What Does Medicare Cost in 2026?

Author: Justin Bishop · May 25, 2026 · 10 min read

If you're approaching 65 in Atlanta — or already on Medicare and trying to make sense of your annual costs — you've probably noticed something frustrating: Medicare costs are scattered across four different products with different rules, and nobody hands you a single bill that shows what it all adds up to.

The reality is that Medicare's 2026 total monthly cost ranges from $185/month (lower-income enrollees on Medicare Advantage) to $900+/month (high-earners on Original Medicare + Medigap + Part D + IRMAA surcharges). That's a 5x spread depending on income, plan structure, and which path you take.

This post breaks down every cost component, the IRMAA surcharge that catches high-earning retirees off guard, the new $2,000 Part D out-of-pocket cap that's the biggest Medicare improvement in years, and gives 5 real Atlanta-area cost scenarios so you can see exactly what your situation will look like.

I'm Justin Bishop, an independent broker in Atlanta. I run Medicare cost projections for Georgia retirees weekly. Here's the honest 2026 breakdown.

The 30-Second Version

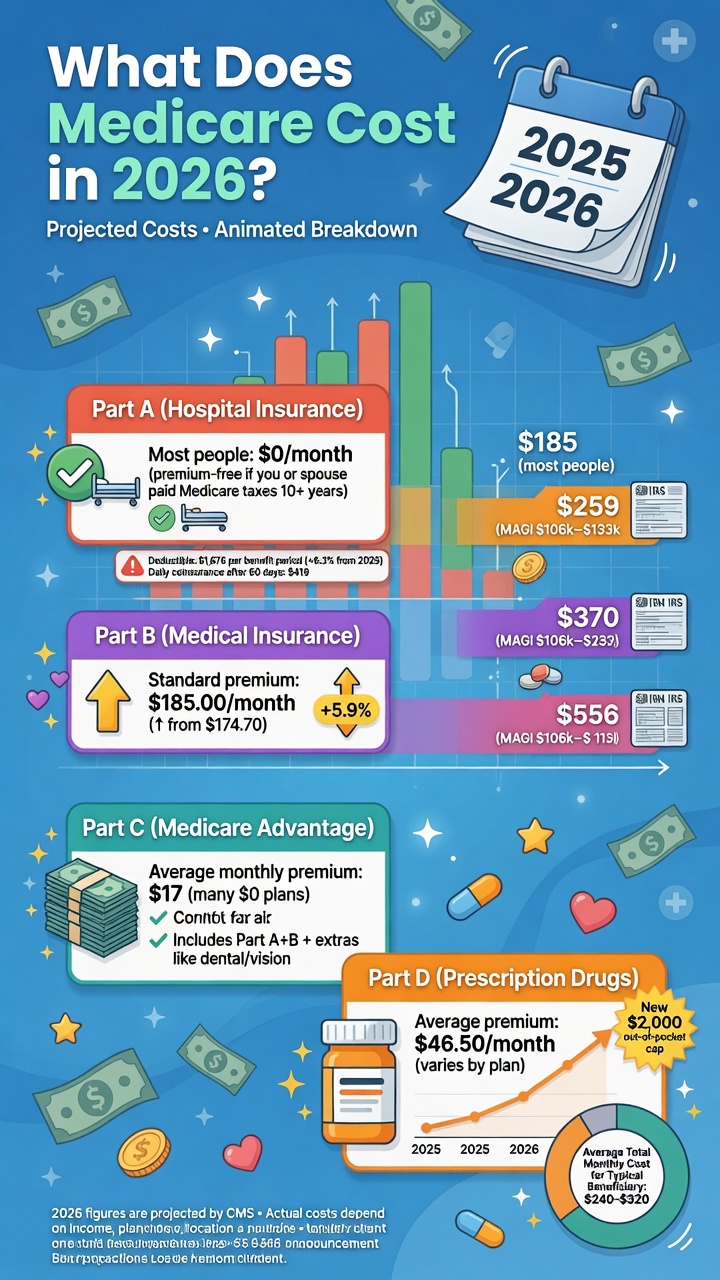

Part A (Hospital): $0/month for most (40+ work quarters). $518/month for those without enough work history.

