ICHRA vs QSEHRA: Which Fits My Atlanta Business?

Author: Justin Bishop · June 18, 2026 · 10 min read

If you own a small business in Atlanta and you have been researching tax-advantaged health benefit alternatives to group insurance, you have probably encountered both acronyms — ICHRA and QSEHRA. Both let an employer reimburse employees tax-free for individual health insurance. Both are creatures of IRS rules. Both sound like the same thing wearing slightly different clothes.

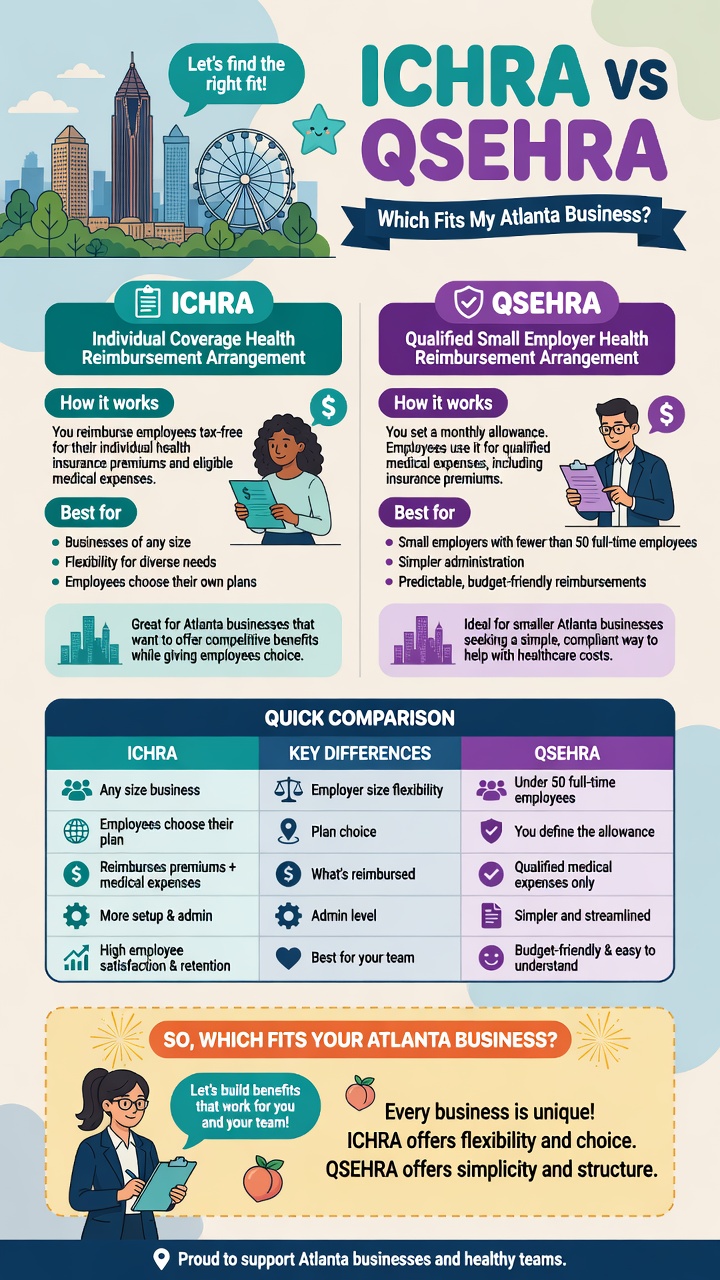

They are not the same thing. QSEHRA came first (2016) and works for small employers under 50 FTE with capped annual reimbursements. ICHRA came later (2020) and works for any size employer with unlimited reimbursement amounts and a more flexible class-based tiering structure. For most Atlanta small businesses that have a choice between the two, ICHRA wins decisively — but there is a narrow set of circumstances where QSEHRA's simplicity and lower setup cost is the right answer.

This post walks through what each structure actually is, the four meaningful differences between them, when QSEHRA's narrow advantages matter, when ICHRA dominates, the 2026 reimbursement math in metro Atlanta for both, and the hidden premium tax credit interaction that catches most owners off guard.

