How Much Is Health Insurance for a Young Adult in 2026?

Author: Justin Bishop · May 4, 2026 · 7 min read

If you just turned 26 and got a letter saying you're aging off your parents' health insurance, or you're a couple years out of college trying to figure out what your gig-economy paycheck can actually afford, you're running into the question every young adult eventually does: how much does this actually cost, and what's the cheapest version that doesn't suck?

Most articles online give you national averages and platitudes. That's not useful when you live in Atlanta and you're trying to decide between paying $250 a month or rolling without coverage. You need real numbers.

I'm Justin Bishop, an independent broker in Atlanta. I'm 28 — meaning I literally just went through this. I write health insurance for young adults every week — 1099 contractors, freelance designers, rideshare drivers, recent grads, side-hustle entrepreneurs, single 20-somethings on their own for the first time. Here's the version of "what does young-adult health insurance actually look like" I'd give a friend.

The 30-Second Version

You age off your parents' plan at 26. Aging off triggers a Special Enrollment Period — you get 60 days to enroll in your own coverage.

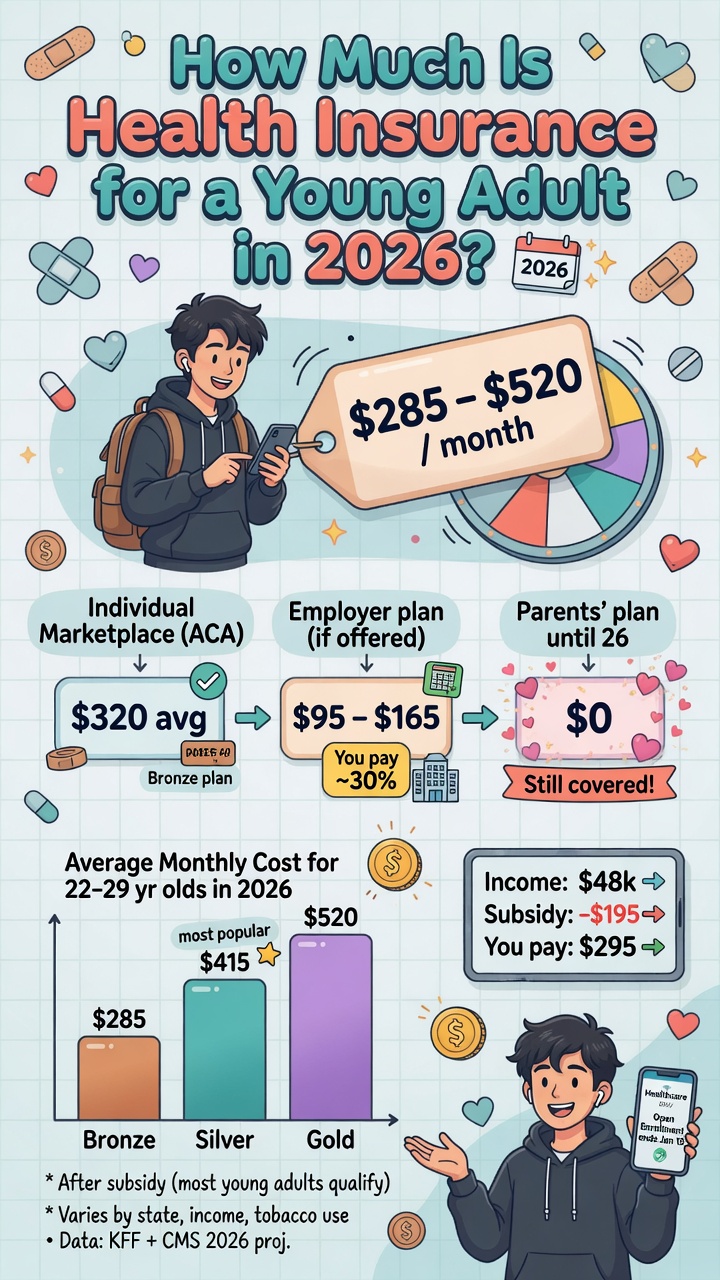

Typical cost for a healthy 25-year-old in Georgia: $200-$350/month for a Silver plan with no subsidy. With subsidy (most young adults qualify), often $50-$150/month.

