Do I Have to Get My Employees Insurance in Georgia?

Author: Justin Bishop · May 3, 2026 · 8 min read

If you've hired your first employee in Georgia — or you're thinking about it — somewhere between the W-2 paperwork and the payroll setup you ran into this question: am I legally required to provide health insurance?

Most articles online either say "consult an attorney" (useless) or push you straight into a sales pitch for group health. Neither is what you actually need. You need a clear answer to the legal question first, and then — only if it's relevant — a real conversation about your options.

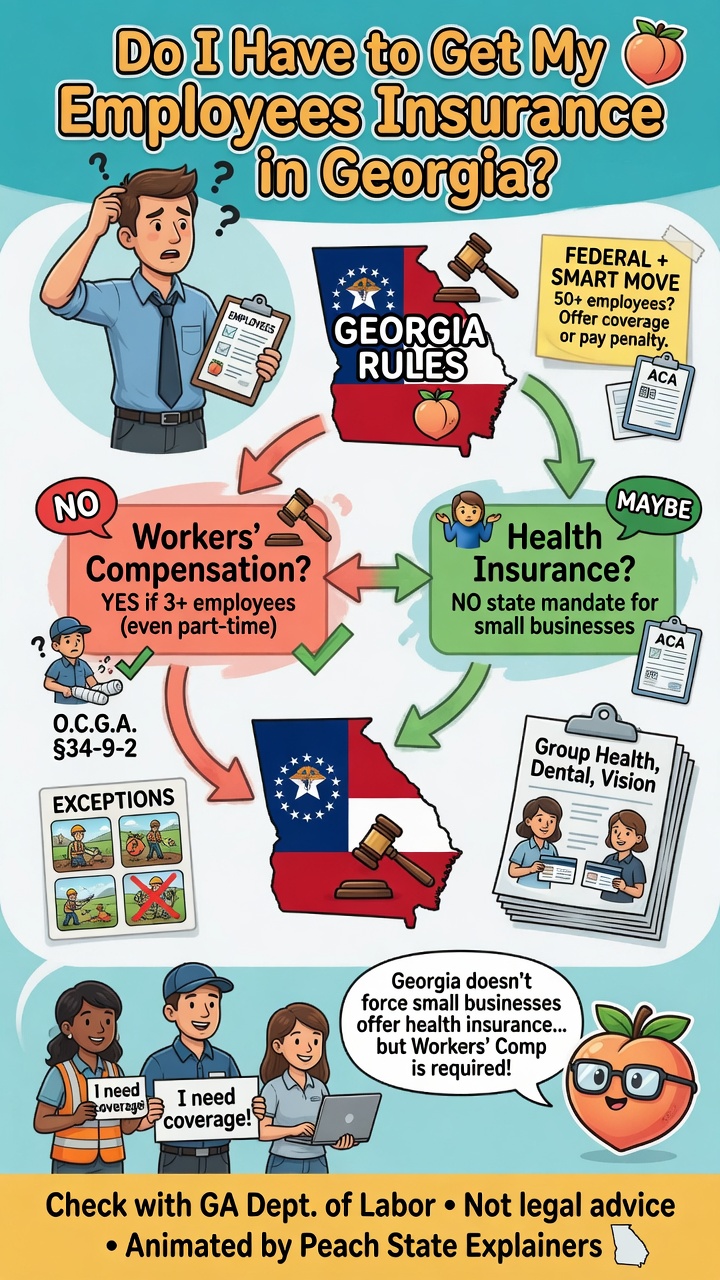

Here's the short version: for most small Atlanta businesses, no, you are not legally required to provide health insurance to your employees in Georgia. The federal employer mandate only kicks in at 50+ full-time employees. Georgia has no separate state mandate. So if you have 1, 5, 10, or 25 employees, you are technically free to offer no health insurance at all.

But "technically free" and "smart business decision" are different things. Most growing Atlanta businesses choose to offer something — and there are now two structurally different ways to do it (traditional group health, or ICHRA reimbursement) that didn't exist as options a few years ago.

I'm Justin Bishop, an independent broker in Atlanta. I write group health and ICHRA setups for small Atlanta businesses every week. Here's the honest framework.

For the broader overview, see Group Health Insurance for Small Business in Atlanta 2026.

The 30-Second Version

Federal law: Required to offer "affordable" health insurance only if you have 50 or more full-time-equivalent employees (the ACA "employer mandate"). Below 50, no federal requirement.

Georgia state law: No additional employer mandate beyond federal. Georgia does not require small employers to offer health insurance.

Workers' comp is different: Required at 3+ employees in Georgia, separate from health insurance.

Two ways to offer health insurance if you choose to: traditional group health insurance (pick a plan, employees enroll) or ICHRA (Individual Coverage HRA — reimburse employees for their own marketplace plans).

Most fitting for 2-15 employee Atlanta businesses: group health if everyone's local, ICHRA if employees are spread across states or want plan choice.