I'm Justin Bishop, an independent broker in Atlanta. I set up both QSEHRA and ICHRA structures for Georgia small businesses — and I tell owners which one fits before they commit. Here's the honest breakdown.

The 30-Second Version

QSEHRA: Qualified Small Employer Health Reimbursement Arrangement. Created 2016. Only for businesses under 50 FTE. Capped annual reimbursement amounts (approximately $6,500 self-only / $13,100 family for 2026 — verify the IRS-indexed amount each year). Reimbursements must be uniform across all eligible employees (limited variation allowed for age and family status). Simpler to administer; fewer compliance requirements.

ICHRA: Individual Coverage Health Reimbursement Arrangement. Created 2020. Any size business — no FTE limit. No reimbursement caps. Allows class-based tiering (different reimbursement amounts for full-time vs part-time, salaried vs hourly, geographic locations, etc.). More flexible; more compliance complexity.

The four meaningful differences: Contribution caps (QSEHRA has them, ICHRA doesn't) Business size eligibility (QSEHRA capped at 50 FTE, ICHRA any size) Class-based tiering (QSEHRA limited, ICHRA flexible) Group health compatibility (QSEHRA can't be combined; ICHRA can be for different classes)

When QSEHRA wins: very small business (under 25 FTE), uniform workforce, owner wants minimum setup cost, modest reimbursement budget that fits inside the IRS caps anyway, no plans to grow past 50 FTE

When ICHRA wins: anything else. Multi-class workforces, growth-stage businesses, owners who want to fund above the QSEHRA caps, multi-state employee populations, restaurants/hospitality/construction with mixed FT/PT classes, businesses that already have group health and want to add an HRA for a separate class

The hidden tax credit trap: employees offered "affordable" QSEHRA or ICHRA reimbursement amounts forfeit their right to ACA marketplace premium tax credit subsidies for the entire family unit. For employees who would qualify for substantial subsidies as individuals, this can change the math materially. Run the employee-by-employee math before committing.

Setup cost and complexity: QSEHRA TPA fees are typically $200-500/year for very small businesses. ICHRA TPA fees are typically $400-1,500/year. Not a major factor, but real.

The right move for most Atlanta small businesses: ICHRA, unless you specifically fit the narrow QSEHRA profile.

What QSEHRA Is (Quick Background)

The Qualified Small Employer Health Reimbursement Arrangement was created by the 21st Century Cures Act in December 2016. It was designed to give small employers a tax-advantaged way to help employees pay for individual health insurance without offering a group plan.

Key rules:

Business size: Only employers with fewer than 50 full-time-equivalent (FTE) employees qualify. Cross 50 FTE and the structure becomes unavailable

Cannot offer group health at the same time. QSEHRA replaces a group plan; you cannot run both

Capped reimbursement amounts. For 2026, approximately $6,500 self-only and $13,100 family annually (the IRS adjusts these each year for inflation; verify current limits before designing)

Reimbursement uniformity. All eligible employees in the same household tier must receive the same reimbursement amount, with limited variation allowed for age and family status

Eligible expenses: Premium reimbursement for individual ACA marketplace plans (Georgia Access in Georgia), some Medicare premiums, and qualified medical expenses depending on plan design

Employee eligibility: Generally all W-2 employees who have qualifying coverage are eligible; can exclude part-time, seasonal, under-25 workers, and union employees

Tax treatment: Reimbursements are tax-free to the employee (with one significant caveat covered in the premium tax credit section below) and fully deductible to the business

Setup mechanics:

Employer adopts a QSEHRA plan document and notifies employees 90 days before the plan year

Employees enroll in individual ACA marketplace plans

Employees submit proof of coverage and premium payments to a TPA (or directly to the employer for very small setups)

TPA verifies coverage and processes reimbursements up to the cap

Plan year typically runs January 1 to December 31

What ICHRA Is (Quick Background)

The Individual Coverage Health Reimbursement Arrangement was created by Treasury, IRS, and HHS regulations finalized in June 2019 and effective January 2020. It was designed to fix QSEHRA's limitations and give employers of any size a more flexible tax-advantaged structure.

