HSA Contribution Limits 2026: How to Actually Use Them

Author: Justin Bishop · May 2, 2026 · 7 min read

If you're enrolled in an HSA-eligible high-deductible health plan in 2026, you have access to the most tax-advantaged account in the entire U.S. tax code. Triple tax advantage. No "use it or lose it." Becomes a stealth retirement account at 65. And in 2026 specifically — with the ACA subsidy cliff back at 400% of the federal poverty level — HSAs do something extra important for self-employed Georgians: every dollar you contribute reduces your MAGI, which can keep you on the marketplace subsidy.

Most people don't max out their HSA. Many don't even invest the balance. And some accidentally disqualify themselves from contributing at all by enrolling in an FSA or Medicare on the side.

I'm Justin Bishop, an independent broker in Atlanta. I write a lot of HSA-eligible plans for self-employed clients. Here are the actual 2026 numbers, who qualifies, and the four strategic moves most people miss.

The 30-Second Version

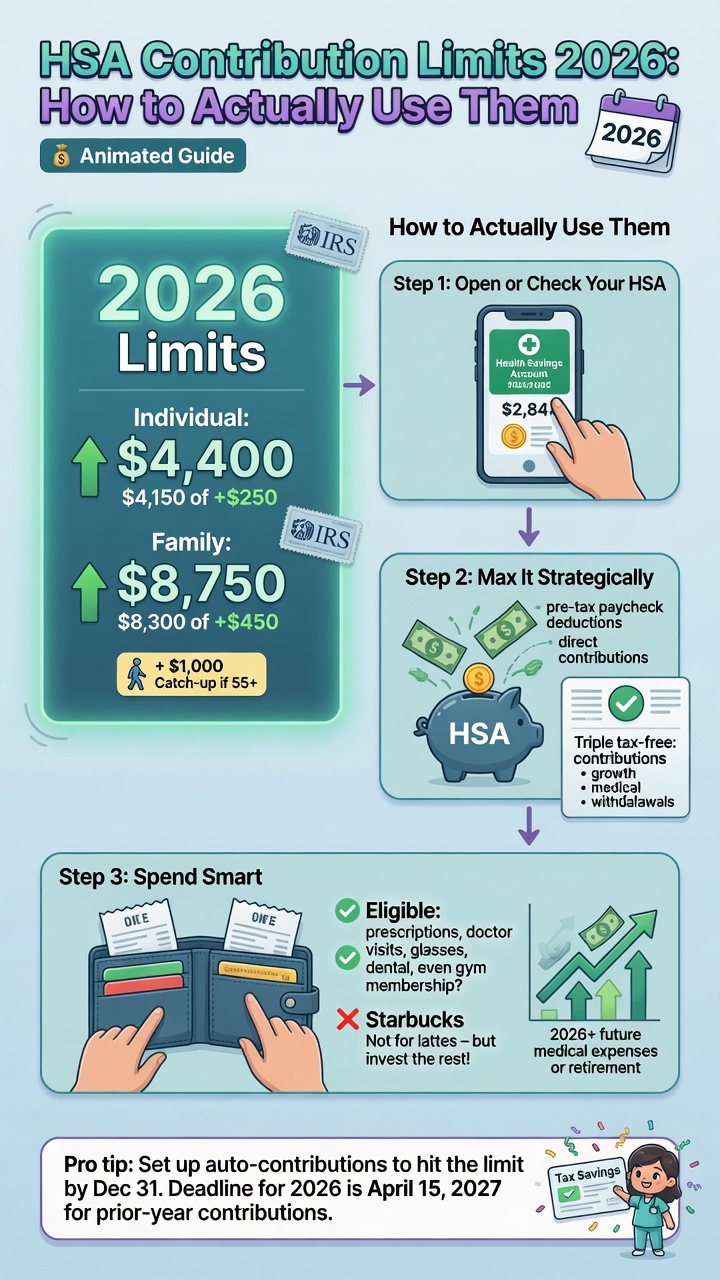

Self-only HDHP: contribute up to $4,400 in 2026

Family HDHP: up to $8,750

Age 55+: add a $1,000 catch-up contribution

Deadline: April 15, 2027 (next year's tax filing day) to make 2026 contributions

Triple tax advantage: deductible going in, tax-free growth, tax-free withdrawals for qualified medical expenses

After age 65: withdrawals for any reason — only ordinary income tax, no penalty

Strategic angle for self-employed Georgians in 2026: HSA contributions reduce your MAGI, which can keep you under the ACA subsidy cliff at 400% FPL

That's the core. The rest of this post is the detail.

