What Health Insurance Should Atlanta Law Firms Offer?

Author: Justin Bishop · June 2, 2026 · 10 min read

If you're a managing partner at an Atlanta law firm — whether it's a 6-attorney boutique in Buckhead, a 30-attorney mid-size firm with offices in Midtown and Alpharetta, or a 75-attorney regional firm with associates spread across the Southeast — you've probably run into the same set of benefit questions every firm eventually faces.

Your partners take K-1 distributions, not W-2 wages, which complicates how they participate in health benefits. Your associates are W-2 employees who qualify for everything. Your paralegal and administrative staff have different needs from your equity partners. And the firm's culture demands predictable, professional-grade coverage — not the cheapest plan on the market, but not the most expensive either. Sound familiar?

This post walks through the four real benefit structures for Atlanta law firms, why the partnership entity structure changes the math compared to tech startups or restaurants, where private medically underwritten plans win (and where they don't fit), how ICHRA solves the partner-vs-associate eligibility question, real cost math for solo/mid-size/large firm scenarios, and the common mistakes I see managing partners make.

I'm Justin Bishop, an independent broker in Atlanta. I quote benefits for law firms across the metro every week. Here's the honest breakdown.

The 30-Second Version

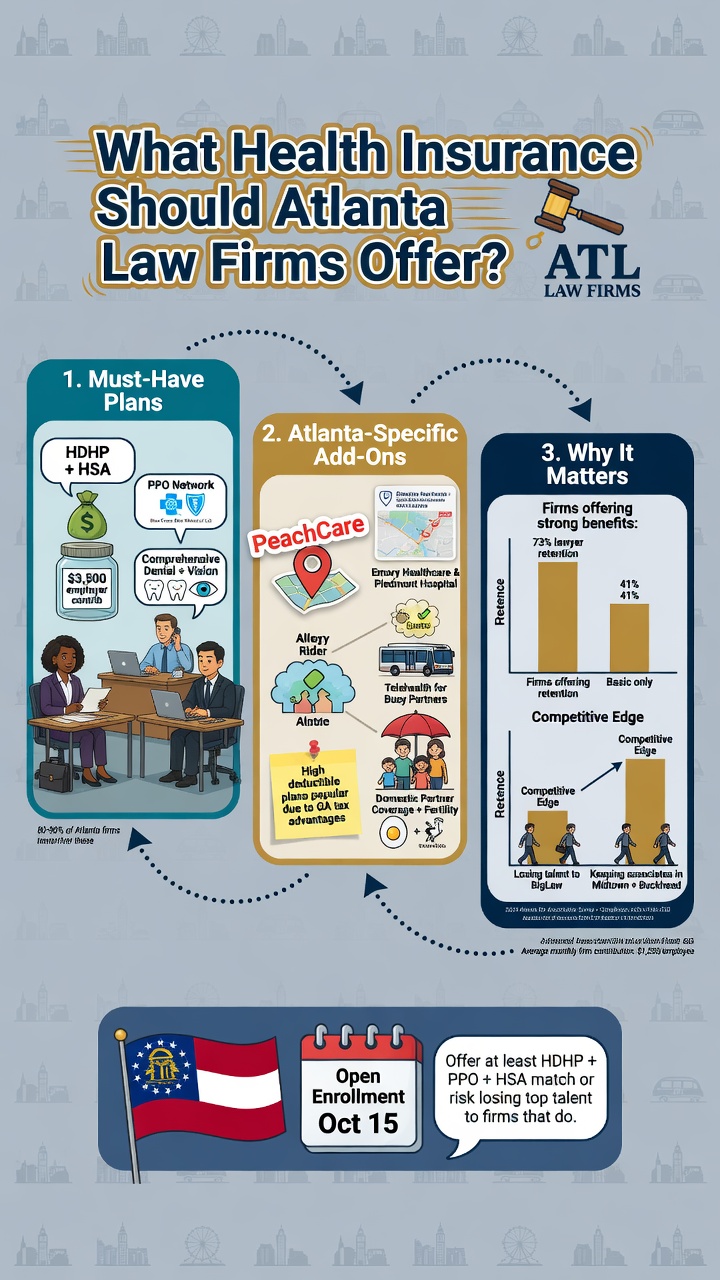

Four real approaches, in order of cost-efficiency for the right firm profile: Private medically underwritten group plans (best when associates and staff skew younger and healthier — typically 15-30% cheaper than ACA-compliant for the right firm; less dramatic than tech startups because lawyers tend to be older) ICHRA (often the right answer — solves the partner K-1 vs associate W-2 eligibility puzzle, works across multiple offices, absorbs hiring across geographies) Traditional ACA-compliant group health (when predictability matters more than cost; common for established firms with stable demographics) Cash stipend (worst tax outcome — avoid)

The partnership tax wrinkle: equity partners taking K-1 distributions cannot participate in group health the same way W-2 associates do. The structure matters enormously for benefit design.