ICHRA is covered in depth in Should My Atlanta Small Business Switch to ICHRA in 2026? — the short version:

Business size: Any. No FTE limit. Works for 2-person LLCs and 5,000-person enterprises

Can be combined with group health for different classes. You can offer group health to full-time W-2 employees and ICHRA to part-time, remote, or other classes

No reimbursement caps. Employer sets the amount based on what fits the business

Class-based tiering. Up to 11 IRS-defined employee classes (full-time, part-time, salaried, hourly, geographic location, seasonal, collective bargaining, etc.) can each receive different reimbursement amounts

Reimbursement uniformity within a class. All employees in the same class must get the same amount, with allowed variation for age and family status

Eligible expenses: Premium reimbursement for individual ACA marketplace plans (Georgia Access), individual coverage purchased off-exchange, Medicare Parts A and B and supplemental, and some other qualifying coverage types

Tax treatment: Reimbursements are tax-free to the employee (with the same premium tax credit caveat as QSEHRA) and fully deductible to the business

The minimum class size requirement. When ICHRA is combined with group health, classes must meet minimum employee counts (5-20 depending on total workforce size) to prevent gaming

ICHRA setup is more complex than QSEHRA but the flexibility is dramatically greater.

The Head-to-Head Comparison

These are the four differences that actually matter for the QSEHRA-vs-ICHRA decision.

Difference #1: Contribution Caps

QSEHRA is capped. For 2026, approximately $6,500 self-only and $13,100 family per year. That works out to roughly $540 self-only and $1,090 family per month. For a 30-year-old employee in metro Atlanta, $540 covers most of a Silver-tier marketplace premium. For a 50-year-old employee, it covers less. For a family of four with a 45-year-old policyholder, $1,090 covers a portion of the family premium — often the employee is paying meaningful out-of-pocket for the remainder.

ICHRA has no cap. Employers set the amount based on what fits the business. Some Atlanta businesses run ICHRA at $400/month per employee; others run it at $1,200/month. The right amount depends on workforce age, marketplace pricing in the relevant counties, and the business's benefit budget.

This is the most consequential difference for older workforces. A QSEHRA reimbursement that fully covers a 28-year-old's premium might cover only 60-70% of a 55-year-old's premium for the same plan tier. ICHRA can be set high enough to cover both age extremes meaningfully.

Difference #2: Business Size Eligibility

QSEHRA requires under 50 FTE. If you are at 48 FTE and growing, QSEHRA is a temporary structure — once you cross 50 FTE, the QSEHRA dissolves and you have to migrate to a different structure mid-stream. That migration is administratively painful.

ICHRA has no size limit. Works for 2-person LLCs (see Can a 2-Person LLC Get Group Health?) and works for businesses with 5,000+ employees. Growth doesn't force a structure change.

For growth-stage Atlanta businesses, this alone is usually enough to pick ICHRA. Why build a QSEHRA in 2026 if you might cross 50 FTE in 2027 and have to rebuild as ICHRA?

Difference #3: Class-Based Tiering

QSEHRA reimbursements must be uniform. All eligible employees get the same amount (with allowed variation for age and family status). You cannot give your senior managers a higher reimbursement than your hourly staff.

ICHRA allows class-based tiering across up to 11 defined classes. Full-time vs part-time, salaried vs hourly, geographic location, seasonal, and several other categories. Your full-time salaried employees can get $700/month while part-time staff get $400/month, structured legally within the rules.

This matters enormously for restaurants, hospitality, construction, and any business with mixed full-time and part-time workforces. Covered in depth in What Health Insurance Should Atlanta Restaurants Offer? — the class structure is often the reason ICHRA fits where QSEHRA does not.

Difference #4: Group Health Compatibility

QSEHRA cannot be combined with a group plan. It is one or the other. If you want to give your W-2 salaried staff group health and your part-time staff a tax-advantaged HRA, QSEHRA doesn't work.

ICHRA can be combined with group health for different classes. Group plan for full-time W-2 employees + ICHRA for part-time, remote, or seasonal classes is a legitimate structure. This is increasingly common for businesses with hybrid workforces.

When QSEHRA Wins (The Narrow Cases)

QSEHRA still fits a specific business profile. It is rare but real.