Subsidy eligibility: if your projected income is between $15,060 and $60,240 (single), you'll likely get help. Above that — the 2026 cliff is back. Below that — you're typically Medicaid-eligible.

Best move for healthy young adults: HSA-eligible HDHP. Lower premium, tax-advantaged savings account, becomes a stealth retirement asset by 65.

What if I just go without? Possible but math is brutal: one ER visit averages $3,000-$15,000 unsubsidized. The risk premium isn't worth it for most.

That's the framework. The rest is the detail.

Why Young Adults Get a Different Pricing Picture

Health insurance is rated by age, location, tobacco use, and family size under ACA rules. For young adults specifically:

Premiums increase ~3-4% per year of age above 21

A 21-year-old's monthly premium is the cheapest. A 30-year-old pays roughly 25-30% more for the same plan.

Smoking adds a tobacco surcharge that varies by carrier (typically 10-50% on top of base premium)

Income matters more than premium for most young adults — subsidies can swing the actual out-of-pocket from $300/month to $40/month for the same plan

The result: most young adults qualify for meaningful marketplace subsidies if they're earning under $60,240 (single in 2026). The math often works out far better than people assume before they actually run their numbers.

The 4 Real Paths When You're Aging Off Your Parents' Plan

You have a 60-day Special Enrollment Period when you turn 26 and lose coverage. Within that window, here are your options:

Stay on your current plan via COBRA for up to 36 months. COBRA at full price is brutal — typically $400-$800/month for a single young adult. Almost never the right answer unless you have an active medical situation you don't want to interrupt.

Get coverage through a new W-2 employer. If you're starting a new job that offers benefits, this is usually the cheapest path because the employer covers 50-80% of the premium. Look at the employer plan first.

Buy your own ACA marketplace plan through Georgia Access. The default for most young adults — especially freelancers, gig workers, or those between jobs. Subsidies often make this surprisingly affordable.

For the full layoff playbook, see I Just Lost My Job in Atlanta.

For the broader Georgia marketplace overview, see Georgia Health Insurance Marketplace: A 2026 Guide

Get on a spouse's employer plan if you're married and your spouse has W-2 coverage. Run the numbers — sometimes cheaper than marketplace.

For most young adults without immediate W-2 employment, Georgia Access marketplace is the default. Read the full Atlanta Health Insurance Buyer's Guide for the broader path framework.

What It Actually Costs in Georgia in 2026

Real numbers for a healthy single 25-year-old non-smoker in metro Atlanta — typical monthly premium for a Silver-tier plan, before and after subsidy:

Income $20,000/year (part-time, side hustle, or just starting out): subsidized to ~$0-$30/month after Premium Tax Credit

Income $30,000/year (full-time entry-level): ~$60-$100/month after subsidy

Income $45,000/year (a few years into your career): ~$150-$220/month after subsidy

Income $58,000/year (close to the cliff): ~$280-$350/month — most subsidy gone

Income $65,000+/year (over the cliff): ~$280-$350/month — full price (no subsidy at all in 2026 since the cliff returned)

Bronze plans run ~30% cheaper monthly but have higher deductibles. Gold plans run ~25% more monthly but have lower deductibles. For most young adults in good health, Silver or Bronze HDHP is the sweet spot.

These are illustrative ranges — your actual cost depends on plan choice, exact age, zip code, and tobacco status. For a real number on your specific situation, a 15-minute conversation with a broker gets you exact quotes within 24 hours.

The HSA Move (If You're Healthy, Read This)

The single most-underrated move for healthy young adults in 2026: enroll in an HSA-eligible high-deductible health plan (HDHP) and max your HSA contributions.

Why this is so good:

Lower monthly premium than non-HDHP plans (often $50-$80/month savings)

2026 HSA contribution limit: $4,400 for self-only coverage — every dollar reduces your taxable income

Triple tax advantage: contributions deductible going in, growth tax-free, withdrawals for qualified medical expenses tax-free

The retirement angle nobody talks about: at age 65, your HSA effectively becomes a traditional IRA. Withdrawals for any reason — not just medical — are subject only to ordinary income tax. Save medical receipts now; withdraw decades of receipts tax-free in retirement.

