How Do I Pick a Small Business Health Broker in Atlanta?

Author: Justin Bishop · June 10, 2026 · 10 min read

If you run a small business in Atlanta, the moment you decide to offer health insurance to your team, your inbox fills up. LinkedIn messages. Cold calls. Referrals from your CPA. A friend's cousin who just got into insurance. Everyone wants to be your broker.

Most owners pick the first one who seems competent, gets one or two quotes back quickly, and answers the phone when they call. That is usually the wrong way to pick.

The right broker can save your business 15-25% per year, place you with carriers you would never find on your own, handle claim disputes when they happen, and quote alternatives like ICHRA and private medically underwritten plans that captive agents and online platforms structurally cannot reach. The wrong broker can lock you into a plan that does not fit, miss your renewal deadlines, and disappear when an employee's claim gets denied.

This post walks through the structural differences between broker types, the 8 questions to ask before you sign anything, the red flags to walk away from, and what good looks like.

I'm Justin Bishop, an independent broker in Atlanta. I get the "how did you pick your broker?" conversation from new clients all the time — usually after they have fired the wrong one. Here's the honest framework.

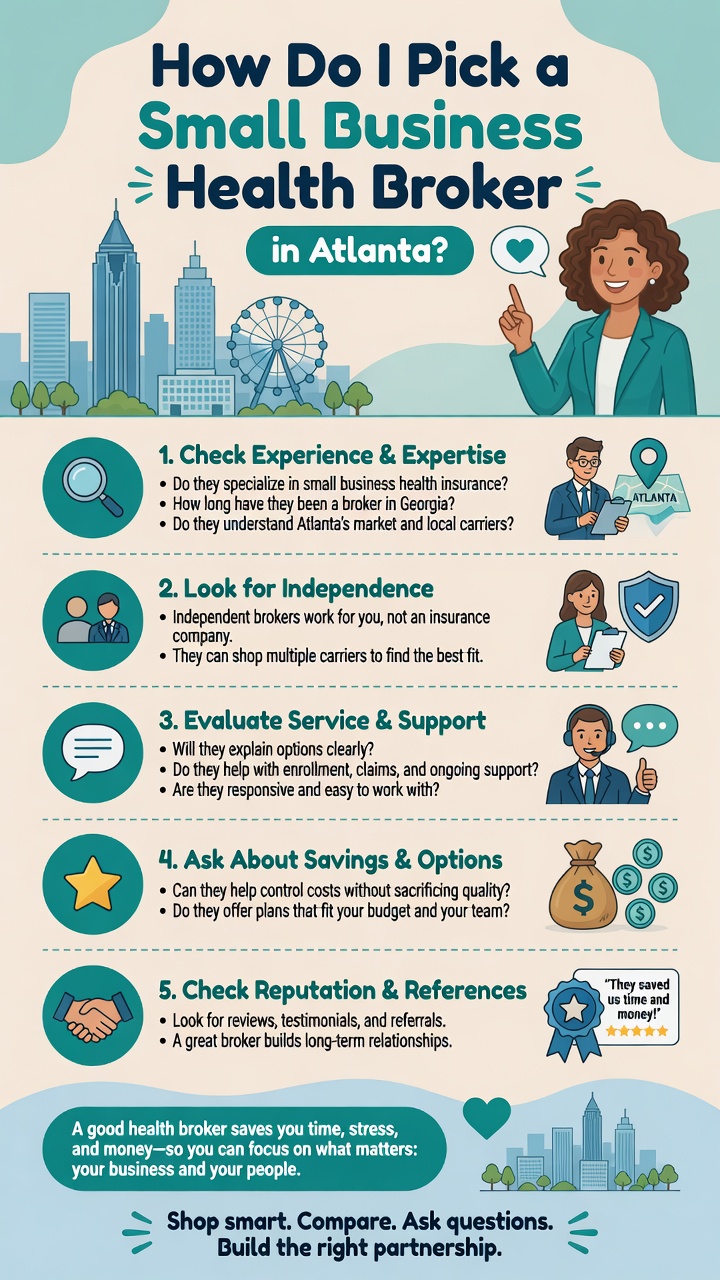

The 30-Second Version

Three types of broker exist: independent broker, captive agent, online platform. Each has different structural incentives.