Profile 1: Very small business (under 25 FTE), uniform workforce, modest budget. A 12-person Atlanta professional services firm where every employee is full-time W-2, similar age range, and the owner wants to offer ~$500/month per employee toward marketplace coverage. The reimbursement amount fits inside the QSEHRA cap, the workforce is uniform, and QSEHRA's lower administrative complexity wins.

Profile 2: Owner specifically wants the simplest possible setup. QSEHRA TPA fees are typically $200-500/year for very small businesses. ICHRA TPA fees can be $400-1,500/year. For a 6-person business where every reimbursement dollar matters, the simpler structure has appeal.

Profile 3: No plans to grow past 50 FTE and no need for class tiering. A stable mature business (long-tenured staff, low growth trajectory, uniform compensation) where the QSEHRA limitations never bind in practice.

Profile 4: Bootstrapped early-stage businesses testing the HRA waters. Some owners want to try a tax-advantaged HRA structure before committing to ICHRA's complexity. QSEHRA's lower setup cost lets them experiment for a year or two before deciding.

The honest reality: even in these profiles, ICHRA is often still the right call. The QSEHRA caps that fit today may not fit in two years as the workforce ages or grows. The administrative cost difference shrinks once you account for the long-term flexibility ICHRA preserves.

When ICHRA Wins (Most Cases)

For most Atlanta small businesses, ICHRA is the right answer. The specific profiles:

Anywhere the owner wants to reimburse above the QSEHRA caps. Higher reimbursement amounts produce stronger employee benefit value and better recruitment/retention

Multi-class workforces (full-time vs part-time, salaried vs hourly, geographic spread). The class-based tiering structurally requires ICHRA

Growth-stage businesses. Avoiding the 50-FTE QSEHRA cliff

Restaurants, hospitality, construction, and other high-turnover or mixed-FT/PT industries. Class flexibility is essential

Businesses that already have group health for some employees. ICHRA can layer for separate classes; QSEHRA cannot

Multi-state or multi-office employee populations. ICHRA accommodates geographic class structures

Practices and firms with K-1 partner / W-2 associate splits. ICHRA's flexibility handles owner participation patterns that QSEHRA's uniformity cannot

Medical practices with older owners and younger staff. See What Health Insurance Should Atlanta Medical Practices Offer? — the owner-staff demographic split typically requires ICHRA's flexibility

For most businesses with an actual choice between QSEHRA and ICHRA, ICHRA's structural advantages exceed the administrative cost difference.

Atlanta Reimbursement Math: QSEHRA Caps vs ICHRA Flexibility

Concrete numbers help. Here are real 2026 scenarios for typical Atlanta small businesses.

Scenario A: 8-person professional services firm, uniform young staff

8 W-2 employees, all single, age range 28-38

2026 Silver-tier marketplace plan for a 33-year-old in metro Atlanta: ~$485/month

Owner wants to offer 100% of Silver-tier premium coverage

QSEHRA approach:

$485/month × 12 = $5,820/year per employee

Within the QSEHRA self-only cap of ~$6,500

Total annual cost: 8 employees × $5,820 = $46,560

TPA admin fee: ~$300

Total: ~$46,860

ICHRA approach:

Same $485/month reimbursement structure

Same total annual cost: ~$46,560

TPA admin fee: ~$600

Total: ~$47,160

In this scenario QSEHRA is structurally fine and modestly cheaper to administer (~$300/year). Owner could pick either.

Scenario B: 22-person restaurant, mixed FT/PT, mixed ages

12 full-time W-2 employees (cooks, managers, salaried) age 25-55

10 part-time servers and hosts (under 30 hours/week)

Owner wants to offer $600/month to full-time staff, $300/month to part-time

QSEHRA approach: Structurally impossible. QSEHRA requires uniform reimbursement across eligible employees. The owner would have to either:

Offer all 22 the same amount (averaging down the FT staff benefit)

Exclude part-timers entirely (defeats the purpose)

ICHRA approach:

Full-time class: 12 × $600/month × 12 = $86,400/year

Part-time class: 10 × $300/month × 12 = $36,000/year

Total: $122,400/year + TPA admin (~$900)

Class structure preserves the benefit philosophy

ICHRA wins this scenario decisively. QSEHRA cannot deliver the tiered structure the business actually wants.