Multi-office or hybrid firms: ICHRA almost always wins because each attorney picks the marketplace plan in their home state/county.

Atlanta law firm typical cost: $450-650/month per enrolled employee for private medically underwritten Bronze-equivalent in 2026; $600-850/month for ACA-compliant fully insured; $500-700/month for ICHRA reimbursements.

Maternity and mental health coverage: non-negotiable for associate retention. Verify these benefits on every quote.

Common mistake: firms structuring benefits around the partners' needs (older, higher-income) and ignoring what works for the associates (younger, family-formation years). Associates are the retention play — design for them.

The right move for most Atlanta law firms: hybrid structure — private medically underwritten group plan for W-2 associates and staff, ICHRA for partners (with K-1-compatible structure), unified by a single broker.

Why Law Firms Have Unique Benefit Challenges

Most industries can use one benefit structure across their whole team. Law firms can't, because the workforce is structurally bifurcated:

Equity partners (K-1 distributions). Owners of the firm. Take draws from partnership profits, not W-2 wages. From the IRS and insurance carrier perspective, they're "self-employed" for benefit purposes. ICHRA eligibility for partners is constrained — they typically cannot participate as employees, though there are specific structures that work.

Non-equity partners and senior associates (W-2 salaries). Treated as employees for benefit purposes. Standard group health eligibility.

Associates (W-2). The bulk of most firms. Standard employees. Often in their late 20s to mid-30s — peak family-formation years.

Paralegals, legal assistants, support staff (W-2 hourly or salaried). Standard employees. Often a mix of ages and family structures.

Of-counsel attorneys. Often 1099 contractors. Generally not eligible for group benefits but eligible for ICHRA only in specific class structures.

The result: a benefit plan that works perfectly for the equity partners may fail to attract or retain associates. A plan that works for associates may shortchange the partners on flexibility. The right structure usually accommodates both.

Other law firm-specific realities:

Older average age than tech startups. Most firms have a meaningful percentage of partners and senior attorneys in their 40s-60s. Private medically underwritten plans still beat ACA-compliant for these groups, but the savings are 15-30% rather than the 25-40% you'd see at a young tech startup.

Maternity coverage is a major retention factor for associates. Most associates have children during their firm tenure. Verify maternity benefits on every quote — some plans have caps or waiting periods that matter.

Mental health coverage is a high-priority benefit. Attorney burnout, depression, and substance use are well-documented industry issues. Strong mental health coverage and EAP access is increasingly seen as table stakes.

Network depth matters more than for tech. Lawyers and their families tend to use a wider range of specialists — orthopedics, fertility, pediatric, mental health. Narrow networks that cost less can backfire on associate satisfaction.

Multi-office firms. Atlanta law firms often have offices in Athens, Augusta, Macon, or remote attorneys in other states. ICHRA fits this geographic spread cleanly.

Continuity matters. Firms don't tolerate annual carrier turnover the way startups do. Partners want a benefit plan they can leave in place for 3-5 years without re-shopping every January.

Approach #1 — Private Medically Underwritten Group Plans (Often the Right Answer for Mid-Size Firms)

This is the option most managing partners haven't seen quoted, because their current broker isn't appointed with the carriers that write these products.

What they are: fully insured group health plans, written by major carriers, that use medical questionnaires during the application process to underwrite the group based on its actual health profile rather than the community-rated ACA pool.

Why it works for law firms (with caveats):

The typical Atlanta law firm has a mixed-age workforce. Senior partners in their 50s-60s drive up the underwriting age. Associates in their late 20s-30s pull it back down. The net result for a 25-attorney firm is typically a workforce that underwrites somewhere between "tech startup" and "established mid-market firm" — meaning private medically underwritten plans still save 15-30% versus ACA-compliant, but not the 25-40% a 6-person SaaS startup might see.

