Should I Get Liability or Full Coverage for My Car in Atlanta?

Author: Justin Bishop · May 20, 2026 · 8 min read

Every Atlanta car owner eventually faces the same question: do I really need full coverage, or can I save money with liability-only? The premium difference is real — $1,000-1,500 per year for most drivers. The exposure difference is also real — one accident on liability-only and you could be out the entire value of your car.

The right answer isn't universal. It depends on what your car is worth, whether you have a loan, what you could absorb out-of-pocket, and how you drive in Atlanta. This post walks through the actual math, the specific scenarios where each one wins, and the coverages most Atlanta drivers should add regardless of which path they pick.

I'm Justin Bishop, an independent broker in Atlanta. I write auto insurance across multiple carriers weekly. Here's the honest breakdown.

The 30-Second Version

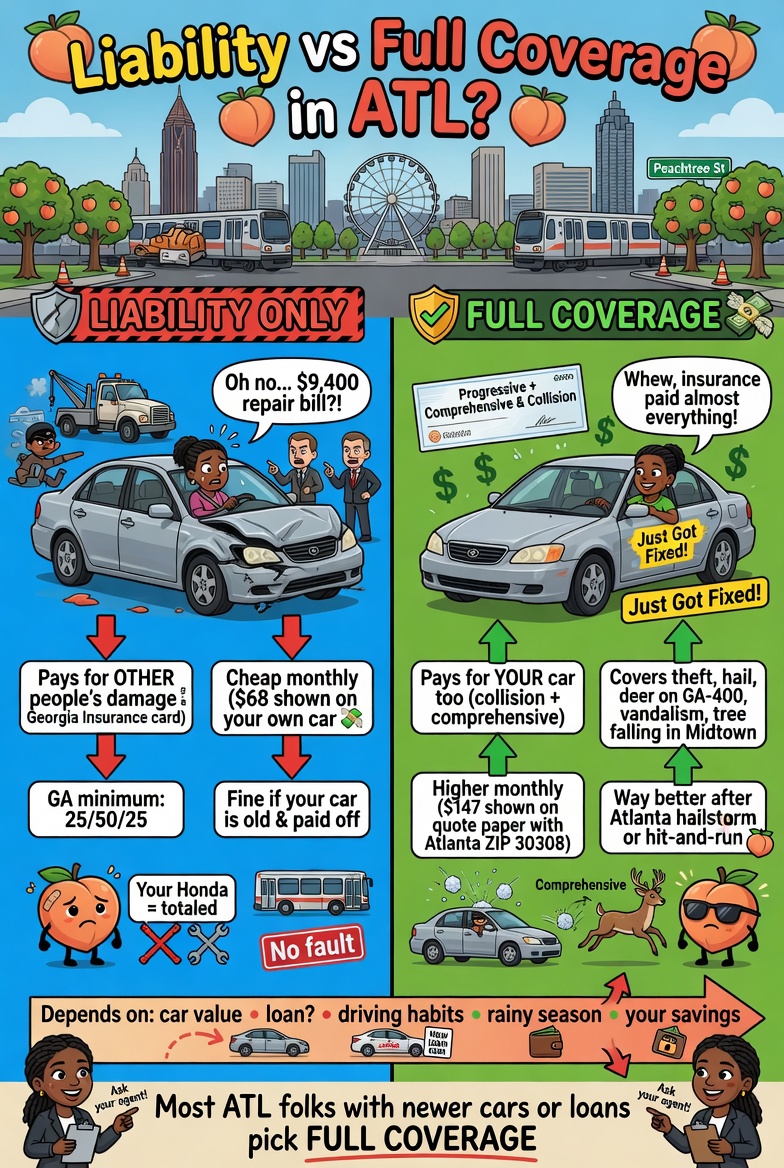

Liability-only covers damage YOU cause to others (their car, their injuries). It does NOT cover your own vehicle in any scenario. Typical Atlanta cost: $700-1,100/year.

Full coverage adds Collision (your car in accidents) + Comprehensive (theft, storm, vandalism). Typical Atlanta cost: $1,800-2,800/year.