Scenario C: 30-person tech startup, all W-2, ages 26-45, some remote

25 employees in metro Atlanta

5 remote employees in 3 other states

Owner wants $800/month reimbursement

Above the QSEHRA self-only cap of ~$6,500/year (= ~$542/month)

QSEHRA approach: Structurally impossible. The reimbursement amount exceeds the cap. Even if it didn't, multi-state coverage is administratively cleaner under ICHRA's geographic class structure.

ICHRA approach:

30 employees × $800/month × 12 = $288,000/year + TPA admin (~$1,200)

Each employee picks the marketplace plan that works in their state

ICHRA wins. The reimbursement amount alone disqualifies QSEHRA.

The Hidden Premium Tax Credit Trap

This is the single most overlooked factor in the QSEHRA vs ICHRA decision — and it affects both structures equally.

The rule: Employees who are offered "affordable" QSEHRA or ICHRA reimbursement amounts forfeit their right to ACA marketplace premium tax credit subsidies for the entire family unit, not just themselves.

"Affordable" has a specific IRS definition tied to the cost of the lowest-cost marketplace plan and the employee's household income. The details get technical, but the practical effect is:

An employee who would qualify for $400/month in marketplace subsidy as an individual loses that subsidy when offered ICHRA or QSEHRA reimbursement, even if the employer's reimbursement is less than the lost subsidy

For employees over 400% of federal poverty level (no subsidy available anyway), the trap doesn't apply

For employees under 250% of federal poverty level, the trap can be severe — they may be financially worse off taking the employer's reimbursement than declining it

How to handle the trap:

Run the employee-by-employee math before committing. The right ICHRA or QSEHRA reimbursement amount should at minimum offset the lost subsidy for affected employees

Employees have the right to decline ICHRA or QSEHRA participation. They can opt out and keep their marketplace subsidy

Communicate clearly so employees understand what they are choosing between

This applies to both structures. It is not a QSEHRA-vs-ICHRA differentiator. But it is a question every owner should run through before deciding whether to offer either structure at all.

Common Mistakes Atlanta Owners Make on the QSEHRA vs ICHRA Decision

Patterns I see at HRA setup conversations:

Picking QSEHRA for simplicity without testing the cap math. If your intended reimbursement is close to the QSEHRA cap, you are building toward an immediate limitation. Pick ICHRA so you have headroom

Picking ICHRA without understanding the class structure requirements. ICHRA's class flexibility is powerful but requires written plan documents that define each class precisely. Skipping this creates compliance risk

Forgetting to count FTE correctly for QSEHRA eligibility. Part-time employees aggregate into FTE under specific calculation rules. A business that thinks it has 35 employees might actually have 52 FTE and be disqualified from QSEHRA

Treating QSEHRA as a permanent solution when the business is growing. Crossing 50 FTE forces a migration to ICHRA. Better to start on ICHRA if growth is plausible

Ignoring the premium tax credit trap. The single most common after-the-fact regret in HRA adoption. Run the employee-by-employee math first

Not communicating the structure clearly to employees. Employees who feel surprised by the QSEHRA or ICHRA structure resent the rollout. Plan for one-on-one education meetings

Picking a TPA based on price alone. The TPA's compliance support, member-side experience, and broker integration matter more than the annual fee. The cheapest TPA often costs more in employee frustration

Forgetting workers' comp. Required in Georgia at 3+ employees and separate from any HRA structure

Confusing QSEHRA with a Section 125 cafeteria plan. Different rules, different tax treatment, different administrative requirements. They can complement each other but they are not the same thing

Frequently Asked Questions

Can I switch from QSEHRA to ICHRA later if my business grows? Yes, but the transition requires planning. The QSEHRA must be terminated and a new ICHRA plan document must be adopted. The 90-day employee notice requirement applies to the ICHRA rollout. Most businesses time the transition to a January 1 plan year start. Some compliance gaps can open during the transition if it is not managed carefully.

