What Health Insurance Should Atlanta Restaurants Offer?

Author: Justin Bishop · May 29, 2026 · 10 min read

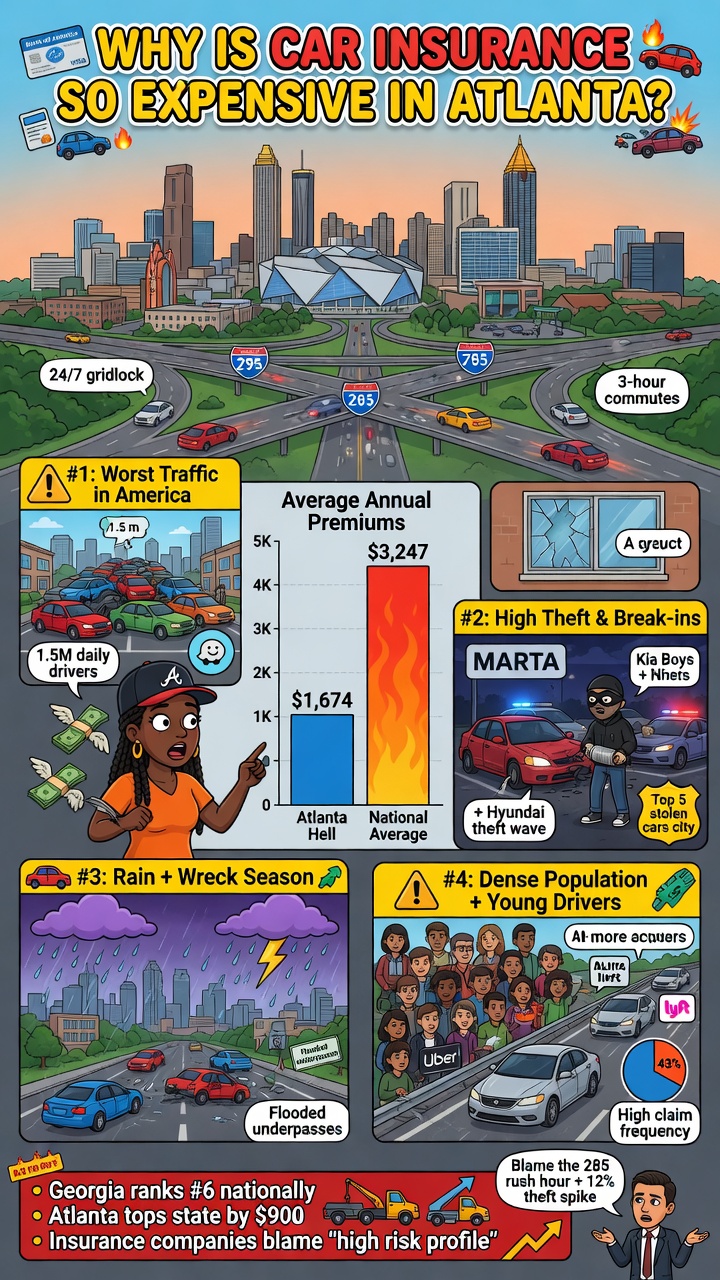

If you've lived in Atlanta long enough to renew an auto insurance policy, you already know: the bill keeps going up, and nothing you do seems to slow it down. You drive carefully. You haven't filed a claim. Your car's the same one you've had for years. And yet your premium is hundreds — sometimes thousands — more than what your cousin in Nashville or Indianapolis pays for nearly identical coverage.

It's not your imagination, and it's not your fault. Atlanta sits at #4 on the national list of most-expensive metros for auto insurance. The average driver here pays roughly $2,400–$2,800/year for full coverage — about 40% more than the U.S. average. And it's not because Georgia drivers are uniquely reckless. It's because eight structural factors stack on top of each other to push every Georgia auto premium up, whether you've contributed to the risk or not.

This post walks through every reason your rate is what it is, what specifically is driving each one in 2026, the comparison to other major U.S. metros, and the four things you can actually control to bring your premium down.