Independent broker: shops 10+ carriers, gets paid by whichever carrier you choose. Best fit for most Atlanta small businesses. Can quote ACA-compliant fully insured, private medically underwritten, level-funded, and ICHRA structures side-by-side.

Captive agent: sells one carrier (State Farm, Allstate, etc.). Cannot shop the market. Avoid for group health.

Online platform (Gusto, Justworks, Take Command Health, Rippling, TriNet): handles paperwork at scale, less personal service, often does not help with claim disputes.

The 8 questions to ask: how many carriers do you quote, are you independent or captive, who handles renewal, what is your average response time, will you help me with claim issues, what is your client retention rate, can you give me 3 references in my industry, and what is your involvement at year-end reconciliation.

The bonus question (new in 2026): are you appointed to quote private medically underwritten group plans and ICHRA, not just ACA-compliant fully insured? Most brokers are not. Those that are can save healthy small groups 15-40% over the ACA-compliant menu (covered in Level-Funded or Fully Insured Group Health?).

Biggest red flag: broker quotes one carrier and pushes for fast signing. Means they are not shopping the market — they are working an angle.

Biggest green flag: broker pushes back on your initial assumptions and says let me run the math both ways before we decide.

What you will pay the broker: $0. Broker commissions are paid by carriers, built into premium. Going direct does not save you money — you just lose the broker service.

The Three Types of Broker (and Why It Matters)

Not every insurance broker is the same. The label gets thrown around loosely. There are real structural differences that determine who can actually help your business.

Independent broker

Represents multiple carriers — typically 10-30 health insurance carriers, often more for individual products. Not employed by any one carrier. Gets paid a commission by whichever carrier you ultimately choose, with similar commission percentages across carriers so the broker is not biased toward one carrier over another.

Best for: Small businesses who want their broker to actually shop the market. The structural setup means the broker's job is to find the best fit, not to push one carrier.

Trade-off: Slightly slower than captive agents at quoting (because they are getting 5-10 quotes instead of one), and slightly less name recognition than the big captives.

Captive agent

Employed by or contracted exclusively with one carrier (State Farm, Allstate, Liberty Mutual, etc.). Can only sell that carrier's products. Often heavily incentivized to sell certain products by their employer.

Best for: Personal auto or homeowners insurance if you specifically want one of those carriers. Not recommended for group health insurance, because they cannot shop the market. If their carrier is not the best fit for your group, they have no answer.

The trap: Captive agents are often the most prominent in marketing and referrals. They are easy to find. But the convenience comes at the cost of optionality.

Online platform / PEO

Companies like Gusto, Justworks, Rippling, Take Command Health, and TriNet bundle payroll, HR, and benefits administration into a single platform. They handle group health as one of many services.

Best for: Fast-growing tech companies with simple needs and a strong preference for self-service. The bundled payroll-and-benefits integration is genuinely useful for some setups.

Trade-off: Often charges 2-12% of payroll on top of premium. Less personal service. Limited claim help — when an employee's claim gets denied, the platform's chat support typically cannot escalate the way a relationship-broker can. The PEO trap is covered in depth in What Health Insurance Should Atlanta Tech Startups Offer?.