You'll spend either way: $400-$800/employee/month in premiums + setup time. The choice is structure, not whether to spend.

That's the framework. The rest is the detail.

The Legal Answer: Are You Required?

Let's settle this part first.

Federal employer mandate (ACA):

Applies to "Applicable Large Employers" (ALEs) — businesses with 50 or more full-time-equivalent (FTE) employees in the previous calendar year

For restaurants specifically, see What Health Insurance Should Atlanta Restaurants Offer? for the FTE math and ICHRA solution that works.

Counts both full-time and part-time hours to calculate FTEs (30+ hours/week = full-time; part-time hours add up proportionally)

Requires offering affordable, minimum-value coverage to at least 95% of full-time employees and their dependents

Penalty for non-compliance: $2,000-$3,000+ per employee per year, scaling up over time

Below 50 FTEs: no federal requirement at all

For the full COBRA and Georgia Mini-COBRA breakdown after an employee separation, see My Employee Just Quit. How Long Do They Stay on Group Health?.

Georgia state mandate:

None for small employers. Georgia has not enacted a state-level individual or employer mandate beyond the federal ACA framework

No "play or pay" requirement at the state level

No reporting obligations specific to small Georgia employers

What about workers' comp? That's a separate requirement — Georgia law requires workers' compensation insurance at 3 or more employees, not health insurance. Don't conflate them. (See the LLC Insurance Georgia post for the full breakdown.)

So the answer for the vast majority of Atlanta small businesses: legally, no, you don't have to provide health insurance. A 5-person agency, a 12-person restaurant, a 25-person construction crew — none are required by federal or state law to offer health benefits.

When You're Not Required But Probably Should Anyway

The legal answer doesn't mean "don't offer it." Here's when it makes business sense to offer health insurance even when you don't have to:

You're trying to recruit competitive talent. In 2026, employees increasingly expect health benefits even from small businesses. Most candidates ask about it in the first interview.

You're losing employees to competitors who offer benefits. If your turnover is suspiciously high in your industry, benefits gap is often the explanation.

You're paying yourself or co-founders well above market. The owner-employee tax math often favors group health over higher salary — same total comp, less tax liability.

You can deduct premiums as a business expense. What you spend is tax-deductible to the LLC, reducing your taxable business income.

You want stability. Without group benefits, every employee's individual marketplace situation is different — different income projections, different subsidies, different open enrollment confusion. Group health takes that variability off the table.

Retention beats hiring. It costs 3-5x more to replace an employee than to retain one. A $5,000-$15,000/year benefits investment per employee often pays for itself in reduced turnover.

If any of those apply to you, the cost of offering health insurance is usually less than the cost of NOT offering it.

The Two Ways to Offer Health Insurance

If you've decided to offer something, there are now two distinct paths. Picking the right one matters more than picking the right plan within either path.

Path 1: Traditional Group Health Insurance

You pick a single health insurance plan (or 2-3 plan tiers) from a single carrier

All eligible employees enroll in that plan or those tiers

You pay 50%+ of the employee-only premium; employees pay the rest plus dependent coverage

Premium is paid once per month, by the business, to the carrier

Renews annually; you re-shop carriers every year if you want better pricing

Path 2: ICHRA (Individual Coverage HRA)

You set a fixed monthly reimbursement amount per employee (e.g., $500/month)

Each employee buys their own individual marketplace plan that suits them

You reimburse them up to the agreed amount

Reimbursements are tax-free to both employer and employee

Each employee can pick a different plan, network, or coverage level

Both are legitimate. Both are tax-advantaged. Both satisfy "we offer health benefits" for recruiting purposes. They're structurally different.

If you do choose to offer benefits but want flexibility on cost, ICHRA is the modern alternative. See Should My Atlanta Small Business Switch to ICHRA in 2026? for the full framework.

When Traditional Group Health Wins

Group health is the better choice when:

Your team is mostly local to Atlanta or Georgia. Group rating is more efficient when employees can use the same carrier networks.

You have older employees or known health conditions. Group rating averages out the cost across the team; individual marketplace pricing in the same age group can be much higher.

You want a single carrier relationship. One renewal call, one plan to explain at onboarding, one set of provider network rules.

Your team is small (2-10) and price-sensitive. Group plans often beat individual marketplace pricing when the team's age skews older.

You want predictable monthly cost. Group plan = fixed premium per employee, no variability based on what each employee chose.

Full breakdown of group health pricing in Atlanta — covers what real teams pay by size and carrier.

When ICHRA Wins

ICHRA is the better choice when:

Your team is spread across multiple states. Group plans get complicated and expensive across state lines; ICHRA scales nationally because each employee uses their own state's marketplace.

You have a young, healthy team. Individual marketplace pricing rewards younger demographics more than group rating does. A team averaging age 28 often does better through ICHRA than group.

You want employees to have plan choice. Rather than picking one plan for the whole team, ICHRA lets each employee pick what fits them — a single 25-year-old gets a Bronze HDHP, a parent of 3 gets a Gold PPO, etc.