A 25-year-old who maxes the HSA at $4,400/year for 30 years at 7% return ends up with roughly $415,000 tax-advantaged. That's not a typo.

If you're healthy in your 20s, the HSA is one of the highest-leverage 30-second decisions you can make. Full HSA guide here.

The catch: HDHPs have higher deductibles. If you have ongoing medical needs (chronic conditions, frequent specialist care, expensive prescriptions), the math may not work. Run both scenarios before committing.

"What If I Just Go Without?" — The Risk Math

Some young adults look at $250/month and decide to skip coverage entirely. Let me give you the realistic risk math, not the moralized version:

The federal individual mandate penalty was zeroed out in 2019 — there's no IRS penalty for going uninsured. So legally, you can.

An average ER visit in Atlanta runs $3,000-$5,000 for something simple (sprained ankle, kidney stone, food poisoning). $10,000-$25,000 for something more serious (broken bone needing surgery, appendicitis).

An overnight hospital stay averages $11,000-$15,000 nationally.

A serious accident or unexpected diagnosis (cancer, neurological event, major injury) routinely produces $50,000-$300,000+ in medical bills uninsured.

You can't enroll outside Open Enrollment without a Qualifying Life Event. If you go uninsured and then get sick, you're typically stuck paying out of pocket until November-January Open Enrollment.

The honest verdict: if you can afford $50-$150/month after subsidies, the math overwhelmingly favors having coverage. If you genuinely can't afford that, look at Medicaid (Georgia's expanded) or short-term medical bridge plans.

The "I'll just be careful" plan is the riskiest financial position you can be in for $1,800-$3,600/year of avoided premium.

Common Mistakes I See

The specific mistakes that cost real money or create real problems for young adults:

Missing the 60-day Special Enrollment window after aging off your parents' plan. The clock starts the day coverage ends. Miss it and you wait until November.

Choosing the cheapest premium without checking the network. A plan that's $30/month cheaper but doesn't include your doctor or your nearest hospital is not actually cheaper.

Underestimating subsidy eligibility. Many young adults with $30-50K incomes assume they don't qualify for help. Most do. Run the numbers before assuming.

Skipping the HSA-eligible plan because "the deductible is high." For young adults expecting low medical spending, an HDHP + HSA combo is often net-cheaper AND builds tax-advantaged retirement savings simultaneously.

Going without coverage to "save money." Math almost always loses long-term. One real medical event eliminates years of avoided premium.

Buying short-term plans for long-term coverage. Short-term medical doesn't cover pre-existing conditions, has annual benefit caps, can be canceled. Useful as a 1-3 month bridge; never as a long-term solution.

Forgetting to update Georgia Access mid-year when income changes. If your gig income jumped or fell, your subsidy eligibility changed. Update it before tax time, not after.

What If You're a 1099 Worker / Freelancer / Gig Worker?

If your young-adult income is from 1099 work — Uber, DoorDash, freelance design, side-hustle income — there's a layered post specifically for you: Health Insurance for Gig Workers in Georgia. It covers:

How to project your MAGI when income is variable

The self-employed health insurance deduction (100% of premiums tax-deductible)

Multi-platform income tracking

The 2026 subsidy cliff specifically for high-earning gig workers

For most 1099 young adults, the marketplace + HSA combo wins decisively when you account for the tax deduction. The math is even better than for W-2 employees in your same age and income range.

For traveling healthcare work specifically: Health Insurance for Travel Nurses.

Real estate agent specifically: Health Insurance for Real Estate Agents.

Want a Real Number for Your Situation?

If you want an actual quote for your specific situation in Georgia — not a generic range — text me at (706) 988-1930 with:

Your age

Atlanta-area zip code (or wherever you're located in Georgia)

Projected 2026 income (if 1099, your net after expenses, not gross)

Whether you smoke

Any prescriptions or doctors you want to keep

I'll come back inside 24 hours with 2-3 real plan options at real prices, after subsidy. Free, independent broker, no follow-up sequence.

I'm 27 myself — I genuinely understand the audience here. Most of my clients are young adults navigating this for the first time. The marketplace looks intimidating from the outside; it's actually pretty manageable once you know which levers to pull.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn.

This post is general education, not medical, tax, or legal advice. Insurance pricing, subsidy eligibility, and rules change.