For boutique firms with younger profiles (especially associate-heavy plaintiff firms, criminal defense practices, immigration firms), the savings approach the tech startup range. For older, partner-heavy firms (estate planning, tax controversy, complex litigation), savings shrink.

Carrier landscape in Georgia for 2026:

Allstate Benefits — strong on small-to-mid group medically underwritten, popular with professional services

Trustmark — flexible plan design, 5-100 employee group size, common pick for boutique firms

Allied National — competitive for professional services groups

National General (Allstate) — level-funded with underwriting overlay, fits stable firms

MedCost / certain ACO products — emerging in metro Atlanta

Anthem and UnitedHealthcare — both offer medically underwritten group products at certain sizes, rarely the default quote unless requested

The trade-offs to know upfront:

Pre-existing condition exclusions can apply on some products. Critical for any firm with attorneys managing chronic conditions — verify exclusions match your group profile.

Renewal pricing is more sensitive to claims experience. A bad year (one major surgery or maternity claim) can drive a steeper renewal increase than ACA-compliant.

Some state mandates don't apply. Verify that maternity, mental health, and fertility benefits are at the level your associates need.

Network access varies. Verify Emory, Piedmont, Wellstar, Northside are in-network on the specific product.

Multi-state issues. These plans are state-specific. Remote out-of-state attorneys need ICHRA or parallel coverage.

When private medically underwritten is the clear winner:

8-30 attorney firm with average age under 42

Predominantly W-2 employees (associates and staff)

Single state or single office

No known major chronic conditions in the group

Firm wants to offer competitive coverage without overpaying for ACA-pooled risk

When it's not the right call:

Firm has multiple partners with known chronic conditions (pre-existing exclusions could leave them exposed)

Significant remote/multi-state attorney population

Firm prioritizes the broadest possible benefits set (every state-mandated benefit at maximum levels)

Group is heavily partner-driven and partners can't participate the way W-2 associates can

Approach #2 — ICHRA (Often the Right Answer for Multi-Partner or Multi-Office Firms)

If your firm has a meaningful partnership component, multiple offices, or remote attorneys, ICHRA solves problems that group health structures struggle with.

How it works:

The firm gives each eligible employee a tax-free monthly amount to use toward an individual health insurance plan of their choice. Each attorney or staff member picks any qualifying ACA marketplace plan in their state of residence, submits proof of coverage, and the firm reimburses up to the amount.

Why it fits law firms:

K-1 partners can participate in specific ICHRA structures, where group plans typically can't accommodate them as employees. The partner's contribution gets handled differently from a W-2 employee's, but participation is possible.

Multi-office ready. Attorneys in Atlanta, Athens, Augusta, Macon all use it. Each picks the marketplace plan that works for their location.

Class-based tiering. Different reimbursement amounts for equity partners vs senior associates vs associates vs staff. Within rules, you can structure tiers that reflect the firm's compensation philosophy.

No participation requirements. Each attorney decides individually. Attorneys with spousal coverage can decline; those without are reimbursed.

Easier to manage than group plan renewals. Set the reimbursement amount; let attorneys handle plan selection. Annual review is lighter than group plan re-shopping.

Tax-advantaged for both sides. Reimbursements are tax-free to the recipient and deductible to the firm.

ICHRA reimbursement math for Atlanta law firms in 2026:

Tier 1 (equity partners + executive committee): $700-1,000/month reimbursement

Tier 2 (non-equity partners + senior associates): $550-750/month reimbursement

Tier 3 (associates): $450-650/month reimbursement

Tier 4 (paralegals + admin staff): $400-550/month reimbursement

Part-time under 30 hours: typically excluded

The Atlanta-specific advantage: Atlanta's ACA marketplace has multiple competitive carriers (Anthem, Ambetter, Oscar, UnitedHealthcare, Cigna, Kaiser), so attorneys have real plan choices including PPO options with broad specialist networks.

When ICHRA is the right answer over private medically underwritten:

Multi-partner firm where equity partners need to participate

Multi-office or multi-state attorney population

Older average firm age that doesn't underwrite favorably

Firm has known pre-existing conditions among partners

Managing partner wants predictable per-employee cost rather than community-rated group premium volatility

For the broader ICHRA decision framework across business types, see Should My Atlanta Small Business Switch to ICHRA in 2026?.

Approach #3 — Traditional ACA-Compliant Group Health (When Predictability Matters More Than Cost)

Many Atlanta law firms — particularly older, established firms — default to ACA-compliant fully insured group plans. There are real reasons this works for some firms.