The math: if the annual premium difference exceeds about 10% of your car's current value, liability-only might make sense. For most Atlanta drivers with vehicles under 10 years old, full coverage wins.

The non-negotiables: if you have a loan, your lender requires full coverage. If your car is worth $5K+, you almost certainly need it.

What both should include: Uninsured/Underinsured Motorist coverage. Georgia's 12% uninsured rate makes this essential, not optional.

What Liability-Only Actually Covers (And Doesn't)

Georgia's state minimum is 25/50/25 — meaning:

$25,000 bodily injury liability per person

$50,000 bodily injury liability per accident

$25,000 property damage liability

What that means in plain English:

You hit someone and injure them: your liability pays for their medical bills, up to $25K per person / $50K per accident

You damage someone else's property (car, fence, building): your liability pays up to $25K

What liability-only does NOT cover:

Your own vehicle in any accident — even if it's totaled, you pay

Theft of your vehicle

Vandalism

Weather damage (hail, falling trees, flooding)

Hit-and-run where the other driver flees

Animal collisions (deer, etc.)

Glass damage

The Georgia state minimum (25/50/25) is dangerously inadequate. A serious injury accident easily exceeds $100K in medical costs. If you cause an accident with state minimum coverage and the damages exceed $25K, you're personally on the hook for the difference — they can sue your savings, retirement, home equity.

Most Atlanta brokers recommend 100/300/100 minimum (100K per person bodily injury / 300K per accident / 100K property damage). That's about $50-150/year more than state minimum and dramatically reduces exposure.

What Full Coverage Actually Covers

Full coverage = Liability + Collision + Comprehensive. Each part covers a different risk:

Collision coverage pays for damage to your vehicle from:

Accidents you caused

Accidents another driver caused (then your carrier subrogates against theirs)

Single-car accidents (hitting a pothole, sliding off the road, etc.)

Object collisions (telephone pole, parked car, etc.)

Comprehensive coverage pays for damage to your vehicle from:

Theft (Atlanta is top-25 nationally for vehicle theft)

Vandalism and break-ins

Storm damage (hail, falling trees — common in Atlanta)

Flooding

Fire

Glass damage

Animal collisions (hitting a deer)

Riot or civil unrest

Standard deductibles for both: $500 or $1,000 are most common. Higher deductible = lower premium.

Maximum payout: the vehicle's actual cash value (ACV) at the time of loss. So if your $20K car is now worth $14K when totaled, you get $14K (minus deductible), not what you originally paid.

The 5-Question Decision Framework

Five questions to answer in order:

1. Do you have an active auto loan or lease?

Yes: full coverage is required by your lender. Decision made. Skip to coverage-add section below.

No: continue to question 2.

2. What is your vehicle currently worth?

Under $3,000: liability-only often makes sense

$3,000 – $7,000: depends on premium difference and risk tolerance

$7,000+: full coverage almost always wins

3. Could you afford to pay cash to replace the vehicle tomorrow?

Yes, easily: you can self-insure the collision/comprehensive risk

No: you need full coverage to transfer that risk to the carrier

4. How and where do you drive?

Daily Atlanta highway commute (I-285, I-75, I-85, GA-400): high accident exposure → full coverage

Mostly suburban driving, short trips: lower exposure → liability-only more defensible

Vehicle parked outside in Atlanta ZIP with high theft rates: comprehensive especially important

5. What's your annual premium difference between the two?

Calculate: (Full coverage premium − Liability-only premium) ÷ Vehicle value

Result above 15%: liability-only might be worth considering

Result below 10%: full coverage almost certainly wins

In between: judgment call based on the other questions

When Liability-Only Actually Wins

Liability-only is the right answer when all of these apply:

You own the vehicle outright (no loan, no lease)

Vehicle is worth under ~$3,000-5,000 in current market value

You can comfortably replace it from cash savings without disrupting your life

Your premium difference is large relative to vehicle value (typically 15%+)

The vehicle is replaceable (common make/model that you could find again easily)

Real example: a 12-year-old Honda Civic worth $4,000, paid off, owned by someone with $10K+ in savings. Premium difference between liability and full = $900/year. That's 22.5% of the car's value. Doing the math: it would take less than 5 years of premium savings to "pay for" the vehicle. Liability-only wins.

