Can a 2-Person LLC Get Group Health?

Author: Justin Bishop · May 25, 2026 · 10 min read

If you run a 2-person LLC in Atlanta — whether it's you and your spouse, you and a business partner, or you and a single employee — and you've been wondering whether you can buy group health insurance instead of individual coverage, the answer is more nuanced than the search results suggest.

The short answer is usually no — but it depends entirely on who counts as the "2." Georgia carriers have a specific rule that determines eligibility, and most 2-person LLCs fail it without realizing why. The good news is that if you don't qualify, there are three real alternatives, and one of them (ICHRA) is genuinely a better fit for many small LLCs than group health would have been.

This post breaks down the three real "2-person LLC" scenarios, the Georgia carrier rule that decides everything, the alternatives if you don't qualify, and the S-Corp tax path that most CPAs handle correctly but some miss.

I'm Justin Bishop, an independent broker in Atlanta. I walk small business owners through this exact decision weekly. Here's the honest breakdown.

The 30-Second Version

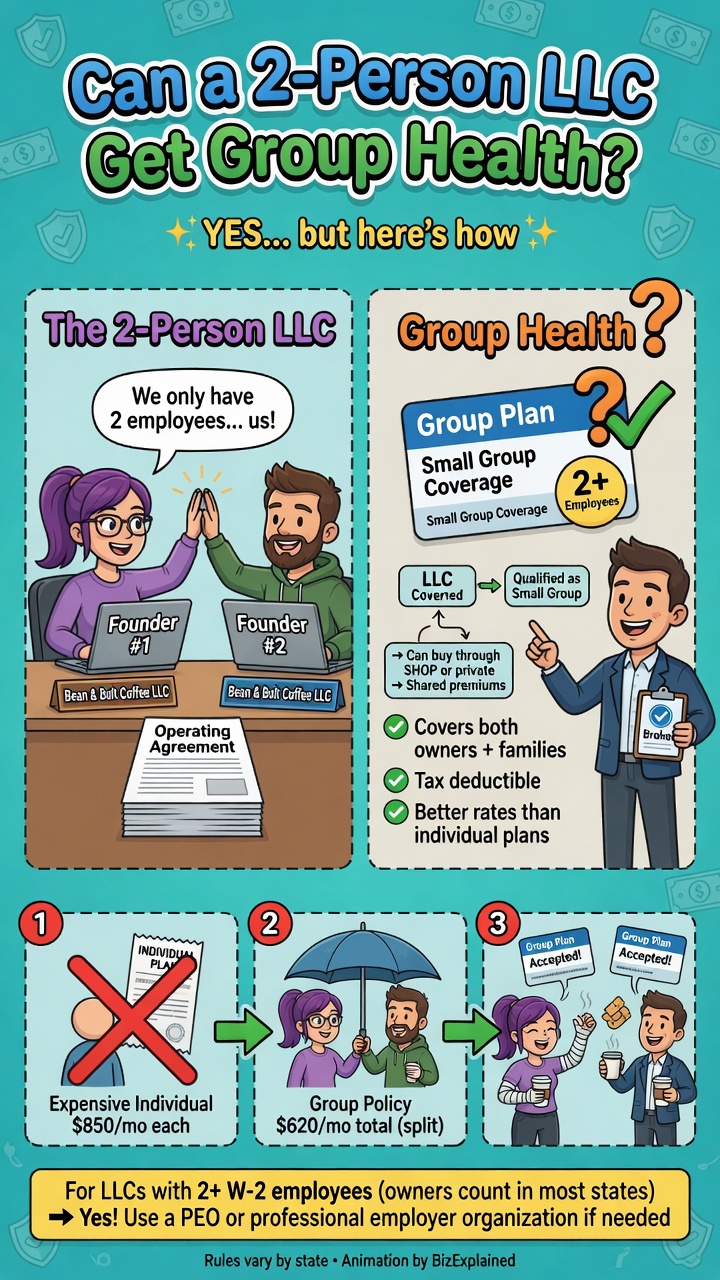

The deciding rule in Georgia: group health requires at least one W-2 employee who is not an owner or an owner's spouse