Why some firms prefer it:

Maximum benefit certainty. Every state-mandated benefit, no pre-existing exclusions, no carve-outs.

Predictable renewal cycle. Annual rate increases are smoother than medically underwritten renewals tied to claims experience.

No medical underwriting questionnaires. Attorneys don't fill out health history forms.

Established carrier relationships. Firms with 20+ year carrier relationships sometimes value continuity over savings.

Why it costs more than necessary for many firms:

Community rating means your young associate is priced at the same risk pool as a 60-year-old with three chronic conditions in another company. The cross-subsidy is baked into the premium. For firms with young, healthy associates, this represents real overpayment.

When traditional ACA-compliant is the right call:

Firm has older average age (50+)

Multiple partners with known chronic conditions

Strong preference for ACA's full benefit set and consumer protections

Established carrier relationship the firm wants to keep

Firm doesn't want to administer the medical underwriting process

For the full carrier-by-carrier ranking, see Best Georgia Small Group Health Insurance Carriers for 2026

Approach #4 — Cash Stipend (The Tax Trap)

Some firms, frustrated with rising premiums, offer attorneys an extra $500-700/month and let them buy their own coverage.

Why it's expensive:

Cash stipends are taxable income. That $600/month stipend becomes $600 of W-2 wages. After federal income tax, FICA, and Georgia state tax, the employee nets $400-440 of actual benefit.

The firm pays payroll tax too. That $600/employee/month also triggers employer-side FICA. Total firm cost: $646/month for $400-440 of net employee benefit.

ICHRA delivers the same benefit tax-free. $600 ICHRA reimbursement is worth $600 net to the employee. No payroll tax for the firm. Identical employer outlay, ~35-50% more value to the employee.

Cash stipends don't satisfy the ACA Employer Mandate at 50+ FTE.

If you're going to spend money on attorney health benefits, do it through ICHRA, not cash.

The Partner Eligibility Question (Where Most Law Firm Benefit Designs Break)

This is where most managing partners get the design wrong.

The structural problem:

Equity partners taking K-1 distributions are not W-2 employees for benefit purposes. They cannot participate in a group health plan as an employee with employer contribution and Section 125 cafeteria plan pre-tax treatment. The traditional group health structure was designed for employer/employee relationships, and partners aren't employees in the eyes of the IRS or carriers.

The three real paths:

Partners participate in ICHRA with specific structuring (not as W-2 employees but through the firm's HRA). Tax treatment differs from W-2 associates but participation is feasible. CPA must structure correctly.

Partners buy their own coverage outside the firm structure and deduct premiums via the self-employed health insurance deduction on their personal Schedule 1. Common approach. Loses the bundling discount but is administratively clean.

Partners take W-2 wages from the firm in addition to K-1 distributions (some firms structure this way for benefit purposes). Then they can participate in group health as employees. Tax-inefficient compared to pure K-1 but works.

The right path depends on:

Firm's entity structure (LLP, PC, PLLC, LLC taxed as partnership, etc.)

Partners' personal tax situations

Whether partners want unified coverage with associates or separate plans

This is a CPA conversation as much as a benefits conversation. The wrong structure can cost a managing partner $15K-30K/year in unnecessary tax. Talk to both your CPA and your broker before designing.

Real Atlanta Law Firm Cost Math (2026)

Scenario 1: 6-attorney boutique firm in Buckhead

2 equity partners (ages 48 and 52) + 3 associates (ages 28-35) + 1 paralegal (age 41)

Single office, all in Atlanta

One partner has a controlled chronic condition

Best fit: Hybrid structure

Associates + paralegal (4 enrolled): Private medically underwritten group plan, ~$430/month per enrolled × 4 = $1,720/month

Partners (2): ICHRA at $750/month per partner × 2 = $1,500/month (CPA-structured for K-1 compatibility)

Firm pays 100% of employee-only premium for associates/staff

Total monthly cost: $3,220 ($38,640/year)

Compared to full ACA-compliant fully insured group covering everyone: saves ~$15,000-20,000/year

Compared to traditional all-firm group with partners buying separate: similar cost, better partner experience

Scenario 2: 30-attorney mid-size firm with offices in Midtown and Alpharetta

8 equity partners + 4 non-equity partners + 14 associates + 4 paralegals/admin

Mixed ages 28-65, 2 partners with chronic conditions

Two physical offices in Georgia

Best fit: Hybrid structure

Non-equity partners + associates + staff (22 enrolled): Private medically underwritten group plan, ~$480/month per enrolled × 22 = $10,560/month

