Health Insurance for Travel Nurses: The Agency Plan Trap

Author: Justin Bishop · May 4, 2026 · 7 min read

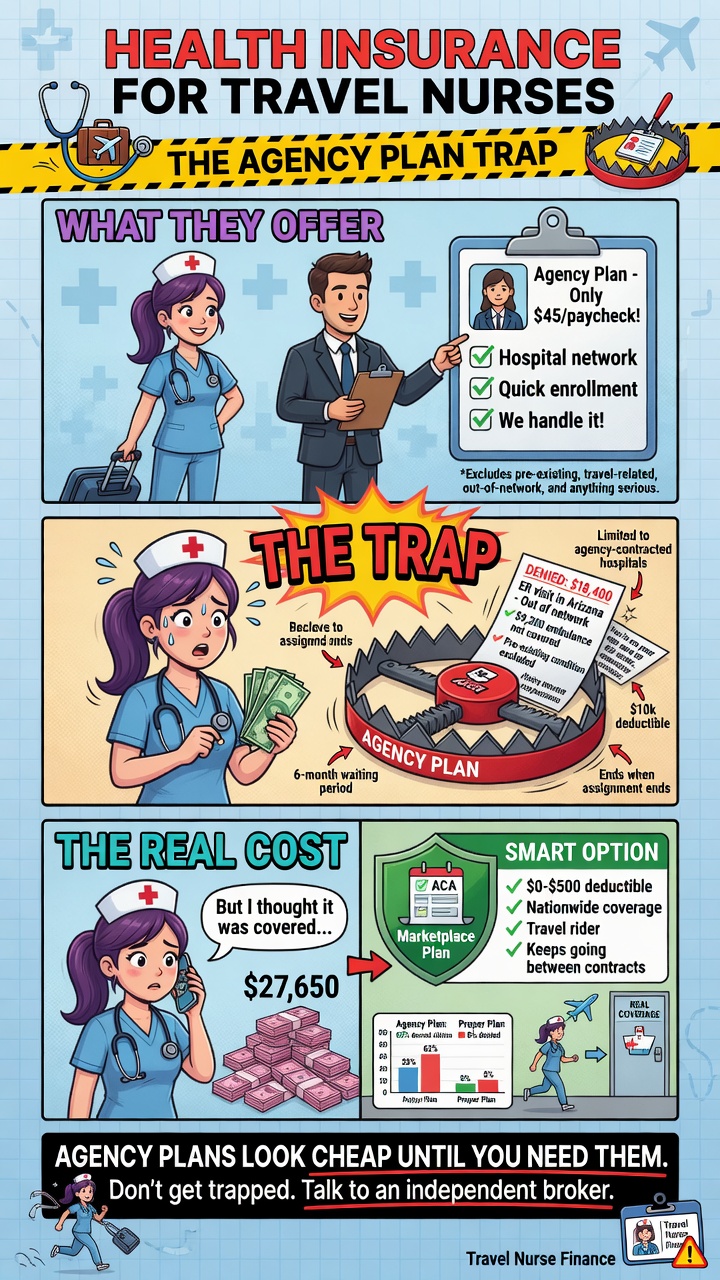

If you're a travel nurse, your agency probably offered you health insurance when you signed your contract. The premium looked manageable, the recruiter said it was "industry standard," and you signed up because — well, you needed coverage. Then, three weeks into your assignment, you went to a doctor and found out your network doesn't include your current city. Or your contract ended and your insurance ended with it. Or your premium quietly went up at renewal.

Here's the honest broker take: agency-provided travel nurse insurance is almost never the best option. Not because agencies are bad, but because the structure of the agency plan rarely fits how travel nurses actually live and work — across states, between contracts, often earning above the subsidy cliff but treated like a W-2 employee for benefits purposes.

I'm Justin Bishop, an independent broker in Atlanta, licensed in 31 states. That last detail matters more than usual for travel nurses — most brokers are licensed in one or two states. I work with travel nurses regularly because the multi-state coverage question is the central problem in this space, and a single-state broker can't fully solve it.

Here's the framework I walk travel nurse clients through.

For real estate agents (also 1099): Health Insurance for Real Estate Agents

The 30-Second Version

Most travel nurse agency insurance plans have narrower networks than open-market plans — often regional rather than national

Agency insurance typically ends when your contract ends — creating coverage gaps between assignments

Travel nurse income is usually high enough to lose marketplace subsidies in 2026 (the cliff returned at $60,240 single MAGI), making the math more interesting than for typical W-2 employees

Open-market PPO plans with national networks often beat agency offerings on both price AND coverage for traveling work

A multi-state-licensed broker is meaningfully better than a single-state broker for this audience — make sure yours is licensed wherever you take assignments

That's the framework. The rest is the why.