Owner + spouse on payroll → almost always NOT eligible (carriers treat spouses as owners)

Owner + unrelated W-2 employee → YES, eligible for group health

Two owners, no W-2 employees → almost always NOT eligible

W-2 employee must work 30+ hours/week in most cases, and be a bona fide employee (1099s don't count)

Most cost-effective alternative if you don't qualify: ICHRA — tax-free reimbursement of individual premiums with no annual limit

S-Corp shareholder-employees can deduct premiums in a tax-advantaged way that saves 15.3% on the payroll tax portion

Cheapest mistake: assuming spouses or 1099s count toward group eligibility — they don't

What "2-Person LLC" Actually Means (and Why It Matters)

When someone asks me "can my 2-person LLC get group health?" they usually mean one of these three setups:

Setup A: Husband and wife each on payroll, no other employees

Setup B: One owner plus one unrelated W-2 employee

Setup C: Two unrelated business partners, both owners, no W-2 employees

Carriers treat each one completely differently. The answer to your question depends on which of these you actually have. Most people calling me about this have Setup A or Setup C — and they're surprised by the answer.

Scenario A — Owner + Spouse on Payroll

This is the most common version of the question, and the answer is almost always no in Georgia.

Here's why: under federal law and most carrier rules, a spouse of an owner is considered an owner for group health eligibility. So even though you're each drawing a W-2 paycheck, the carrier sees the application as "one owner-couple, zero W-2 employees" — and rejects it as a group of one.

A handful of states allow spousal group plans under specific carrier products. Georgia is not one of those states for most major carriers. Anthem, Cigna, UnitedHealthcare, and Humana all decline spouse-only groups in Georgia in nearly every case.

Your real options if you're owner + spouse:

Buy individual health insurance for each of you (ACA marketplace or off-exchange)

Set up an ICHRA to reimburse those individual premiums tax-free (often the smartest move — covered below)

Add a non-related W-2 employee, even part-time at 30+ hours, to legitimately qualify as a group

Scenario B — Owner + Unrelated W-2 Employee

This is the version that works. If your 2-person LLC is one owner plus one unrelated W-2 employee working at least 30 hours per week, you qualify as a group for almost every Georgia carrier.

A few rules to know:

The W-2 employee must be bona fide — actually working, actually paid through payroll, with a real role. Carriers occasionally audit, and putting a friend on payroll just to qualify is fraud.

Most carriers require the employee to have worked at least 60 days before the group plan effective date

The employer must contribute at least a minimum percentage of the employee-only premium — usually 50% in Georgia, though some carriers go as low as 25%

The group must enroll at least 70% of eligible employees — easy when you have 2 people and both want coverage; harder if the employee waives because of spouse coverage elsewhere

The benefits of this setup over individual coverage:

Group plans typically have broader networks than individual ACA plans

The employer's contribution to premium is fully tax-deductible for the business

The employee's contribution can be paid pre-tax via a Section 125 cafeteria plan, lowering payroll taxes for both employer and employee

Group plans use age-banded pricing without medical underwriting

Employees can keep coverage even if their personal health changes

Scenario C — Two Owners, No W-2 Employees

This is the partnership setup — two owners splitting equity, no salaried employees outside themselves.

Same answer as Scenario A: usually not eligible. Carriers count two owners as zero W-2 employees, and you don't have a group.

The path forward is the same: individual coverage, ICHRA reimbursement, or hire an unrelated W-2 employee to legitimately qualify.

Why Group Health Is Worth Pursuing (When You Can Get It)

I get asked all the time whether it's even worth the hassle to qualify for a group plan vs. just buying individual coverage. Three reasons it usually is, once you qualify:

Once you qualify for group health, the next decision is funding structure. See Level-Funded or Fully Insured Group Health? for the choice that decides your monthly cost.

Network access. Many Georgia group plans include broader PPO networks than the on-exchange individual plans (Emory, Northside, Piedmont networks are often more accessible)

Tax treatment. Employer contributions are deductible to the business; employee contributions via cafeteria plan lower FICA for both sides

Predictable pricing. Group rates are based on the group's demographics (age-banded), not individual medical underwriting — your premium doesn't spike because someone got diagnosed mid-year

That said, for very small groups (2-5 people), individual coverage with an ICHRA reimbursement often wins on flexibility and sometimes on total cost. Don't assume group is automatically better.