Equity partners (8): ICHRA at $850/month per partner × 8 = $6,800/month

Firm pays 100% of employee-only premium for non-equity/staff; partners structure handles itself

Total monthly cost: $17,360 ($208,320/year)

Compared to traditional ACA-compliant fully insured group across the firm: saves ~$45,000-70,000/year

Includes maternity and full mental health coverage for associates (critical retention factor)

Scenario 3: 75-attorney regional firm, multi-state

18 equity partners + 12 non-equity partners + 30 associates + 15 paralegal/admin

Offices in Atlanta, Charleston, Nashville; some remote attorneys

75+ FTE → ACA Employer Mandate applies

Mixed ages, mixed health profiles

Best fit: Full ICHRA structure (single mandate-compliant approach across all states)

Tiered ICHRA: equity partners $900/month, non-equity partners $700/month, associates $600/month, staff $475/month

Total monthly: (18 × $900) + (12 × $700) + (30 × $600) + (15 × $475) = $16,200 + $8,400 + $18,000 + $7,125 = $49,725 ($596,700/year)

Compliance reporting (Form 1095-C) handled by ICHRA TPA

Compared to traditional ACA-compliant + separate partner coverage: saves ~$80,000-120,000/year

All attorneys regardless of state get marketplace plan choice in their state

Hybrid alternative for Scenario 3: Private medically underwritten group plan for Atlanta-based associates + staff (eligible 35 employees, ~$17,500/month), ICHRA for partners and remote/multi-state (40 employees, ~$26,400/month) = $43,900/month / $526,800/year. Saves another ~$70K/year if the Atlanta team underwrites favorably.

Common Mistakes Atlanta Law Firms Make

Patterns I see at managing-partner-level benefit reviews:

Designing benefits around the partners' needs. Equity partners' needs are very different from associates'. Associates are your retention play; design for them too.

Treating partners as W-2 employees in benefit design. K-1 partners are not employees for benefit purposes. Structuring the plan wrong creates tax issues and compliance gaps.

Defaulting to ACA-compliant without exploring private medically underwritten. Even with older average age, most firms save 15-25% by underwriting. Worth the medical questionnaires.

Cutting maternity coverage to save money. Associates plan family formation during firm tenure. Weak maternity coverage hits retention directly.

Underestimating mental health coverage importance. Attorney burnout and substance use issues are well-documented industry problems. Strong EAP and mental health coverage is increasingly table stakes.

Selecting carriers based on partner preference for "their doctor." Verify the network actually covers the specialists associates and their families need, not just the partner's preferred internist.

Not re-shopping at renewal. Carrier rates and product offerings change. The carrier that fit the firm 5 years ago rarely still fits today.

Forgetting workers' comp. Required in Georgia at 3+ employees. Not bundled with health.

Ignoring disability and life insurance. Long-term disability is meaningful for high-income attorneys whose families depend on professional income. Often underdone in firm benefit packages.

Common Mistakes Atlanta Tech Founders Make

Patterns I see repeatedly:

Staying on a PEO for benefits without ever pricing it out independently. Convenience tax is real — typically $40-80K/year for a 25-person company.

Defaulting to ACA-compliant without exploring private medically underwritten. For young healthy engineering teams, this is the single most expensive mistake. 25-40% savings on the table.

Setting up cash stipends instead of ICHRA. Same employer cost, 33% less employee value, plus payroll tax exposure.

Crossing 50 FTE without redesigning benefits. Surprise ACA Employer Mandate penalties can hit $50-100K+ in the first year.

Choosing the cheapest carrier without checking network depth in Atlanta. Some plans don't include Emory specialists or Northside. Verify before signing.

Treating benefits as a static decision. Re-shop annually. Carrier rates change; your team composition changes; what was right at 8 employees isn't right at 25.

Excluding founders from ICHRA without understanding entity-specific rules. S-Corp shareholder-employees with W-2 wages can typically participate. Sole proprietors and LP partners generally cannot. Run with your CPA.

Forgetting workers' comp. Georgia requires it at 3+ employees. Most tech startups don't have high-injury exposure, but the policy is required and not bundled with health.

Not factoring benefits into hiring brand. Top engineering candidates compare benefit packages. A weak benefits offering reads as "early-stage and underfunded" to senior candidates.