Why Atlanta small businesses usually win with independent brokers

For most Atlanta small businesses (2-50 employees), an independent broker wins on three structural dimensions:

Carrier optionality — captives cannot shop; platforms shop a narrow set; independents shop all five major Georgia small group carriers (see Best Georgia Small Group Health Insurance Carriers for 2026) plus private medically underwritten alternatives plus ICHRA

Local Atlanta knowledge — which Georgia carriers are strong in which ZIP codes, which hospital networks (Emory, Piedmont, Wellstar, Northside) are in-network for which carriers, which carriers have favorable underwriting for which industries

Claim escalation — when something goes wrong, an established independent broker has direct lines to carrier reps that platforms and captives do not

The 8 Questions to Ask Any Broker Before You Sign

Print this list. Ask every broker who pitches you. The way they answer tells you whether they are going to actually serve you for the next 5+ years or churn through to the next prospect after onboarding.

1. How many carriers will you quote?

Right answer: 5+ for group health, ideally 8-10. If the answer is just one or two or we focus on Anthem/UHC primarily — they are not shopping the market.

2. Are you independent, or captive with one carrier?

Right answer: Independent — I represent multiple carriers. If they answer captive or tied to one carrier — fine for personal auto, but they cannot fairly shop group health for you.

3. Who handles my renewal next year?

Right answer: Me, personally. I reach out 90 days before renewal with shop-the-market quotes. Wrong answer: Our service team handles renewals or you will get an email from underwriting. That means your broker disappears after onboarding.

4. What is your average response time on a question or claim issue?

Right answer: Same day, or specific commitment (e.g., within 4 business hours). Wrong answer: vague (we get back to clients quickly) or no specific commitment.

5. Will you help me when a claim is denied or disputed?

Right answer: Specific examples of past denials they have helped resolve. Wrong answer: Talk to your carrier directly. If they punt claim issues, they are an onboarding broker, not a relationship broker.

6. What is your client retention rate?

Right answer: 85%+ for established brokers, with a credible reason for the churn (e.g., we lost a few when one carrier exited Georgia). Wrong answer: I do not track that or we do not really lose clients (everyone loses some clients; not tracking is a tell).

7. Can you give me 3 references in my industry?

Right answer: They name specific companies in your industry within 24 hours. Wrong answer: Vague references or no industry-specific clients. If they do not have references in your space, they do not understand your underwriting profile.

8. What is your involvement at year-end reconciliation?

This one is specific to level-funded and ASO plans. Right answer: I will review your claims report quarterly and pre-model the renewal scenario in October. Wrong answer: The carrier handles that. If your broker cannot read claims data, they cannot tell you whether your plan is performing.

Bonus question for 2026: Are you appointed to quote private medically underwritten and ICHRA?

This is the question that separates strong independent brokers from average ones in 2026. Most brokers are appointed only with ACA-compliant fully insured carriers — they cannot quote the private medically underwritten products that can save healthy groups 15-40%, and they may not have the infrastructure to set up ICHRA. A good Atlanta independent broker should be able to quote ACA-compliant, private medically underwritten, level-funded, and ICHRA structures side-by-side and tell you honestly which fits. If a broker says we just do ACA-compliant — they are leaving real money on the table for your business.

Red Flags to Walk Away From

Patterns I have seen Atlanta business owners get burned by:

Pressure to sign fast. Real brokers know group health is a 5+ year decision. Anyone pushing we need to sign this week to lock in rates is either misinformed or working a quota.

Quoting only one carrier without explanation. If you only see one quote, you are not seeing the market. Every good broker can explain why the carriers they did not quote were not a fit.

No written renewal commitment. A broker who cannot commit in writing to a renewal process and timeline is not going to be there next year.

No clear answer on commission. Healthy brokers will tell you exactly how they are paid (typically 4-7% of premium, paid by the carrier). Anyone who dodges the question is hiding something.

No physical Atlanta presence. Online-only platforms struggle with claim disputes that require local carrier relationships. The Atlanta-specific knowledge matters more than people think.

We handle 500+ businesses. Sounds impressive, often means you are a small fish in their book. A broker with 30-80 small business clients gives you more attention than one with 500.

Promises a specific carrier without seeing your group's demographics. Anyone who says we will get you Anthem at $X before reviewing your census is making it up.