If I have a 2-person LLC, can I offer QSEHRA or ICHRA? Yes for both, with caveats. The structure works for the W-2 employee (if there is one). The owner's participation depends on entity type and CPA structuring. See Can a 2-Person LLC Get Group Health? for the smallest-end specifics, and Should My Atlanta Small Business Switch to ICHRA in 2026? for owner participation detail.

Do employees have to enroll in ACA marketplace plans, or can they use any individual coverage? For both QSEHRA and ICHRA, employees can use individual ACA marketplace plans (Georgia Access in Georgia), off-exchange individual plans, and Medicare with supplemental coverage. Short-term medical plans and ministry plans generally don't qualify. Employees submit proof of qualifying coverage to the TPA for reimbursement verification.

What if my employee is on a spouse's group health plan? They can still receive QSEHRA or ICHRA reimbursement for excess premium they pay on the spouse's plan (typically the family-coverage upgrade cost) and for qualified medical expenses if the plan design allows. They are not eligible for premium reimbursement on a spouse's employer-provided plan. The TPA verifies eligible expenses.

Are there state-level rules in Georgia that affect QSEHRA or ICHRA? Not significantly. Both structures are federal creations. Georgia state insurance law does not impose additional QSEHRA or ICHRA restrictions. The Georgia Access marketplace operates independently for individual enrollment. Always verify with a licensed broker if your specific situation has state-law complications.

How does the premium tax credit interaction work mechanically? When you offer QSEHRA or ICHRA reimbursement to an employee at an "affordable" level (defined by IRS rules), the employee is no longer eligible for marketplace premium tax credit subsidies for themselves OR their family. The employee can decline the HRA reimbursement to preserve their subsidy. This is a meaningful trade-off for subsidy-eligible employees that the rollout needs to address.

What happens if I set up QSEHRA and grow past 50 FTE mid-year? The QSEHRA disqualifies. You must transition to ICHRA (or a group plan) within a reasonable timeframe. The transition creates administrative complexity and can leave employees in a coverage gap if not managed carefully. This is the strongest argument for starting on ICHRA if growth is plausible.

Are reimbursements taxable to the employee if their plan covers them with subsidies? This is where the premium tax credit trap shows up in the math. If the employee accepts QSEHRA or ICHRA reimbursement, the reimbursement itself is tax-free, but the employee forfeits their subsidy. If they decline the HRA and keep the subsidy, the subsidy is tax-advantaged in the normal marketplace way. The right answer depends on which dollar amount is larger.

The Bottom Line

QSEHRA and ICHRA are both legitimate tax-advantaged HRA structures. They are not the same thing.

For very small Atlanta businesses (under 25 FTE) with uniform workforces, modest budgets that fit inside the IRS caps, and no plans to grow past 50 FTE, QSEHRA can be the right answer — slightly simpler, slightly cheaper to administer, no downside in practice.

For everyone else — businesses with mixed workforces, growth-stage trajectories, multi-state populations, owners who want to reimburse above the QSEHRA caps, or any business with a group plan already in place — ICHRA is the right answer. The class-based tiering, the size flexibility, the absence of contribution caps, and the group-health compatibility all matter.

The single most important pre-decision step is running the employee-by-employee premium tax credit math. Both structures can leave low-income employees financially worse off if the reimbursement isn't designed to offset the lost subsidy. Skip this step and you create resentment among the staff you are trying to retain.

If you are an Atlanta small business owner deciding between QSEHRA and ICHRA — or trying to figure out whether either fits at all — book a 15-minute call with me. I'll model both options against your specific workforce, run the premium tax credit math employee-by-employee, and tell you honestly which structure fits. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out Should My Atlanta Small Business Switch to ICHRA in 2026? for the ICHRA-specific decision framework, Best Georgia Small Group Health Insurance Carriers for 2026 for the carrier menu your broker should be shopping, or How Do I Pick a Small Business Health Broker in Atlanta? for the questions to ask any broker quoting these structures.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal, tax, or financial advice. QSEHRA and ICHRA rules, IRS-indexed contribution amounts, ACA premium tax credit eligibility rules, and Georgia marketplace specifics can change.