Part B (Medical): $185/month standard in 2026. Higher for incomes over $109K single / $218K joint (IRMAA — see below).

Part D (Prescription): $46/month average + new $2,000 annual out-of-pocket cap (huge 2026 improvement)

Medigap (Plan G): $150-300/month in Atlanta for age 65 healthy enrollee. Combined with Part B + Part D = $380-500/month all-in.

Medicare Advantage: often $0 premium beyond Part B. Total $185-280/month, but with copays and out-of-pocket exposure up to ~$9,300/year.

Not covered: dental, vision, hearing aids, long-term care, most international travel

The IRMAA surcharge: high earners pay $74-443/month MORE for Part B and Part D. Most don't realize this exists until the first bill.

Real Atlanta total monthly costs (2026): $185 (low-income MA) → $400 (typical middle-income Medigap path) → $939 (high-earner Medigap + IRMAA)

Part A (Hospital Coverage) — Usually Free, But Not Always

Part A covers inpatient hospital stays, skilled nursing facility care, hospice, and some home health care.

2026 Part A premium:

$0/month for anyone with 40+ quarters (10 years) of Medicare-covered work history. This applies to the vast majority of Atlantans approaching 65.

$285/month for those with 30-39 quarters of work history

$518/month for those with fewer than 30 quarters (rare situation, usually applies to immigrants or those with very limited US work history)

2026 Part A deductible (per benefit period):

$1,676 per benefit period for hospital stays. This isn't annual — it resets each new benefit period (60 days without inpatient care)

Days 1-60 of hospital stay: $0 coinsurance after deductible

Days 61-90: $419/day coinsurance

Days 91-150 (lifetime reserve): $838/day coinsurance

Beyond 150 days: you pay 100% (where Medigap or Medicare Advantage caps become critical)

For most Atlanta retirees, Part A premium is $0 — but the $1,676 deductible plus daily coinsurance for longer stays adds up fast. This is where Medigap pays its biggest dividends.

Part B (Medical Coverage) — The $185 Standard Premium

Part B covers doctor visits, outpatient services, durable medical equipment, preventive services, and some home health.

2026 standard Part B premium: $185/month (set by CMS, applies regardless of which state you live in).

2026 Part B deductible: $257/year. After meeting deductible, Medicare pays 80%, you pay 20% — with no annual maximum out-of-pocket on Part B (which is exactly why most Atlanta retirees buy Medigap or Medicare Advantage).

Part B premium is automatically deducted from your Social Security check if you're collecting Social Security. Otherwise you're billed quarterly.

Important: Part B premium goes UP every year. From $174.70 in 2024 → $185 in 2026. Plan for 3-7% annual increases.

The IRMAA Surcharge Most People Don't Know About

This is the cost most Atlanta retirees miss until they get their first Medicare bill. IRMAA stands for Income-Related Monthly Adjustment Amount. If your income exceeds certain thresholds, you pay extra for Part B AND Part D — sometimes a LOT extra.

2026 IRMAA brackets (based on 2024 modified adjusted gross income):

Single up to $109K / Joint up to $218K: standard premiums (no surcharge)

Single $109K-137K / Joint $218K-274K: +$74/month Part B, +$13.70/month Part D

Single $137K-171K / Joint $274K-342K: +$185.40/month Part B, +$35.50/month Part D

Single $171K-205K / Joint $342K-410K: +$296.80/month Part B, +$57.20/month Part D

Single $205K-500K / Joint $410K-750K: +$408.20/month Part B, +$78.90/month Part D

Single $500K+ / Joint $750K+: +$443.40/month Part B, +$85.80/month Part D

Critical points about IRMAA:

Based on 2-year-old income. Your 2026 IRMAA is calculated from your 2024 tax return.

Triggered by one-time income spikes. Sold a business in 2024? Took a big Roth conversion? Received a one-time large bonus? All trigger 2026 IRMAA even if your normal income is much lower.