Why Agency Insurance Usually Underperforms for Travel Nurses

The structural problems with agency-offered travel nurse insurance:

Network limitations. Agency plans are typically priced for the average travel nurse staying within a regional network. If you take an assignment in a city not in that network, you're paying out-of-network rates for routine care — sometimes 2-3x what you'd pay in-network.

Coverage tied to contract duration. Most agency insurance is "active during your contract" — meaning the day your assignment ends, your coverage ends. If your next contract starts 3 weeks later, you're uninsured for 3 weeks (or paying COBRA at full price).

Premium per pay period vs total annual cost. Agency plans typically deduct premium from your weekly paycheck. The number looks small ($150/week, $200/week) but the annual total often exceeds open-market pricing.

Stipend/income misclassification at benefits time. Some agencies count tax-free stipends as "income" for benefit eligibility, others don't — leading to inconsistent treatment when you change agencies.

Limited dental, vision, and ancillary coverage in many agency plans — or these are bundled in ways that make them hard to evaluate separately.

Carrier choices baked in by the agency. You can't shop carriers — you take whoever the agency has contracted. For an open-market plan, you compare 4-6 carriers and pick the best fit.

The combination is often: higher real cost, narrower network, gaps between contracts, less control. That's the "agency plan trap."

The 4 Real Paths to Health Insurance for Travel Nurses

Here are the actual options:

Path 1: Agency-provided insurance. Default option. Sometimes the right answer for short-term assignments where the network coincidentally matches your work locations. More often than not, NOT the best deal.

Path 2: ACA marketplace plans (state-specific). Best for travel nurses with relatively stable income and base location. You enroll through your "tax home" state's marketplace. Continues across all your assignments since marketplace plans don't end when contracts end.

Path 3: National PPO plans (open market). Many carriers offer plans with national networks — Blue Cross, UnitedHealthcare, Aetna, Cigna. You buy directly or through a broker. Network covers you in most US cities. Usually the best fit for high-mobility travel nurses.

Path 4: Spouse's employer plan. If you're married and your spouse has W-2 coverage with national network access, this is often the cheapest path overall.

For most travel nurses, Path 3 (national PPO) wins when you account for network breadth, contract continuity, and total annual cost. Path 2 (ACA marketplace) is the right answer when your income is below $60,240 single (and you qualify for subsidy) AND your assignments are within your home state's network.

The Multi-State Network Reality

Travel nurse contracts span multiple states in a typical year. Here's how the major carriers handle this:

Blue Cross Blue Shield — best in this category because of the "BlueCard" national network. A BCBS Georgia plan, for example, gives you access to in-network rates with BCBS plans in every other state. Strong fit for travel nurses based in Georgia who take assignments nationally.

UnitedHealthcare PPO — solid national network, generally accepted at major hospital systems in metro areas across the US. Less flexible than BCBS in rural areas.

Aetna PPO — competitive national coverage, sometimes better pricing than BCBS for younger nurses with limited medical history.

Cigna PPO — good national network, often priced aggressively for individual market plans.

Kaiser — rarely a good fit for travel nurses because it's limited to specific metro areas with Kaiser facilities. Skip unless 100% of your assignments are in Kaiser markets.

Ambetter / regional HMOs — typically worse fit due to narrow networks. Avoid for traveling work.

The right carrier for you depends on which states you take assignments in, but BCBS PPO plans are the default starting point for most travel nurses I work with.

The 2026 Subsidy Cliff for Travel Nurses

The federal premium tax credits enhanced under the IRA expired December 31, 2025. As of January 1, 2026, the subsidy cliff is back at 400% of the federal poverty level — about $60,240 for a single person, $81,760 for a couple, $124,800 for a family of four.

Why this hits travel nurses hard:

Travel nurse base salaries are typically $50,000-$80,000 — many travel nurses are right at the cliff

Tax-free stipends (housing, meals, incidentals) often add $20,000-$40,000 to total compensation but typically aren't counted in MAGI for marketplace purposes (since they're non-taxable)

Overtime and shift differentials push taxable income up

Travel nurses with strong utilization (80+ hours/week, top-paying assignments) can hit $120,000+ taxable income and lose all subsidy access

If your projected MAGI is under $60,240 single, marketplace + subsidy is usually the cheapest path. If you're over the cliff, off-marketplace national PPO plans become more attractive because you're paying full freight on the marketplace anyway.