For the broader landscape of affordable Georgia coverage paths, see Affordable Health Insurance Options in Georgia for 2026.

The Actual 2026 Limits

These are the numbers you came here for. Set by the IRS, updated annually for inflation:

Self-only HDHP coverage: $4,400 (up from $4,300 in 2025)

Family HDHP coverage: $8,750 (up from $8,550)

Catch-up contribution at age 55+: additional $1,000 (this number doesn't index for inflation — has been $1,000 since the rule was created)

Total possible if 55+ on family coverage with spouse 55+: $8,750 + $1,000 + $1,000 = $10,750 (the second catch-up has to go in your spouse's separate HSA — not yours)

Deadline for 2026 contributions: April 15, 2027 (you get until next year's tax filing day to put money in for the current year)

If your employer contributes to your HSA, that money counts toward the limit. The limit is total contributions to your HSA from all sources combined — not just yours.

Who Qualifies — The HDHP Requirement

You can only contribute to an HSA if you're enrolled in an HSA-eligible high-deductible health plan (HDHP). The IRS sets specific rules each year for what counts:

2026 minimum HDHP deductible: $1,650 self-only / $3,300 family

2026 max out-of-pocket on the HDHP: $8,300 self-only / $16,600 family

For the broader marketplace tier comparison (and why HDHP/HSA usually means Bronze), see Bronze vs Silver vs Gold: Which Plan Do You Actually Need?

No first-dollar coverage — the plan can't pay for non-preventive care before you hit the deductible (preventive services like annual physicals can be covered before deductible)

What can disqualify you from contributing even if you have an HDHP:

Being enrolled in Medicare (Part A, B, C, or D — any of them disqualifies). This trips up a lot of people who turn 65 mid-year.

Having a general-purpose Health FSA through your spouse's employer

Being claimed as a dependent on someone else's tax return

Having other non-HDHP health coverage (e.g., a spouse's traditional plan that also covers you)

Being enrolled in TRICARE or VA benefits within the last 3 months (with some exceptions)

The "other coverage" rules are stricter than most people realize. If you have any traditional health coverage on the side — even a spouse's plan you don't actively use — you may not be HSA-eligible.

The Triple Tax Advantage (and Why It's Underrated)

There's no other account in the U.S. tax code that does all three of these:

Tax-deductible going in — Contributions are above-the-line deductions on your federal taxes (Form 8889). For self-employed people, this happens via Schedule 1. No itemizing required.

Tax-free growth — Money inside the HSA grows without capital gains, dividend, or interest taxes. If you invest it in mutual funds (which most modern HSAs allow), the growth compounds untaxed.

Tax-free withdrawals for qualified medical expenses — Doctor visits, prescriptions, dental, vision, hearing aids, mental health, and a long list of other qualified expenses come out tax-free at any age.

Compare to a traditional 401(k) (taxed on withdrawal) or a Roth IRA (taxed going in). HSAs combine the best of both — and one feature neither has.

The kicker: at age 65, the HSA effectively becomes a traditional IRA. Withdrawals for any reason — not just medical — are subject only to ordinary income tax, no penalty. Save your medical receipts over the years and you can withdraw decades' worth of receipts tax-free in retirement to cover anything else you're spending money on.

This is why finance writers call the HSA "the stealth retirement account."

Why HSAs Matter More in 2026 Than They Did in 2025

This is the angle most people miss in 2026.

The federal enhanced premium tax credits expired December 31, 2025. As of January 1, 2026, the ACA subsidy cliff is back at 400% of the federal poverty level. Earn $1 over the cliff for your household size — roughly $60,240 single, $124,800 family of four — and you lose all premium tax credits.

But your "income" for ACA subsidy eligibility isn't your gross. It's your MAGI (modified adjusted gross income). And HSA contributions reduce your MAGI dollar for dollar.