I'm Justin Bishop, an independent broker in Atlanta. I shop auto coverage across 10-15 carriers for Atlanta clients every week. Here's the honest breakdown.

The 30-Second Version

Atlanta sits at #4 on the national list of most-expensive metros for auto insurance — roughly 40% above the U.S. average

Not because of driver behavior — because of 8 stacked structural factors specific to metro Atlanta and Georgia state law

The big ones: top-10 traffic congestion, 12% uninsured driver rate, top-20 theft metro, severe weather (hail), one of the worst tort/lawsuit environments in the country, rising repair costs, severe-injury accidents on Atlanta interstates, and Georgia's legal use of credit-based scoring

You can't change the ZIP code, the weather, or the tort environment

You can control: reshopping every 12-24 months, bundling home + auto, raising deductibles, and refusing to drop uninsured motorist coverage

The biggest mistake Atlanta drivers make: buying the state minimum 25/50/25 because it's cheap. Georgia's tort environment makes this a financial trap for anyone with assets to protect.

Reason #1 — Atlanta Traffic Is Among the Worst in America

According to the INRIX Global Traffic Scorecard, Atlanta consistently ranks in the top 10 most congested U.S. cities, and the metro logs some of the longest commute times in the Southeast.

More cars on more roads for more hours equals more accidents. And insurers price by ZIP code based on accident frequency. If you live inside I-285 — especially in Buckhead, Midtown, Brookhaven, Decatur, or anywhere along I-75/85 — you're paying for that risk whether or not you ever cause a crash.

What this means for your rate: A driver with a clean record in suburban Cherokee County will pay materially less than the same driver living in 30309. The car didn't change. The ZIP code did.

Reason #2 — Georgia Has One of the Highest Uninsured Driver Rates in the Country

Roughly 1 in 8 Georgia drivers (about 12%) drive without insurance, per Insurance Research Council data.

That matters because when an uninsured driver hits you, your own uninsured/underinsured motorist coverage pays the claim — not theirs. Insurance carriers price that risk into every Georgia policy, even for drivers who never personally encounter an uninsured motorist.

Atlanta-specific impact: the uninsured rate is concentrated in metro Atlanta, which pushes premium higher inside I-285 than in rural Georgia.

If you don't carry uninsured motorist coverage, you're paying for everyone else's risk without protecting yourself. Read Should I Get Liability or Full Coverage for My Car in Atlanta? for the full breakdown on what UM/UIM actually covers.

Reason #3 — Vehicle Theft Rates in Metro Atlanta Are High

Atlanta consistently ranks in the top 20 metros for auto theft nationally. Kia and Hyundai theft surged dramatically in 2023–2024 due to the well-documented security vulnerability, and Atlanta was one of the hardest-hit metros. Catalytic converter theft compounds the issue.

If your car is covered for theft, you're paying comprehensive premium against a real, measurable risk. If you drive a 2011–2022 Kia or Hyundai, expect to see this priced in heavily until carriers cycle through the new pricing models.

Reason #4 — Georgia Weather Drives Comprehensive Claims

Tornadoes, hail, severe thunderstorms, and flooding all generate comprehensive claims, and Georgia gets all four.

Hail damage alone is one of the largest single-event claim drivers for Georgia auto insurers. A single hailstorm in metro Atlanta can generate hundreds of millions of dollars in claims across a single afternoon. Insurers price that volatility into every Georgia comprehensive premium.

Reason #5 — The Georgia Lawsuit Environment (and Nuclear Verdicts)

This is the one most drivers don't know about.

Georgia is consistently ranked one of the worst "judicial hellholes" in the U.S. by the American Tort Reform Foundation. The state has produced repeated nuclear verdicts — single auto-related lawsuits resulting in $10M+, $50M+, even $100M+ jury awards in recent years.

Even if 99% of accidents settle for far less, insurers must price the tail risk — the small chance that any given claim could turn into a multi-million-dollar verdict. That tail risk gets priced into every Georgia auto policy.