The strategic levers travel nurses can pull to manage MAGI:

Solo 401(k) or SEP-IRA contributions if you're 1099 (tax-deductible, reduces MAGI)

HSA contributions if enrolled in an HSA-eligible HDHP

Self-employed health insurance deduction if you're 1099 (100% deductible)

Timing of stipend vs taxable wage in your contract negotiation

Bridging Gaps Between Contracts

The single most underrated travel nurse insurance challenge: the gap between assignments.

If your contract ends April 30 and your next one starts May 21, you have 3 weeks of "what about insurance?" Three options:

Stay enrolled in your marketplace or open-market plan continuously. Doesn't end when contracts end. Easiest answer if you're already on Path 2 or 3.

COBRA from the previous agency's plan. Federal COBRA gives you up to 36 months — but the cost is the full unsubsidized premium plus a 2% admin fee. Often $700-$1,200/month for a single person. Brutal.

Short-term medical insurance. Cheap monthly premium ($60-$200/month for a young, healthy nurse) but NOT ACA-compliant — doesn't cover pre-existing conditions, has annual benefit caps, can be canceled. Useful as a 1-3 month bridge ONLY when you have no other options.

For travel nurses who take regular assignments, a continuous marketplace or open-market plan is dramatically better than the COBRA-or-short-term-bridge approach. You set up coverage once, and it runs forever — across all your contracts and gaps.

What to Look For in a Travel Nurse Health Plan

Before you sign onto any plan (agency or open-market), check these:

Network reach. What hospitals and providers are in-network in the states/cities you'll take assignments? Plug specific zip codes into the carrier's "find a doctor" tool before enrolling.

Out-of-network coverage. PPO plans typically cover some out-of-network care; HMO plans typically don't. For traveling work, you need PPO unless you'll only be in HMO network states.

Annual deductible vs out-of-pocket maximum. What you'd pay in a worst-case medical year.

Telehealth access. For traveling work, virtual care is invaluable. Most modern plans include it; verify.

Coverage when you cross state lines. Some plans treat out-of-state care differently. Read the policy specifically on multi-state utilization.

Plan year vs contract year. Plan year typically Jan 1 - Dec 31. Doesn't depend on your contract start/end dates.

Pre-authorization requirements. Some plans require pre-auth for non-emergency care. For traveling work, complicated pre-auth is friction.

Common Mistakes I See

The specific errors I watch travel nurse clients make:

Default-accepting the agency's insurance without comparing. Even 30 minutes of comparison reveals whether it actually fits your situation.

Choosing HMO over PPO because the premium is lower. Saves you $40/month, costs you $4,000 when you need care outside the network during an assignment.

Letting coverage lapse between contracts thinking nothing will happen. One ER visit during an uninsured gap can wipe out a year of contract income.

Not factoring tax-free stipends correctly. They affect compensation negotiation but typically don't affect MAGI for marketplace eligibility — many travel nurses get this backwards.

Buying short-term medical for long-term coverage. Useful as a bridge; never as a primary plan. Pre-existing condition exclusions are brutal.

Working with a single-state broker. They can quote Georgia plans but can't help you when you take an assignment in Texas or Colorado. A multi-state broker fits this audience.

A Real Travel Nurse Client Said It Best

"Best Health Insurance rep in the biz! Beat the snot out of the travel nurse insurance I was offered by my employer!" — Ava R., Atlanta, March 2026

That's a real review from a travel nurse client on our reviews page. Her situation isn't unique — most travel nurses I work with end up with better coverage at lower total cost when we shop the open market vs. taking the agency's default.

Want a Real Quote for Your Travel Nurse Situation?

If you want to compare your agency's offering against the open-market alternatives, the fastest path is to text me at (706) 988-1930 with:

Your "tax home" state (where you file)

States where you typically take assignments (top 3-4)

Your projected 2026 MAGI (taxable wages, NOT including tax-free stipends)

Whether you have any ongoing medical needs or prescriptions

What your agency's current plan offer is (premium + carrier name if you have it)

I'll come back inside 24 hours with a side-by-side comparison: 2-3 open-market PPO options vs your agency's plan, with real network analysis for the cities you actually work in.

Free. Independent. Licensed in 31 states — meaning I can help you regardless of where your next assignment takes you.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not medical, tax, or legal advice. Travel nurse compensation structures, agency insurance terms, and marketplace rules vary.