When Full Coverage Is Essential

Full coverage is required (or essentially required) when any of these apply:

You have an auto loan or lease (lender requires it)

Your vehicle is worth $5,000+ with no emergency fund to replace it

You couldn't easily replace the vehicle from cash without major financial disruption

You drive in Atlanta traffic regularly (high accident exposure)

You finance any portion of the vehicle

Your vehicle is less than 7-8 years old

For most working Atlanta professionals with vehicles less than 10 years old, full coverage is the right call. The premium savings of liability-only rarely outweighs the risk of total vehicle loss.

Real Atlanta Math: The Break-Even Calculation

Let me show you the math with a real Atlanta scenario.

Vehicle: 2020 Honda Civic, currently worth $14,000 Liability-only premium: $900/year Full coverage premium: $1,950/year Annual premium difference: $1,050

Question: how long would you have to go without a covered loss for liability-only to "win"?

Years to recoup vehicle value through premium savings: $14,000 ÷ $1,050 = 13.3 years

Translation: you'd need to go 13+ years without a covered loss for liability-only to be the right financial choice on this vehicle.

Probability of a covered loss in 13 years for an Atlanta driver? Very high. Theft, weather damage, accidents — at least one is statistically likely over that timeframe.

This is why full coverage usually wins. The math is rarely close on vehicles worth more than ~$5,000.

Coverages You Should Add Beyond Standard Full Coverage

Whether you pick liability-only or full coverage, these add-ons matter:

Uninsured/Underinsured Motorist (UM/UIM): Critical in Georgia. Roughly 12% of Georgia drivers are uninsured. If they hit you and disappear or have inadequate coverage, your UM/UIM pays your damages. Skipping it is dangerous. Add: $30-100/year.

The full structural explanation of Atlanta's expensive rates is in Why Is Car Insurance So Expensive in Atlanta?.

Higher liability limits: raise from state minimum 25/50/25 to at least 100/300/100. Cost: about $50-150/year. Protects against major lawsuits.

Personal Injury Protection (PIP) or Medical Payments: pays for medical bills for you/passengers regardless of fault. Cost: $25-75/year. Useful if you don't have great health insurance.

Rental reimbursement: pays for a rental car while yours is being repaired after a covered loss. Cost: $25-50/year.

Roadside assistance: towing, jump starts, lockouts. Cost: $10-30/year. Some include flat tire and fuel delivery.

Gap insurance: for financed vehicles where you owe more than the car is worth. Critical for new car loans. Cost: $300-500 (often one-time fee) or $20-40/year through carrier.

OEM parts endorsement: ensures repair shops use original manufacturer parts (not aftermarket). Cost: $30-60/year. Worth it on newer vehicles with body work concerns.

Diminished value coverage: rare in Georgia auto policies, but valuable. Pays the difference between pre-accident value and post-repair value (since accident history reduces resale value).

For the deep-dive on adding $1M-5M umbrella above auto/home liability, see What Is an Umbrella Policy?

Atlanta-Specific Risks That Affect This Decision

Several Atlanta-specific factors push the math toward full coverage:

Traffic density. I-285, I-75, I-85, GA-400 — Atlanta's highway system has some of the highest accident rates in the South. More miles in heavy traffic = higher accident probability.

Uninsured motorist rate. ~12% of Georgia drivers carry no insurance. If they hit you and flee, only your own coverage protects you.

Theft rates. Atlanta consistently ranks top-25 nationally for vehicle theft. Comprehensive coverage specifically addresses this.

Storm exposure. Hail, falling pine trees, flooding — Atlanta storms regularly cause vehicle damage that liability-only doesn't cover.