The Atlanta Law Firm Carrier Landscape

For private medically underwritten group plans in Atlanta for 2026:

Allstate Benefits — strong for professional services, competitive on mid-size firms

Trustmark — flexible plan design, common pick at 10-50 attorneys

Allied National — competitive for professional services groups

National General (Allstate) — level-funded with underwriting overlay

For ACA-compliant fully insured group plans:

Anthem Blue Cross Blue Shield of Georgia — broadest network including Emory, Piedmont, Wellstar, Northside specialists

UnitedHealthcare — competitive, strong PPO networks

Aetna — good for mixed demographic firms

Cigna — strong network in metro Atlanta

Kaiser Permanente — integrated care, popular with younger associates who value the HMO experience

For ICHRA-eligible individual marketplace plans:

Anthem Pathway PPO — broad network, common attorney pick (Emory, Piedmont in-network)

UnitedHealthcare — solid marketplace presence

Cigna — competitive in metro Atlanta

Oscar — strong digital experience, popular with younger associates

Ambetter — value-priced option

Frequently Asked Questions

Can equity partners participate in our group health plan? Not in the traditional W-2 employee sense. K-1 partners are not employees for benefit purposes. They can participate in ICHRA with specific structuring, or buy their own coverage and deduct premiums via the self-employed health insurance deduction. Talk to your CPA before designing.

Will my associates leave if the plan isn't generous enough? Possibly. Benefits are a top-3 factor in associate retention surveys consistently. Maternity coverage, mental health, and family/dependent coverage are particularly important to associates in their family-formation years.

Should we use the same broker for the firm's malpractice and the firm's health benefits? Sometimes works, often doesn't. Malpractice insurance and group health are different products with different broker specializations. Verify your broker has demonstrable depth in both before consolidating.

How does workers' comp interact with our group health plan? Workers' comp is required in Georgia at 3+ employees and is separate from group health. Office injuries (slip-and-fall, repetitive strain) are covered by WC. General health is covered by group health. Not bundled.

What about disability insurance for our attorneys? Long-term disability is increasingly part of the firm benefit package. For attorneys earning $200K+, individual disability policies (in addition to or instead of group disability) make sense because group LTD typically caps benefit amounts. Often overlooked, worth designing in.

Can part-time of-counsel attorneys be in our group plan? Generally no. Group plans typically require 30+ hours/week. Of-counsel attorneys who are 1099 contractors aren't employees for group health purposes. They'd need individual coverage.

How long does benefits setup take for a law firm? Private medically underwritten and ACA-compliant group plans: 45-60 days from underwriting to effective date. ICHRA setup: 30-45 days for TPA setup + employee plan selection. Most firms target a July 1 or January 1 plan year start.

What happens if our firm merges with another firm? Group health plans transition on the merger close date or the next renewal. ICHRAs can be inherited or unified. Plan the benefits transition with the M&A team — benefits gaps during a merger are a Day 1 attorney retention risk.

The Bottom Line

Atlanta law firms have structurally different benefit needs from restaurants or tech startups. The K-1 partner vs W-2 associate distinction changes everything about eligibility and tax treatment. The older average age changes the cost-benefit math on private medically underwritten plans. The high-touch attorney relationship with health benefits — maternity, mental health, specialist network depth — raises the floor on what "good coverage" means.

For most Atlanta law firms, the right structure is a hybrid: private medically underwritten group plan for W-2 associates and staff (when the group underwrites favorably), ICHRA for equity partners (CPA-structured for K-1 compatibility), unified by a single broker who handles both. This delivers the cost savings of medical underwriting where it works AND the partner-eligibility flexibility of ICHRA where it matters.

For firms with older partner-heavy demographics or significant remote/multi-state populations, full ICHRA often delivers the best combination of cost control, partner participation, and administrative simplicity.

If you're a managing partner evaluating your firm's benefit structure — or running your first benefit review since founding — book a 15-minute call with me. I'll walk through your firm's specific structure and quote both private medically underwritten and ICHRA approaches with real numbers. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out What Health Insurance Should Atlanta Tech Startups Offer?, What Health Insurance Should Atlanta Restaurants Offer?, or Level-Funded or Fully Insured Group Health? — parallel professional services and small business decisions.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal, tax, or financial advice. PEO contract terms, ICHRA compliance rules, ACA Employer Mandate thresholds, FTE calculations, and Georgia carrier offerings change