Appealable. If your income drops due to retirement, divorce, death of spouse, loss of pension, or work stoppage, you can file Form SSA-44 to appeal. This is one of the most underused tools in Medicare cost management.

Cliffs, not phase-ins. Cross a threshold by $1, you pay the full higher amount for the year.

For high-earning Atlanta retirees, IRMAA can add $1,000-6,500 per year to your Medicare costs. Tax planning around the brackets matters enormously.

Part D (Prescription Coverage) — Plus the 2026 Game-Changer

Part D covers prescription drugs. You enroll either as a standalone plan (paired with Original Medicare + Medigap) or built into a Medicare Advantage plan.

2026 Part D average premium: $46/month for stand-alone plans. Atlanta-area plans range $15-90/month depending on formulary coverage.

2026 Part D deductible: $590 maximum allowed by CMS. Many plans have $0 deductible.

THE 2026 GAME-CHANGER: for the first time, Part D includes an annual out-of-pocket maximum of $2,000. Once you hit $2,000 in prescription costs in a year, you pay $0 for additional covered drugs the rest of the year.

This is the biggest Medicare improvement in over a decade. Previously, expensive specialty drugs could cost retirees $5,000-15,000+ per year out-of-pocket. The $2,000 cap eliminates that exposure.

Important Part D nuances:

Each plan has its own formulary (covered drug list). Same drug can cost $5/month on one plan and $200/month on another.

Re-shop your Part D plan EVERY year during AEP (Oct 15-Dec 7). Formularies change.

Late enrollment penalty: 1% of national base premium per month delayed. Permanent.

Medigap (Medicare Supplement) — $150-300/Month in Atlanta

Medigap policies fill the "gaps" in Original Medicare — primarily the 20% Part B coinsurance and the Part A hospital deductible.

2026 Atlanta Medigap pricing (age 65, healthy, female):

Plan G (most popular for new enrollees): $150-280/month

Plan N (lower premium, small copays at point of care): $110-220/month

Plan F (closed to those new to Medicare 2020+): $200-380/month for those eligible

Plan G-HD (high-deductible Plan G): $40-80/month (for healthy enrollees willing to absorb $2,800 annual deductible)

Pricing varies significantly by:

Age (premium increases ~3-5% per year of age in most "attained age" rating states)

Gender (women typically pay slightly more)

Tobacco use

Carrier (rates vary $50-150/month between carriers for IDENTICAL Plan G coverage)

In Georgia, Medigap carriers use medical underwriting outside your initial 6-month Medigap enrollment window — meaning if you try to switch plans after that window, the new carrier can deny you or charge higher rates based on health history. Critical to know: lock in Medigap during your initial Part B enrollment window.

Medicare Advantage (Part C) — Often $0 Additional Premium

Medicare Advantage replaces Original Medicare with a private plan. You still pay Part B premium ($185/month) to the government, but the MA plan often charges $0 additional premium.

2026 Atlanta Medicare Advantage cost structure:

Plan premium: $0-150/month (most $0 premium HMO plans available)

Includes Part D drug coverage (no separate plan needed)

Often includes extras: dental, vision, hearing, gym memberships, OTC allowances

Copays per visit: typically $0-$50 for primary care, $40-$75 for specialists

Hospital copays: typically $300-450/day for first 5-7 days

Maximum out-of-pocket (MOOP): required by Medicare; capped at $9,300 in-network for 2026, $13,950 combined in-and-out-of-network for PPO plans

Real Atlanta MA total monthly cost: typically $185-280/month base (Part B + small MA premium if any). Plus point-of-care copays as you use services. Plus IRMAA if you're a high earner.

For the deep comparison between MA and Medigap, see What's the Difference Between Medicare Advantage and Medigap?.

What Medicare Does NOT Cover (Major Cost Gaps)

This is where most retirees get caught off guard. Original Medicare does NOT cover:

Dental care. Cleanings, fillings, crowns, dentures — all separate. Stand-alone dental plans in Atlanta: $25-80/month.

