What's the Difference Between Medicare Advantage and Medigap?

Author: Justin Bishop · May 13, 2026 · 9 min read

If you're approaching 65 in Georgia — or already on Medicare and rethinking your plan choice — you've hit the single biggest decision in Medicare: Medicare Advantage (Part C) or a Medigap (Medicare Supplement) plan paired with Original Medicare?

You've probably seen the TV commercials for $0 premium Medicare Advantage plans. You've probably also heard horror stories from neighbors about prior authorizations, network surprises, and out-of-pocket bills. Both are real. The truth is that the right answer depends on your specific health, budget, doctor relationships, and tolerance for risk — not on whichever option happens to be advertised most loudly.

This post breaks down what each path actually is, what each one really costs, where each one wins, and the specific Georgia-market considerations that should shape your choice in 2026.

I'm Justin Bishop, an independent broker in Atlanta. I help Georgians choose between Medicare Advantage and Medigap every week. Here's the honest comparison.

The 30-Second Version

Medicare Advantage (Part C): private alternative to Original Medicare. Often $0 monthly premium, includes Part D drug coverage, often includes dental/vision/hearing. But: HMO/PPO networks, prior authorizations required, copays/coinsurance per visit, max out-of-pocket up to ~$9,300/year in-network for 2026.

Medigap (Medicare Supplement) + Original Medicare + Part D: higher monthly premium ($150-300/month in Georgia for Plan G). But: no networks (any doctor that accepts Medicare), minimal out-of-pocket once premium is paid, no prior authorizations.

The trade-off most retirees miss: Medicare Advantage trades monthly premium savings for variable, harder-to-predict out-of-pocket costs. Medigap trades higher monthly premium for predictable, capped out-of-pocket costs.

The right answer in Georgia: depends on your specific situation. There's no universally "best" choice — but there's a best choice for you.

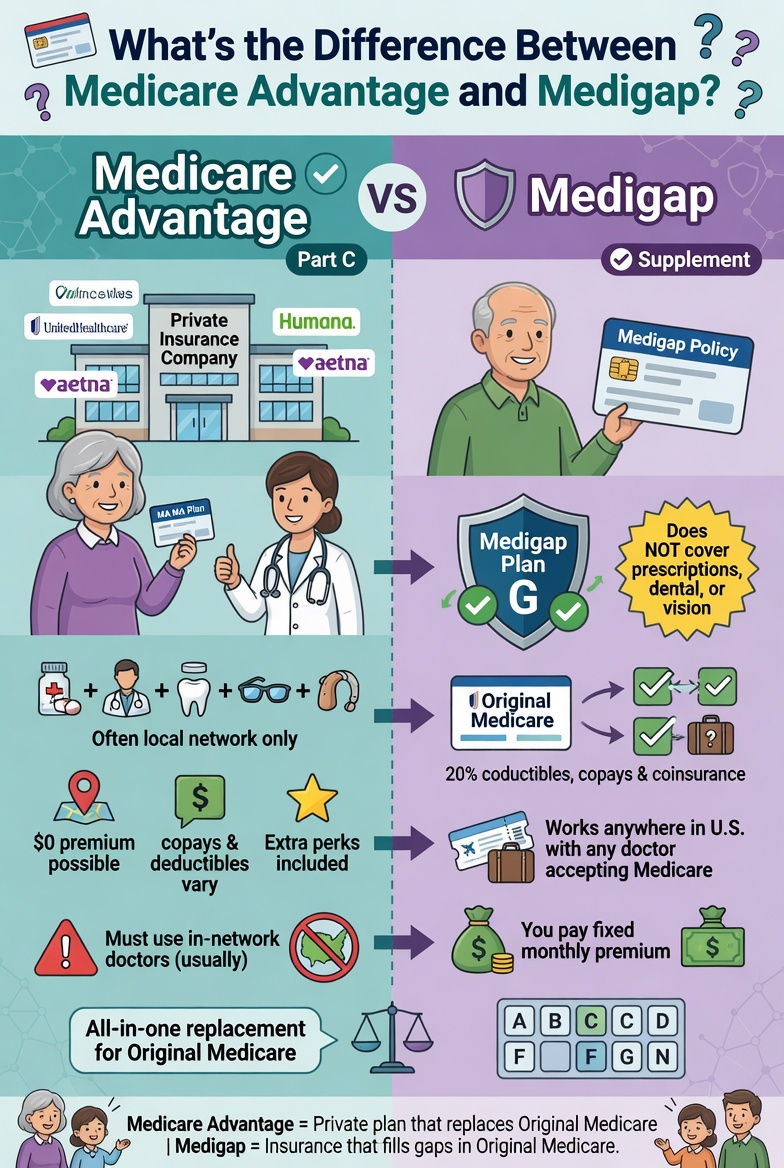

What Medicare Advantage Actually Is

Medicare Advantage (also called "Part C" or "MA plans") is a private health insurance alternative to Original Medicare. When you enroll in a Medicare Advantage plan:

The private carrier replaces Original Medicare as your primary insurance

You still pay your Part B premium to the government ($185/month in 2026 standard)

You usually pay a low additional premium to the MA carrier (often $0)

The MA plan provides all your Part A and Part B benefits, plus typically Part D drug coverage

You get extra benefits not in Original Medicare: dental, vision, hearing, fitness memberships, sometimes over-the-counter allowances or transportation

You're locked into the plan's network (HMO) or pay much more out-of-network (PPO)

What the TV commercials don't always emphasize:

Prior authorizations required for many tests, procedures, specialist referrals, and post-acute care (skilled nursing, home health, physical therapy)

Network restrictions vary by plan — some Atlanta MA plans don't include Emory or Northside; verify your specific doctors and hospitals

Copays and coinsurance apply to most services. A hospital stay might cost $250-450/day for the first 5-7 days

Annual maximum out-of-pocket (MOOP) is required by Medicare rules — typically $4,000-9,300 in-network in 2026

You can switch back to Original Medicare but Medigap underwriting may apply (and you can be denied or charged higher rates based on health)

What Medigap (Medicare Supplement) Actually Is

Medigap is private insurance that pays the "gaps" in Original Medicare — specifically the 20% coinsurance you'd otherwise owe on Part B services, plus the Part A hospital deductible and other cost-sharing.

Medigap plans are sold by letter: Plan A, B, C, D, F, G, K, L, M, N. Plan G is the most popular plan for people new to Medicare because it covers nearly everything except the small annual Part B deductible ($257 in 2026).

When you enroll in Medigap:

You keep Original Medicare as your primary insurance

You pay the Medigap carrier a monthly premium (typically $150-300/month in Georgia for Plan G, age 65)

You also enroll in a Part D drug plan separately (typically $20-80/month)

Any doctor or hospital that accepts Medicare accepts your Medigap — no network

No prior authorizations for Medicare-covered services

Predictable out-of-pocket costs — once you've paid your premiums, most services have zero or minimal additional cost

What's the catch:

Monthly premium is higher than Medicare Advantage

No extras like dental, vision, hearing (you can buy separate dental/vision plans)

You need to enroll in Part D separately

You can switch Medigap plans later, but Georgia uses medical underwriting outside of your initial enrollment period — meaning health questions affect your ability to switch

The Real Side-by-Side Comparison

Here's where the rubber meets the road on monthly cost vs total cost:

Monthly cost (typical Atlanta 65-year-old, healthy, 2026):

Medicare Advantage (HMO, $0 premium): $185 (Part B premium) = $185/month total

Medicare Advantage (PPO, $30 premium): $185 (Part B) + $30 (MA premium) = $215/month total

Original Medicare + Plan G Medigap + Part D: $185 (Part B) + $180 (Plan G in Atlanta) + $40 (Part D) = $405/month total

At first glance, Medicare Advantage is $200+/month cheaper. That's the headline you see.

Total annual out-of-pocket if you stay healthy (no medical events):

MA $0 premium HMO: $185 × 12 = $2,220 in premiums + maybe $0-200 in copays for routine care = ~$2,400/year

Medigap Plan G: $405 × 12 = $4,860 in premiums + $257 Part B deductible = ~$5,100/year

If nothing happens, Medicare Advantage saves you roughly $2,700/year.

Total annual out-of-pocket if you have a major medical event (cancer diagnosis, hip replacement, heart procedure, hospitalization):

MA HMO ($9,300 max out-of-pocket): $2,220 premiums + $9,300 MOOP = ~$11,500/year

Medigap Plan G: $4,860 premiums + $257 Part B deductible = ~$5,100/year

If something significant happens, Medigap saves you roughly $6,400/year.

This is the real trade-off most retirees don't have explained clearly. Medicare Advantage is cheaper if you stay healthy; Medigap is dramatically cheaper if you don't.

