up to 36 months. Georgia does not have such an extension — federal COBRA in Georgia is 18 months max for most qualifying events.

Can I outsource all of this to my insurance broker? Brokers don't typically administer COBRA — that's a separate function called a COBRA Third-Party Administrator (TPA). Most small business benefits brokers can recommend a TPA. Expect $5-15/employee/month for COBRA admin services.

The Bottom Line

When an employee leaves your Atlanta small business, the practical answer to "how long do they stay on group health?" is:

20+ employees → Federal COBRA, up to 18 months

2-19 employees → Georgia Mini-COBRA, up to 3 months (if your plan is fully insured)

Either way → 60-day marketplace SEP is usually the better deal for the former employee

Your job as the employer is to send the election notice on time, continue coverage if elected, and stay out of the decision-making. The penalties for missing notice deadlines are real — outsource the admin if it's worth $5-15/employee/month to get peace of mind.

If you've just had an employee separation and need help figuring out the right path — for both your business and the former employee — book a 15-minute call with me. I can walk you through the COBRA paperwork, recommend a TPA, and help the departing employee compare COBRA vs marketplace if they want a second opinion.

Want to keep reading? Check out Group Health Insurance for Small Business in Atlanta 2026, Do I Need Group Health Insurance for My Employees?, or How to Get Health Insurance If I Just Lost My Job (the employee-perspective companion to this post).

COBRA mechanics are the same on both level-funded and fully insured plans. The funding-model decision is covered in Level-Funded or Fully Insured Group Health?.

Other Coverage Your Business Needs

Every small business also needs General Liability. See General Liability Insurance for Atlanta Small Businesses for the full breakdown

For the parallel Georgia employer obligation triggered by employee count, see Do I Need Workers' Comp for My Small Business?

"If you're rebuilding your group structure after an employee transition, see Can a 2-Person LLC Get Group Health? for what qualifies.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal, tax, or HR advice. COBRA and Georgia Mini-COBRA rules, notice requirements, and penalties change.