Vision care. Eye exams, glasses, contacts — separate. Stand-alone vision plans: $10-25/month.

Hearing aids. $1,000-6,000 per pair, not covered. Some Medicare Advantage plans include limited hearing benefits.

Long-term care. Nursing home or in-home care for non-medical needs — completely excluded. Atlanta long-term care costs $80K-150K+/year. This is the biggest financial risk most retirees don't plan for.

Most international travel. Limited coverage abroad. Travel medical insurance recommended.

Cosmetic procedures. Almost never covered.

Routine foot care. Limited coverage; basic podiatry usually not covered.

Acupuncture and most alternative medicine. Limited acceptance.

Personal care services at home (bathing, dressing, meals) — separate.

Many Medicare Advantage plans include dental, vision, and hearing benefits — though these benefits are typically limited (e.g., $1,000-3,000/year dental cap). For comprehensive coverage, separate plans usually still needed.

Real 2026 Atlanta Total Monthly Cost Scenarios

Here's what Medicare actually costs in Atlanta for typical situations:

Scenario 1: Low-income retiree, Medicare Advantage HMO

Part B: $185

MA premium: $0

Includes Part D

Total: $185/month (~$2,220/year base, plus copays as you use it)

Scenario 2: Middle-income retiree (under IRMAA), Medigap Plan G + Part D

Part B: $185

Plan G: $180

Part D: $46

Total: $411/month (~$4,930/year, plus $257 annual Part B deductible = $5,187/year)

Scenario 3: Same as Scenario 2 but Plan N instead of Plan G

Part B: $185

Plan N: $150

Part D: $46

Total: $381/month (~$4,575/year, plus small copays at point of care)

Scenario 4: High earner ($200K joint income), Medigap Plan G + Part D

Part B: $185 + $74 IRMAA = $259

Plan G: $180

Part D: $46 + $13.70 IRMAA = $59.70

Total: $499/month (~$5,985/year)

Scenario 5: Very high earner ($600K joint income), Medigap Plan G + Part D

Part B: $185 + $408.20 IRMAA = $593.20

Plan G: $180

Part D: $46 + $78.90 IRMAA = $124.90

Total: $898/month (~$10,775/year — almost 5x the basic MA scenario)

For most middle-income Atlanta retirees, $380-500/month is the realistic total cost when factoring in Medigap and Part D. For Medicare Advantage routes, expect $185-280/month base plus variable point-of-care costs.

What's "Free" with Medicare in 2026

Original Medicare covers certain preventive services at $0 cost-share to you:

Annual wellness visit

Cardiovascular disease screenings

Cancer screenings (mammograms, colonoscopies, prostate exams)

Diabetes screenings

Vaccinations (flu, COVID, pneumonia, shingles, Tdap)

Bone mass measurements

Smoking cessation counseling

Depression screening

Obesity counseling

Use these aggressively — they're a real benefit that costs you nothing and catches problems early when they're cheaper to treat.

How to Lower Your Medicare Costs in Atlanta

Real moves that work:

Time your Part B enrollment perfectly. Late enrollment penalty is 10% per year delayed — permanent.

Lock in Medigap during your initial 6-month window. Georgia uses medical underwriting outside that window.

Re-shop your Part D plan every year during AEP. Drug formularies change; the cheapest plan rotates.

Re-shop Medicare Advantage every year during AEP if you're on MA. Plan benefits change annually.

File SSA-44 to appeal IRMAA after retirement. One of the most underused tools in Medicare cost management.

Plan tax events around IRMAA brackets. A large Roth conversion or business sale can spike your IRMAA for 1-2 years if not planned.

Consider Plan N vs Plan G if you don't visit doctors often. Save $30-60/month for small copays at point of care.

Use Medicare's free preventive services. Aggressive use of $0 screenings catches problems early.

Check for Medicare Savings Programs if income is limited. Georgia has programs that help pay Part B premium for those who qualify.

Bundle dental/vision through Medicare Advantage if those benefits matter and you don't need broad provider choice.