When Medicare Advantage Wins

Medicare Advantage is typically the right choice when:

You're generally healthy with limited medical needs and want lower monthly costs

You have predictable healthcare patterns — annual physical, occasional sick visits, established prescriptions

You like the bundled extras — dental, vision, hearing, gym memberships matter to you

You don't travel out of Georgia often — most MA plans only cover non-emergency care in their network area

You have limited monthly budget flexibility — saving $200+/month on premium frees up cash flow

Your doctors are all in the MA plan's network — confirm before enrolling

You qualify for a "dual eligible" plan (Medicaid + Medicare) — these often have zero cost-sharing on top of $0 premium

About 40-50% of Atlanta clients I work with end up choosing Medicare Advantage. It's a legitimate choice — just not for everyone.

When Medigap Wins

Medigap (typically Plan G or Plan N) is typically the right choice when:

You have chronic conditions or expect significant medical use

You value predictable monthly costs over premium savings

You travel out of Georgia for vacations or to visit family — Medigap covers you anywhere in the US that accepts Medicare

You have specific doctors or specialists you want to keep without worrying about network changes

You don't want prior authorizations standing between you and care

You can afford the higher monthly premium to lock in low out-of-pocket exposure

You're at higher risk for major medical events (family history, current health issues)

The other 50-60% of Atlanta clients land on Medigap. Atlanta retirees with established doctor relationships at Emory or Piedmont especially benefit from Medigap's network freedom.

The "Hidden Costs" of Medicare Advantage Most TV Ads Don't Mention

Specific MA cost realities I see weekly with Atlanta clients:

Hospital stay copays. A typical Atlanta MA HMO plan charges $250-400/day for the first 5-7 days of a hospital admission. A week-long stay = $1,750-2,800 out of pocket just for the hospital portion.

Skilled nursing facility (SNF) costs. Original Medicare covers 100% of approved SNF days 1-20. Most MA plans charge $0-50/day for days 1-20 BUT then $150-200/day for days 21-100. A 60-day SNF stay can cost $6,000-12,000 on MA but $0 on Medigap Plan G.

Specialist copays. $40-65 per specialist visit. If you see specialists regularly, this adds up.

Prior authorization delays. Treatment delayed by 3-7 days waiting for prior auth approval is routine. Some treatments get denied entirely.

Out-of-network surprises. PPO plans cover out-of-network at much lower rates. An out-of-network ER visit on travel can cost thousands.

For the full breakdown of every Medicare cost component (including IRMAA and the new $2K Part D cap), see What Does Medicare Cost in 2026?

Network changes mid-year. Carriers can drop providers from their network during the year. Your specialist could be out-of-network by July.

Annual plan changes. MA plans change every January — premium, copays, formulary, network. The plan you picked this year may be worse next year.

These aren't reasons to avoid Medicare Advantage. They're reasons to understand exactly what you're buying before deciding.

Georgia-Specific Considerations

A few things that matter specifically for Georgians:

Major Atlanta hospital networks: Emory, Piedmont, Wellstar, Northside, and Children's Healthcare all accept Original Medicare (which means Medigap works everywhere). Specific MA plans may or may not include each system — verify before enrolling.

Medigap underwriting in Georgia: Georgia is a medical-underwriting state for Medigap outside your initial enrollment period. Translation — if you start on Medicare Advantage and try to switch to Medigap later, the carrier can deny you or charge higher rates based on health history. This is a major reason to think carefully before defaulting to Medicare Advantage.

The "Birthday Rule" does not apply in Georgia. Some states (California, Oregon, Illinois) let Medigap members switch plans around their birthday without underwriting. Georgia is not one of them.

Atlanta-area MA plan options: Humana, UnitedHealthcare (AARP), Aetna, Kaiser Permanente, WellCare, Blue Cross Blue Shield of Georgia, and Cigna all offer MA plans in the Atlanta metro for 2026.

Atlanta-area Medigap carriers: Mutual of Omaha, Cigna, Aetna, UnitedHealthcare (AARP), Blue Cross Blue Shield of Georgia, Anthem, Humana, and others write Plan G in Atlanta. Pricing varies significantly across carriers for the exact same Plan G coverage — same benefits, different premiums.

How to Actually Pick

A simple decision framework I use with Atlanta clients:

Step 1: Make a list of all your current doctors, hospitals, and specialists. Are they all in-network on the MA plans you're considering? If even one critical doctor is out-of-network, Medicare Advantage may be the wrong fit.

Step 2: Make a list of your prescriptions. Are they all on the formulary at reasonable tiers on the MA plan you're considering? Or on the Part D plan you'd pair with Medigap?

Step 3: Run the worst-case-cost math. What would a hospitalization, cancer diagnosis, or major surgery cost you on each option? Can you absorb the worst-case under each?