This is why higher liability limits are not optional in Atlanta. The state minimum (25/50/25) is a financial trap. See Should I Get Liability or Full Coverage for My Car in Atlanta? for the limit recommendations.

Reason #6 — Repair Costs Are Climbing Fast

The cost to fix a damaged car has risen sharply over the last 5 years for three compounding reasons:

Modern vehicles have more sensors, cameras, and computer modules — a fender bender on a 2022 vehicle now involves recalibrating ADAS systems, which adds thousands to repair bills

Parts shortages and supply chain disruptions lingering from 2020–2023

EV repair costs run 30–40% higher than comparable gas vehicles, and EV adoption in Atlanta is climbing

Higher repair costs = higher claim payouts = higher premiums for everyone.

Reason #7 — Atlanta Has a High Rate of Severe-Injury Accidents

Insurance Institute for Highway Safety data shows Atlanta-area interstates have higher-than-average rates of severe and fatal accidents — driven by speed differentials, merge-heavy interchanges (the Connector, Spaghetti Junction, Tom Moreland), and high commercial truck traffic.

Severe-injury claims are far more expensive than property-damage-only claims. When your metro produces more of them, your bodily-injury premium reflects that.

Reason #8 — Credit-Based Insurance Scoring (Still Legal in Georgia)

Most states allow insurers to use a credit-based insurance score as part of pricing. Georgia is one of them.

This means a driver with a clean record and excellent credit can pay 30–50% less than the same driver with poor credit — for the exact same coverage on the exact same car. California, Hawaii, Massachusetts, and a few others have banned this. Georgia hasn't.

This is one of the biggest hidden levers on your rate. If your credit has improved meaningfully in the last 2 years, you should reshop your auto insurance.

So Why Is Atlanta More Expensive Than Other Cities?

Atlanta isn't expensive because of one thing. It's expensive because of all eight stacked together:

High traffic and high accident frequency

High uninsured driver rate

Top-20 theft metro

Severe weather exposure

One of the worst tort environments in the country

Rising repair costs

High-severity interstate accidents

Credit-based scoring (legal here)

Cities like Boston look surface-similar on traffic, but Atlanta's tort environment and uninsured-driver rate are what really push it past Northeast metros. Cities like Detroit are higher than Atlanta because Michigan's no-fault system is uniquely expensive. Atlanta sits at #4 nationally — and it's earned it.

What You Can Actually Do About It

You can't change the ZIP code on your insurance application (well, you can — by moving — but most people don't want that conversation). You can control these four levers:

1. Reshop every 12–24 months. Insurance carriers re-price their risk models constantly. The cheapest carrier for you 3 years ago is rarely the cheapest carrier today. Independent brokers can compare 10–15 carriers in one call — captive agents (State Farm, Allstate, etc.) can only show you their own.

2. Bundle home + auto. Most carriers give 15–25% off auto premium if you bundle homeowners or renters. If you own a home and you're not bundling, you're leaving money on the table. See What Is an Umbrella Policy? for the related bundle math.

3. Raise your deductibles. Moving from $250 to $1,000 on comprehensive and collision typically saves 15–25% on those line items. Just make sure the higher deductible is money you could actually pay out of pocket without disrupting your life.

4. Don't skip uninsured motorist coverage. This is the one Atlanta drivers cut to save money — and it's the worst place to cut. With 1 in 8 Georgia drivers uninsured, UM/UIM is the coverage you're statistically most likely to use. Drop your collision before you drop UM.

The One Mistake Atlanta Drivers Make Most

They buy the state minimum (25/50/25) because it's cheap, then they get hit by an at-fault driver causing $80,000 in medical bills and find out the hard way that they're personally liable for the $30,000 gap.

In Georgia, the state minimum is a financial trap. 100/300/100 with $1M umbrella is the realistic Atlanta baseline for any household with assets (a paid-off car, retirement savings, a home, future earning power).