For the full menu of carriers writing 2-50 small group in Georgia for 2026, see Best Georgia Small Group Health Insurance Carriers for 2026

Alternatives If You Don't Qualify

Option 1 — Individual ACA marketplace or off-exchange plans

Each owner (and spouse) buys their own individual health plan. The business doesn't pay anything directly. Each person handles their own coverage, their own subsidy eligibility, their own enrollment.

Best for: Owners with very different ages, very different income brackets, or different medical needs. The flexibility is worth the lack of group buying power.

Option 2 — QSEHRA (Qualified Small Employer HRA)

A QSEHRA lets a small business (under 50 employees) reimburse employees tax-free for individual health insurance premiums and medical expenses. The 2026 limits are roughly $6,350 for self-only coverage and $12,800 for family coverage per year, per employee.

Critical limitation: QSEHRAs cannot include owners. So if you're owner-only or owner+spouse with no W-2 employees, you can't even set one up — there's no employee to reimburse.

Best for: Small businesses with 1-5 W-2 employees who want to offer tax-free reimbursement instead of a group plan.

Option 3 — ICHRA (Individual Coverage HRA) ← often the best answer

This is the most flexible and most underused option for small Atlanta LLCs.

ICHRA lets a business of any size reimburse employees (and owners, with caveats) tax-free for individual health insurance premiums. Unlike QSEHRA, there are no annual reimbursement limits. You set the amount.

If your entity does not qualify for group health, ICHRA is often the right alternative. See Should My Atlanta Small Business Switch to ICHRA in 2026? for the setup framework

Critical rules:

The owner can participate in some entity structures (S-Corp shareholder-employees with W-2 wages can, with limits; sole proprietors and partners generally cannot)

Employees must have actual individual health coverage to be reimbursed

ICHRA classes (e.g., full-time vs. part-time) can be structured to offer different amounts

Best for: Small LLCs that want a benefit infrastructure but don't qualify for or don't want a group plan. The combination of individual coverage + ICHRA reimbursement gives many small businesses 80% of the group experience with more flexibility.

The S-Corp Shareholder-Employee Tax Path

If your LLC is taxed as an S-Corp and you (the owner) take a W-2 wage from the business, you can deduct health insurance premiums in a specific way:

The premium is paid by the S-Corp

It's added to your W-2 wages as Box 1 income (so you pay federal income tax on it)

It's NOT subject to FICA/Medicare (so you save 15.3% on that portion)

You deduct it as a self-employed health insurance deduction on your personal Schedule 1 (so federal income tax is offset)

Net effect: premiums become deductible at the federal income tax level and exempt from payroll tax — a meaningfully better deal than paying premiums with after-tax personal money.

This is a tax structure conversation, not an insurance one. Talk to your CPA before changing how premiums flow through your business. But if you're an S-Corp shareholder-employee, ask specifically about this — many CPAs handle it correctly, some don't.

What to Do If You're About to Hire Your First Employee

If you're 30 days out from hiring your first W-2 employee, you have a real strategic decision to make.

Do you want to offer group health as part of the comp package? It's a major hiring lever, especially in competitive labor markets

Or do you want to reimburse them with an ICHRA? Less commitment, more flexibility, easier to administer

Or do you want to pay a higher cash wage and let them buy their own? Cleanest, simplest, but loses the tax efficiency

The right answer depends on your hiring market, your cash flow, and how long you expect this employee to stay. I help Atlanta small business owners walk through this decision regularly — see Where Do I Get a Business Owner Policy in Atlanta? for the parallel business-insurance setup conversation.

Common Mistakes 2-Person LLCs Make

Patterns I see weekly:

Assuming spouse-on-payroll qualifies you as a group. It doesn't in Georgia. Spouses are owners for this purpose.

Hiring a 1099 contractor and counting them as your group health employee. Carriers will deny the application — 1099s are not employees.

Putting a child or parent on payroll to qualify. Gray area; some carriers will treat them as related-party and decline. Always check with a broker before structuring it.