Generic, non-specific renewal email last year. If you have had a broker before and your last renewal email was a copy-paste rates are increasing 12%, let me know if you want to shop — that is an onboarding broker, not a relationship broker.

Only quotes ACA-compliant fully insured. If your group is healthy and the broker has not even mentioned private medically underwritten or ICHRA as alternatives, you are getting the narrow menu — not the full menu.

Green Flags — What a Good Broker Actually Does

The opposite of the red flags. These are the patterns you should see in someone you would actually want as your broker for the next decade:

Asks more questions than you do. Real brokers want to understand your business, your team's demographics, your cash flow, and your priorities before they recommend anything.

Pushes back on your assumptions. If you say I want the cheapest plan possible, a good broker says let us make sure cheap does not cost you when someone has a baby. That pushback is the value.

Shows you the bad-case scenario. Whether it is level-funded vs fully insured, ICHRA vs group, or HMO vs PPO, a good broker models the bad case, not just the projected case.

Has Atlanta-specific examples. I just placed a Buckhead family of 5 with Anthem or I helped a Sandy Springs S-Corp set up an ICHRA last quarter. Real client work, anonymized.

Names specific carrier reps. Good brokers have direct lines to specific people at each carrier. When something goes wrong, they call that person, not the 800 number.

Talks about claims, not just premiums. Premium is the cost; claims handling is the service. A broker who only talks about premium is not going to be useful when you actually need them.

Has a Calendly or direct number. You should not have to go through a gatekeeper to reach your broker for a 15-minute question.

Quotes the full menu. ACA-compliant fully insured, private medically underwritten, level-funded, ICHRA — all four on the table where structurally appropriate. The narrower the menu, the narrower the broker.

Common Pitches That Should Make You Walk

Specific scripts to watch for:

We can get you 30% off your current rate. Possibly true, possibly not — but if they are promising savings before seeing your current plan or claims history, they are guessing. Walk away from anyone who promises savings without doing the work.

This carrier is offering a special this month only. Carriers do not run flash sales on health insurance. If a broker is pitching urgency, they are working a quota.

We handle your business AND your personal insurance — one broker for everything. Sometimes great, sometimes a sign they are a generalist who does not go deep on group health. Ask them to demonstrate their group health expertise specifically before consolidating.

Your CPA recommended us. Good if your CPA actually vetted them. Often the CPA just refers to whoever sends them a holiday gift. Ask your CPA: what is your specific reason for recommending them?

Sign here to get the quote process started. You should not need to sign anything to get quotes. If they want signatures upfront, walk.

ICHRA is not really a fit for small businesses. Sometimes true, often a tell that the broker is not set up to administer ICHRA and would rather steer you away from it. See Should My Atlanta Small Business Switch to ICHRA in 2026? for the honest framework.

How Broker Fees Actually Work (Spoiler: You Do Not Pay Them)

This is the most under-explained part of the entire industry, and it is a common reason small business owners stay away from brokers.

You do not pay your broker directly. Broker commissions are paid by the insurance carrier as a percentage of premium — typically 4-7% for group health, sometimes lower for very large groups.

The premium you pay the carrier is the same whether you went through a broker or signed up direct on the carrier's website. The broker commission is built into the rate structure either way.

This means:

Going direct does not save you a penny on premium

Using a broker does not cost you anything

The broker is incentivized to retain you long-term (they get paid each year you renew)

A bad broker who lets you churn is hurting their own income

The one nuance: some platforms (Gusto, Justworks, etc.) charge an additional administrative fee per employee per month on top of premium, in exchange for the payroll/HR/benefits integration. That fee IS something you pay. Independent brokers typically do not charge per-employee admin fees.

What to Expect From the Quote Process

A normal, healthy broker engagement looks like:

Week 1: Initial conversation. Broker asks about your business, team, goals, current coverage if any, cash flow, and risk tolerance.

Week 2: Broker collects a census (employee demographics for underwriting). Submits to 5-10 carriers across ACA-compliant, private medically underwritten, level-funded, and ICHRA structures where appropriate.