Your team has highly variable preferences. Some employees want low-premium high-deductible; others want low-deductible peace of mind. ICHRA lets each pick.

You want fixed-cost predictability. You set the reimbursement amount; if employees pick more expensive plans, that's their cost. Your monthly outflow per employee is locked in.

You're hiring fast or have variable headcount. Adding a new employee to an ICHRA is faster than adding them to a group plan — they just buy a marketplace plan and you start reimbursing.

The 2026 dynamic: ICHRA is growing faster than traditional group health for small businesses with under-30 average team age and remote/distributed teams. For a co-located older team, group still wins.

The Cost Reality (Both Paths Cost Real Money)

Don't let either path's marketing convince you it's "the cheap option." Both cost roughly the same in total dollars per employee for similar coverage levels. The difference is structural.

Atlanta small business cost reality in 2026:

Group Health (5-person team, mid-tier Silver): ~$700/employee/month total. Employer pays 60% = $420/employee/month. Annual employer cost: ~$25,200 for the team.

ICHRA (5-person team, $500/month reimbursement): ~$500/employee/month employer cost (the reimbursement amount). Annual employer cost: $30,000. Slightly more dollars, but employees can pick plans worth more or less than that depending on their needs.

The hidden ICHRA savings: if an employee qualifies for an ACA premium tax credit on their own, the federal subsidy reduces what they need from your reimbursement. Some businesses set lower reimbursement amounts for younger/lower-paid employees who qualify for big subsidies.

The honest answer: costs are similar. Pick based on team structure (local vs distributed), team age (older vs younger), and your operational preference (one plan vs many).

Common Mistakes I See

The specific mistakes that cost real money or create real problems:

Counting only W-2 employees toward the 50-FTE threshold. Part-time hours add to the FTE count proportionally. A business with 30 W-2 employees plus 40 part-time at 20 hours each can hit ALE status. Run the math properly before assuming you're below 50.

Confusing health insurance with workers' comp. They're separate Georgia requirements with separate rules. Workers' comp at 3+. Health insurance not required for small employers but smart to offer.

Adding family members as "employees" to qualify for group plans. Carriers and the IRS scrutinize. Real W-2s, real wages, real work — or skip group entirely.

Picking ICHRA without realizing employees lose subsidy eligibility. If you offer an ICHRA that's "affordable" by ACA standards, employees can't claim premium tax credits on their own marketplace plans. This may or may not be a net positive depending on income levels — run the math.

Choosing group health for a remote team across many states. You'll either pay carriers for many state networks (expensive) or have employees in some states pay out-of-network rates routinely. ICHRA solves this; group doesn't.

Setting up too late before hiring. A new employee asking "where's my insurance card?" on day one is a bad look. Set up the offering 60 days before you start hiring.

Not communicating with employees about what's offered. Group health vs ICHRA are different employee experiences. Explain what they're getting and how to use it. Most employees will tolerate a less-rich plan if they understand it; they won't tolerate confusion.

How to Decide What Fits Your Business

The 5-question framework:

Are you legally required (50+ FTEs)? If yes, you must offer something. If no, it's a business decision.

Are you trying to recruit/retain talent? If yes, offer something. If no, you can wait.

Is your team local or distributed? Local → group probably fits. Distributed → ICHRA probably fits.

What's your team's age skew? Older → group rating averages out. Younger → ICHRA + individual marketplace often wins.

Do you want one plan or employee choice? One plan → group. Employee choice → ICHRA.

If you've decided to offer something but aren't sure which path, a 15-minute conversation with a broker running both scenarios with your specific numbers usually clarifies it.

Want a Real Comparison for Your Atlanta Business?

If you want both group health quotes AND an ICHRA cost projection for your specific team, the fastest path is to text me at (706) 988-1930 with:

Number of W-2 employees (full-time + part-time)

Rough age range of the team

Where employees are located (Atlanta only, multi-state, remote)

Your sense of monthly budget per employee

I'll come back inside 48 hours with side-by-side comparisons: 2-3 group health quotes from different carriers, plus an ICHRA reimbursement structure analysis with what your employees would actually pay on the marketplace.

You'll see the real numbers for both paths. No pressure, no follow-up sequence.

I write Atlanta small business group health and ICHRA setups every week — agencies, restaurants, professional services, retail, and remote-first companies. Most of my clients want one person who can quote both options and explain the trade-offs in plain English. That's what an independent broker does.

You don't have to buy traditional group. ICHRAs are a real option — here's the breakdown

If you're providing health insurance voluntarily, the funding-model choice matters. See Level-Funded or Fully Insured Group Health?

Other coverage you may need

For the parallel question on Business Owner Policy coverage, see Where Do I Get a Business Owner Policy in Atlanta?

For another Georgia employer obligation triggered by employee count, see Do I Need Workers' Comp for My Small Business?

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn.

This post is general education, not legal or insurance advice. Group health rules, carrier participation, and pricing change.