Defaulting to individual ACA plans without checking ICHRA math. For S-Corp shareholders with kids on the plan, ICHRA can save thousands in payroll and income tax annually.

Not exploring the S-Corp election before buying individual coverage. The shareholder-employee tax treatment is worth meaningfully more than most CPAs proactively bring up.

Setting up a QSEHRA when no W-2 employee exists to receive it. Wasted setup; you needed ICHRA or individual.

Buying group health through a friend's "broker" without comparison shopping. The cheapest carrier rotates annually. The 2024 best carrier rarely stays the 2026 best.

Frequently Asked Questions

My LLC is just me. Can I still get group health insurance? No. A group of one isn't a group. You'd need to buy individual coverage. If you have a 1099 income business, the self-employed health insurance deduction makes premiums tax-deductible — worth talking to your CPA about.

Can I add my spouse to my LLC payroll just to qualify for group health? In Georgia, no. Adding a spouse to payroll doesn't help because carriers still treat them as an owner. The rule that matters is "at least one W-2 employee who is not an owner or owner's spouse."

What if I hire a 1099 contractor — does that count as my W-2 employee for group health? No. 1099 contractors are not employees for group health purposes. The IRS and insurance carriers use different tests, but the answer for group health is the same: you need a real W-2 employee.

How many hours does my W-2 employee need to work to count? Most Georgia carriers require 30+ hours per week. Some carriers will accept 20+ hours under specific group products, but 30 is the safe baseline.

Can I qualify by paying my child or parent a W-2 wage? This is a gray area — some carriers treat a child or parent as a related party and decline. Others allow it. Don't assume; ask a broker before structuring it this way.

What's the difference between QSEHRA and ICHRA? QSEHRA has annual reimbursement limits ($6,350 self / $12,800 family for 2026), is restricted to businesses with under 50 employees, and excludes owners from participating. ICHRA has no annual limits, applies to any size business, and can include certain owner-employees. ICHRA is more flexible — QSEHRA is simpler.

If I qualify with an unrelated W-2 employee, can my spouse and kids be on my group plan? Yes. Once you're a legitimate group with the right employee mix, your spouse and dependents enroll as your dependents on the plan, just like any other employee's family.

Can I use a PEO (Professional Employer Organization) to qualify for group health? Yes — PEOs effectively merge your employees into a larger pooled group, which lets very small businesses access group health. The trade-off is administrative cost (typically 2-12% of payroll) and giving up some HR control. Worth running the math for fast-growing 2-5 person LLCs.

The Bottom Line

A 2-person LLC qualifies for group health in Georgia if one of those two people is an unrelated W-2 employee. Owner-plus-spouse doesn't qualify. Owner-plus-owner doesn't qualify. The W-2 rule is the only thing that matters to the carrier.

If you don't qualify, ICHRA is the most underused alternative — it gives small Atlanta LLCs a tax-advantaged way to fund individual coverage without needing a group plan at all. For S-Corp shareholder-employees, the shareholder-employee deduction stacked with ICHRA is often the most tax-efficient structure.

The right setup depends on your entity structure, your hiring plans, and your cash flow. If you want a personalized recommendation for your specific situation — including whether group, ICHRA, or individual coverage fits best — book a 15-minute call with me. I'll walk through the math for your actual numbers. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out Where Do I Get a Business Owner Policy in Atlanta?, General Liability Insurance for Atlanta Small Businesses, or Do I Need Workers' Comp for My Small Business? — all parallel small business decisions.

industries that benefit from ICHRA" section if mentioned, paste: "Restaurants are the most dramatic example. See What Health Insurance Should Atlanta Restaurants Offer? for the full breakdown

Tech founders scaling beyond founder + 1 should see What Health Insurance Should Atlanta Tech Startups Offer? for the benefit structures that work as the team grows.

Law firm partnerships face their own unique benefit design challenges. See What Health Insurance Should Atlanta Law Firms Offer?

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not tax, legal, or financial advice. Group health eligibility rules, carrier underwriting criteria, QSEHRA/ICHRA limits, and S-Corp tax treatment change.