Common Medicare Cost Mistakes Atlantans Make

Patterns I see weekly:

Not knowing about IRMAA until the first bill. Most retirees are stunned when they see Part B premium $400-600/month instead of $185.

Picking Part D based on premium alone. A $25/month plan that doesn't cover your specific medications costs you thousands more than a $50/month plan that does.

Letting Medicare Advantage auto-renew. Plans change every year. The 2025 best plan rarely stays the 2026 best.

Defaulting to Original Medicare without Medigap. Without Medigap, you face uncapped 20% Part B coinsurance forever.

Skipping the SSA-44 IRMAA appeal after retirement. Free money left on the table.

Buying separate dental/vision when MA bundled benefits would have worked. Or vice versa.

Not factoring long-term care into Medicare planning. Medicare doesn't cover it. LTC costs are the biggest financial risk most retirees face.

Choosing plans on premium alone without checking out-of-pocket exposure. A $0 premium MA plan with a $9,300 MOOP can cost more than a $200/month Medigap plan with $0 out-of-pocket after Part B deductible.

Frequently Asked Questions

Why does Part B keep going up every year? Medicare costs grow faster than inflation due to medical inflation and the aging population. Expect 3-7% annual Part B increases through 2028+.

Can I lower my Part B premium? Only by appealing IRMAA if your income dropped due to a qualifying life event (retirement, divorce, etc.). Standard Part B premium is set by CMS.

Does the $2,000 Part D out-of-pocket cap apply to Medicare Advantage too? Yes — Medicare Advantage plans that include Part D coverage are also subject to the $2,000 annual prescription drug out-of-pocket cap in 2026. Huge improvement for MA enrollees on expensive medications.

What if I can't afford my Medicare premiums? Look into Medicare Savings Programs (MSPs) through Georgia DCH. There are 4 programs that help with Part B premium, Part A premium, and cost-sharing for those with limited income/assets.

Does my Part B premium count toward income taxes? Yes, Medicare premiums (including IRMAA surcharges) are tax-deductible as medical expenses to the extent they exceed 7.5% of AGI. Worth tracking if you itemize.

How much should I budget for total annual Medicare costs? Middle-income retiree: $5,000-6,500/year for Original Medicare + Medigap + Part D. High earners with IRMAA: $7,000-12,000/year. Medicare Advantage route: $2,500-4,500/year base plus variable point-of-care.

Will Medicare costs go down ever? Highly unlikely in absolute terms. The 2026 Part D $2,000 cap reduces extreme drug costs for some, but base premiums continue rising. Plan for steady increases.

Should I delay Medicare to save on premiums? Almost never. Late enrollment penalties last for life and exceed any short-term savings.

The Bottom Line

Medicare in 2026 costs Atlanta retirees somewhere between $185/month (lower-income Medicare Advantage) and $900+/month (high-earner Original Medicare + Medigap + IRMAA). The 5x spread depends primarily on income (IRMAA), plan structure (Medigap vs MA), and which add-ons you need (dental, vision, LTC).

The 2026 game-changer is the new $2,000 Part D out-of-pocket cap — the biggest Medicare improvement in over a decade. If you take expensive specialty medications, this single change could save you thousands per year compared to pre-2026 rules.

For most middle-income Atlanta retirees, plan for $400-500/month all-in for Original Medicare + Medigap Plan G + Part D. Medicare Advantage routes run $185-280/month base but with variable point-of-care costs.

If you're approaching 65 and want a personalized cost projection for your specific situation — including any IRMAA exposure and Medigap shopping across multiple Atlanta carriers — book a 15-minute call with me. I'll run the actual numbers for your income level, health profile, and prescriptions. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out What's the Difference Between Medicare Advantage and Medigap?, When Should I Sign Up for Medicare? The 6 Windows Explained, or Final Expense Insurance: The Policy Most Atlantans Overlook (Medicare-adjacent end-of-life planning).

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not medical, tax, or financial advice. Medicare premiums, IRMAA brackets, Part D rules, and CMS guidance change.