Repair cost inflation. Atlanta-area auto repair costs have climbed faster than the national average. A "minor" fender bender that would have cost $2,000 five years ago now runs $4,000-6,000.

High-cost ZIP codes. Atlanta proper (30309, 30312, 30318) has both higher accident frequency AND higher repair costs vs suburbs.

Common Mistakes Atlanta Drivers Make

Patterns I see weekly:

Carrying state minimum 25/50/25 liability. Dangerously inadequate. One serious accident exhausts your coverage and exposes your personal assets.

Dropping full coverage on a financed vehicle. Violates your loan terms. Lender can call the loan immediately, force-place expensive insurance, or repossess. Don't do this.

Carrying full coverage on a $2,000 beater. The collision/comprehensive premium can exceed the entire value of the car within 2-3 years.

Skipping uninsured motorist coverage. Georgia's 12% uninsured rate means this is essential, not optional.

Not increasing liability limits as wealth grows. State minimum makes sense at 22 with no assets. At 45 with a house and retirement savings, 100/300/100 minimum (or 250/500/250 with umbrella) is appropriate.

Filing every small claim. A $1,500 claim raises premium $200-300/year for 3-5 years. You collect $1,500 but pay $900-1,500 in premium increases. Not always worth it.

Not reviewing coverage as vehicle ages. A car worth $25K new might be worth $8K after 8 years. Coverage that made sense at $25K may not at $8K.

Auto-renewing without re-shopping. Carrier loyalty rarely pays. Shop every 2 years.

Frequently Asked Questions

Is full coverage required by law in Georgia? No — only liability is required. But your lender, lessor, or finance company will require full coverage if you have a loan.

Can I drop my collision coverage but keep comprehensive? Yes, some carriers allow this — comprehensive without collision (covers theft, storm, glass but not accidents). Useful for vehicles you mostly park and rarely drive.

What if I have a loan and stop paying for full coverage? Your lender will be notified by the carrier. They'll force-place insurance (which is much more expensive and covers only their interest, not yours). Repeated lapses can trigger loan default.

Does my homeowners insurance cover my car? No. Personal property coverage on homeowners excludes vehicles. Auto insurance is the only product that covers vehicles.

How fast can I switch from liability to full coverage? Same-day with most carriers. Coverage takes effect at the time of binding.

Can I have liability-only with one carrier and full coverage with another? You can split policies across carriers, but it's almost always more expensive than bundling both on the same vehicle with one carrier. Not recommended.

Does the make/model of car affect the liability vs full decision? Yes. High-theft models (certain Hyundais, Kias, full-size pickups) have higher comprehensive premiums. Luxury vehicles have higher collision premiums. Match coverage to vehicle.

Do I need full coverage on a project car or rarely-driven vehicle? If you store it indoors and rarely drive it, comprehensive-only might make sense (covers theft and storm while parked). Many carriers offer specialty antique/classic policies for this scenario.

The Bottom Line

For most Atlanta drivers with vehicles less than 10 years old, full coverage wins — the premium difference rarely justifies the risk of total vehicle loss. The exception: older vehicles (10+ years), low cash value (under $5K), no loan, with the financial ability to absorb a total loss.

Regardless of which path you pick, three things matter:

Raise your liability limits to at least 100/300/100 (or higher with an umbrella)

Add Uninsured/Underinsured Motorist coverage — Georgia's 12% uninsured rate makes this essential

Reassess every 2-3 years as your vehicle ages and value drops

If you're not sure which path makes sense for your specific vehicle and situation, book a 15-minute call with me. I'll pull quotes across all major Atlanta auto carriers, run the actual math for your vehicle, and tell you exactly what coverage is appropriate. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out How Much Does Car Insurance Cost in Atlanta in 2026? (the prerequisite cost breakdown), or Atlanta Homeowners Insurance: A 2026 Buyer's Guide (the natural bundle partner). The "Why Is Car Insurance So Expensive" deep-dive publishes Tuesday May 26.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal, tax, or financial advice. Auto insurance premiums, Georgia minimum requirements, carrier coverages, and uninsured motorist rates change.