Step 4: Consider your travel and family situation. Do you go to South Florida for the winter? Visit grandkids in California? Travel internationally? MA networks usually don't follow you.

Step 5: Think about future you. You'll likely live another 15-25 years on Medicare. Health changes over time. Medigap's predictability gets more valuable as you age.

For most healthy Atlanta retirees with limited specific medical needs and budget pressure, Medicare Advantage is a reasonable starting point.

For retirees with chronic conditions, established doctor relationships, travel plans, or who value predictability over premium savings, Medigap Plan G is usually the answer.

For those who can afford it and want maximum protection, Plan G + a separate dental/vision policy is often the gold standard for Atlanta retirees.

Common Medicare Decision Mistakes

Patterns I see weekly:

Picking based on TV commercials alone. The "$0 premium" headline doesn't show the prior authorizations, network restrictions, or potential 5-figure out-of-pocket exposure.

Not verifying network before enrolling. A doctor or hospital you assumed was covered may be out-of-network on the specific MA plan you picked.

Defaulting to Medicare Advantage because it's "free." Free monthly premium is not the same as free care.

Switching from Medigap to MA without understanding the path back. Once you leave Medigap, Georgia underwriting can make it expensive (or impossible) to come back.

Picking a Medigap carrier on brand alone. All Plan G policies cover the same benefits — but premium pricing varies $50-150/month across carriers for identical coverage. Always compare.

Not enrolling in Part D when you choose Medigap. Medigap doesn't include drug coverage. Forgetting to enroll triggers a late-enrollment penalty for life.

Waiting too long to enroll. Missing your Initial Enrollment Period (around your 65th birthday) triggers permanent Part B and Part D penalties.

Not reviewing your plan annually. MA plans change every year. The plan that fit you in 2024 may not fit in 2026.

Before you Decide

Before you pick between Medicare Advantage and Medigap, make sure you know when to enroll: When Should I Sign Up for Medicare? The 6 Windows Explained.

Frequently Asked Questions

Can I switch from Medicare Advantage to Medigap later? Yes, but in Georgia, the Medigap carrier can use medical underwriting to deny you or charge higher rates outside your initial 6-month Medigap enrollment window. Switching back is harder than you'd think.

Is Medicare Advantage really free? No. The $0 premium MA plans still require you to pay Part B ($185/month in 2026) to the government. They have copays, coinsurance, and significant max-out-of-pocket exposure.

What's the difference between Medigap Plan G and Plan N? Plan G covers everything except the small annual Part B deductible. Plan N has slightly lower premiums but includes small copays ($20 doctor visits, $50 ER) and may not cover excess charges (rare). For most Atlantans, Plan G is the simpler choice.

Do I need both Original Medicare AND Medigap AND Part D? Yes. Medigap and Part D are separate from Original Medicare and from each other. You enroll in all three to get the Medigap pathway.

What if I'm under 65 on Medicare (disability)? Medicare Advantage is available. Medigap is harder — Georgia doesn't guarantee Medigap eligibility for under-65 Medicare beneficiaries, though some carriers offer it at higher premiums.

Can I keep my employer health insurance and Medicare? Sometimes — if you're still working and the employer has 20+ employees, you can delay Part B without penalty. Talk to a broker before assuming.

Does Medicare cover long-term care? No — neither Original Medicare, Medicare Advantage, nor Medigap covers extended long-term care or nursing home stays. Long-term care insurance is a separate product.

The Bottom Line

The Medicare Advantage vs Medigap decision is genuinely consequential — and it's the one decision most retirees don't get explained clearly. The right answer for you depends on your health, doctors, travel, budget, and tolerance for variable costs.

For most healthy Atlanta retirees on a tight budget without specific medical needs, Medicare Advantage is a reasonable choice.

For retirees with chronic conditions, established specialist relationships, frequent travel, or higher risk of significant medical events, Medigap Plan G is almost always the better long-term decision.

If you're approaching 65, recently turned 65, or rethinking your current Medicare plan, book a 15-minute call with me. I'll walk through your specific situation — your doctors, your prescriptions, your travel patterns, your health profile — and run the math on both paths so you can make an informed choice. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out When Should I Sign Up for Medicare? The 6 Enrollment Windows Explained (publishing May 18), What Does Medicare Actually Cost in 2026? (publishing May 22), or Atlanta Homeowners Insurance: A 2026 Buyer's Guide (same retiree audience, different coverage).

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not medical, tax, or legal advice. Medicare rules, premium amounts, plan availability, formulary coverage, and Georgia Medigap rules change