Weeks 3-4: Quotes come back. Broker reviews with you, explains plan differences, runs cost scenarios.

Week 5-6: Decision made. Broker handles paperwork. Plan effective date set.

Weeks 7-8: Implementation. Employees enroll. ID cards distributed.

Total elapsed time: 6-8 weeks for a clean placement. Faster placements (2-3 weeks) are possible but usually mean less shopping.

If a broker promises we can have you set up by next week, you are getting their fastest path, not their best fit.

Frequently Asked Questions

Should I use the same broker for personal and business insurance? You can — and many do — but only if their group health expertise is genuinely deep. Some excellent personal lines brokers are weak on group health, and vice versa. Ask specifically about their group health credentials, carrier appointments, and client mix.

How do I know if my current broker is doing a good job? Three signals: (1) they reach out to you, not the other way around, at least quarterly; (2) they pre-model your renewal in October before you ask; (3) they have helped you with at least one claim issue. If none of those apply, you have an onboarding broker, not a relationship broker.

Can I fire my current broker? Yes, easily. Health insurance broker of record can be transferred to a new broker with a single form. The new broker handles the paperwork. Your coverage does not change — only who manages it on the back end.

What if my company is just 2-3 employees? Are brokers willing to work with me? Some yes, some no. Many established brokers focus on 50+ employee groups because the commission per case is higher. An independent broker who works with very small groups (or who runs ICHRA setups) is the right fit. Ask what is your smallest client — if they say 25+, they may not give you enough attention. See Can a 2-Person LLC Get Group Health? for the smallest-end specifics.

How much should I expect my broker to know about Georgia-specific rules? A lot. They should know which carriers are strong in metro Atlanta vs north Georgia, which hospital networks are in-network on which plans, the Georgia 3-employee workers' comp threshold, the Georgia Access marketplace, and Mini-COBRA rules. If they are vague on Georgia specifics, they are a generalist who happens to work with Georgia clients.

Does it matter if my broker has been in business 30 years vs 5 years? Less than you would think. Carrier appointments, technology, and ICHRA expertise have changed massively in the last 5 years. A newer broker who is deep in current products may serve you better than a decades-established broker who is coasting on relationships from 2010.

What about going direct to the carrier? You can. But you would be paying the same premium as you would with a broker (because broker commission is built into rates regardless), without the benefits of independent shopping, claims help, and renewal management. The direct route makes sense if you genuinely want zero outside help; otherwise, you are leaving service on the table.

Should I get multiple brokers to compete for my business? Not really — and most reputable brokers will not engage in broker bake-offs. What you should do: meet with 2-3 brokers, ask them all the 8 questions above, and pick the one whose answers and approach you trust. Letting multiple brokers run quotes on the same group simultaneously creates carrier confusion and usually ends with worse pricing for everyone.

The Bottom Line

The broker you pick today shapes your group health experience for the next 5-10 years. Get it right and you have a partner who shops the market, handles renewals proactively, models alternatives like ICHRA and private medically underwritten plans, and shows up when something goes wrong. Get it wrong and you are stuck with someone who collects commission and disappears.

The 8 questions in this post (plus the 2026 bonus question on ICHRA and private medically underwritten appointments) separate relationship brokers from onboarding brokers. The red flags identify brokers working an angle. The green flags identify brokers worth a 30-minute conversation.

If you want to walk through these questions with a broker who will answer them on the spot — and tell you the honest answer even if it is I am not the right fit for your business — book a 15-minute call with me. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out Best Georgia Small Group Health Insurance Carriers for 2026 for the carrier menu your broker should be shopping, Should My Atlanta Small Business Switch to ICHRA in 2026? for the ICHRA decision framework, or Level-Funded or Fully Insured Group Health? for the structural alternatives a good broker will model.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal or financial advice. Broker compensation structures, carrier appointments, and group health regulations change