Here's how that plays out for a self-employed person near the cliff:

A consultant with $65,000 of net self-employment income is over the single cliff and would lose all subsidies — paying full freight on a marketplace plan

That same consultant maxes the HSA at $4,400 for the year

Their MAGI drops to $60,600 — back under the cliff

They keep their premium tax credit, which might save $3,000–$8,000+ per year depending on plan choice

The $4,400 going into the HSA is also tax-deductible — saving roughly $1,000 in federal income tax at a 22% bracket

Net effect: a $4,400 HSA contribution that the consultant gets back in tax savings AND keeps them eligible for thousands in subsidy

I covered the broader strategy in the 2026 subsidy cliff post. The HSA is one of the five levers I described there. It's often the cheapest one to pull.

Specific to gig workers: Health Insurance for Gig Workers.

4 Strategic Moves Most People Miss

The contribution limits are the easy part. These are the moves that separate "I have an HSA" from "my HSA is doing real work":

The Last-Month Rule. If you're HSA-eligible on December 1 of the year, the IRS lets you contribute the full annual amount — even if you only had HDHP coverage for one month. Catch: you have to stay HSA-eligible for the entire following year (the "testing period") or you owe taxes plus penalties on the prorated portion. Useful when you switch to an HDHP late in the year.

Mid-year coverage changes. Marriage, divorce, having a baby, or moving from family to self-only coverage all change your contribution limit. The IRS uses a per-month formula based on which coverage you had each month. If your situation changed mid-year, your limit isn't a flat number — it's prorated. Most people miss this and either over-contribute (penalty) or under-contribute (lose tax savings).

Catch-up contributions at 55. The $1,000 catch-up is per HSA owner, not per household. If you're 55+ and your spouse is 55+ and you both have HDHP coverage, you can each contribute a catch-up — but they have to go in separate HSAs. You can't double-stuff one HSA with both catch-ups.

Invest the balance. Most HSAs let you invest funds above a minimum cash threshold (usually $1,000-$2,000) into mutual funds. The default is to leave everything as cash earning ~0%. Switching to investments compounds the triple tax advantage over decades. A $4,400/year contribution invested in a moderate-growth fund for 30 years can become $400,000+ tax-free for medical or retirement expenses.

Common Mistakes I See

I've watched these specific mistakes cost real clients real money:

Contributing while on Medicare. Even Medicare Part A — the part you get free at 65 — disqualifies you from HSA contributions. Many people enroll in Part A automatically when they file for Social Security and don't realize their HSA eligibility ended that day. Penalty: 6% excise tax per year on the excess, until you withdraw it.

Forgetting employer contributions count toward the limit. If your employer puts $1,500 into your HSA, you can only contribute $2,900 yourself (self-only) before hitting the $4,400 limit. People often see "I get $1,500 from work" and contribute the full $4,400 themselves — over-contribution penalty applies.

Withdrawing for non-qualified expenses before 65. Pulling out $1,000 to pay for a vacation costs you ordinary income tax PLUS a 20% penalty. After 65, only ordinary income tax — but before 65, that penalty bites hard.

Not investing the balance. Most HSAs default to cash. Cash earns ~0% interest and gets eroded by inflation. Switching to a target-date fund or index fund inside the HSA (most providers offer this — sometimes there's a small admin fee or threshold) is one of the highest-leverage 30-second decisions in personal finance.

Forgetting to claim the deduction at tax time. Self-employed contributions go on Form 8889 plus Schedule 1. The deduction can be missed if your CPA isn't paying attention. Worth bringing up explicitly.

Want to Run the Math for Your Situation?

If you're self-employed in Georgia and trying to figure out whether an HSA-eligible HDHP makes sense for you in 2026 — especially if you're near the subsidy cliff — text me your projected MAGI and household size at (706) 988-1930. I'll come back with whether you'd qualify, what the contribution math looks like, and which specific HDHP plans on Georgia Access are HSA-eligible for your zip code.

15 minutes. Free. Independent.

I help self-employed Georgians, Atlanta freelancers, and small business owners maximize the marketplace every week. The HSA is one of the most under-used tools in the toolkit — happy to walk you through it.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn.

This post is general education, not tax or legal advice. Marketplace platforms, carriers, and federal rules change.