The whole umbrella math is broken down in What Is an Umbrella Policy?.

Common Mistakes Atlanta Drivers Make Beyond the Minimum-Limits Trap

Patterns I see weekly:

Not reshopping after credit improves. Credit-based scoring drops your rate when your score climbs. Most drivers never reshop after paying off debt or graduating from school.

Auto-renewing with the same carrier for 5+ years. The cheapest carrier rotates every 2-3 years as risk models change. Loyalty discounts rarely cover what you'd save by switching.

Dropping uninsured motorist to save $15/month. In a state where 12% of drivers are uninsured, this is statistically the coverage you're most likely to use. Cut elsewhere.

Carrying low liability limits "because the car is paid off." Liability protects YOU from being sued. It has nothing to do with your car's value. Georgia's nuclear-verdict environment makes 100/300 the realistic floor for any household with assets.

Buying minimal comprehensive on a 2011-2022 Kia or Hyundai. Theft risk on these models is concentrated and material. The "I don't need theft coverage" gamble looks bad fast.

Not bundling because you "got a great deal" years ago on standalone auto. Reshopping bundled at renewal almost always wins now.

Frequently Asked Questions

Will my rate go down if I move outside I-285? Usually yes — sometimes significantly. ZIP code is one of the biggest single rating factors. A driver moving from 30309 (Midtown) to 30075 (Roswell) often sees 15–25% off the same policy.

Does my credit really affect my car insurance rate in Georgia? Yes. A "credit-based insurance score" (different from your FICO, but related) is used by most carriers. Improving your credit by 100+ points can save you 20%+ on auto premium. Reshopping after major credit improvements is one of the highest-ROI moves.

Why does my premium go up when I haven't filed a claim? Three main reasons: your carrier raised rates across your ZIP code because regional losses went up, parts and repair costs are climbing industry-wide, and your credit-based score may have moved. None of these are personal — but they all hit your bill.

How much can an independent broker really save me? It varies. If your current carrier happens to be the cheapest for your specific situation, an honest broker will tell you that. More often, comparing 10–15 carriers turns up a better fit by 15–40%. The shopping is free.

Is teen driver coverage really that expensive? Adding a 16-year-old to a policy in metro Atlanta often doubles the household premium. Crash data justifies it — teens crash at multiples of the adult rate. There are real ways to reduce it (good-student discounts, driver-training discounts, restricting which vehicle they drive), but the structural cost is real.

Can I get a lower rate by switching to a different carrier mid-policy? Yes. There's no penalty for canceling mid-policy — your old carrier issues a prorated refund. Set the new policy's effective date to match your old cancellation date so there's no coverage gap.

Are usage-based / telematics programs worth it? For most safe drivers, yes — discounts of 15-30% are common. The trade-off is letting the carrier monitor your driving via app or device. If you brake hard, drive late at night, or commute long distances, telematics can sometimes raise your rate. Read terms before opting in.

What's the cheapest carrier in Atlanta in 2026? There isn't one. The cheapest carrier for your specific demographic, vehicle, ZIP, and credit profile rotates. Anyone telling you "X carrier is always cheapest in Atlanta" is selling something. The actual answer comes from running quotes.

The Bottom Line

Atlanta is the 4th most expensive metro in the U.S. for car insurance because eight structural factors stack on top of each other. You can't change the ZIP code, the weather, or the tort environment — but you can control four things: who you buy from, how you bundle, where you set deductibles, and which coverages you refuse to drop.

If you haven't reshopped in 18+ months, you're almost certainly overpaying. Independent brokers compare 10–15 carriers in a single call, no obligation. Reach out and let's see what the market actually looks like for your situation.

Want to keep reading? Check out How Much Does Car Insurance Cost in Atlanta in 2026?, Should I Get Liability or Full Coverage for My Car in Atlanta?, or What Is an Umbrella Policy? — all parallel Atlanta driver decisions.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal or financial advice. Auto insurance rates, Georgia tort law, credit-based scoring rules, and carrier underwriting criteria change.