When Should I Sign Up for Medicare? The 6 Windows Explained

Author: Justin Bishop · May 19, 2026 · 9 min read

If you're approaching 65 in Atlanta — or already on Medicare and trying to make changes — timing is the single most consequential Medicare decision. Miss the right window and you face penalties that last the rest of your life. Get the timing right and you avoid a lifetime of overpayment.

Medicare has six different enrollment windows, each with different rules, different triggers, and different consequences. Most retirees only learn about the windows when they accidentally miss one — at which point it's usually too late to fix it.

This post walks through all 6 Medicare enrollment windows, when each one opens, who they apply to, what the penalties are for missing them, and the specific timing decisions Atlanta retirees should be thinking about right now.

I'm Justin Bishop, an independent broker in Atlanta. I help Georgians navigate Medicare enrollment every week. Here's the practical timing breakdown.

The 30-Second Version

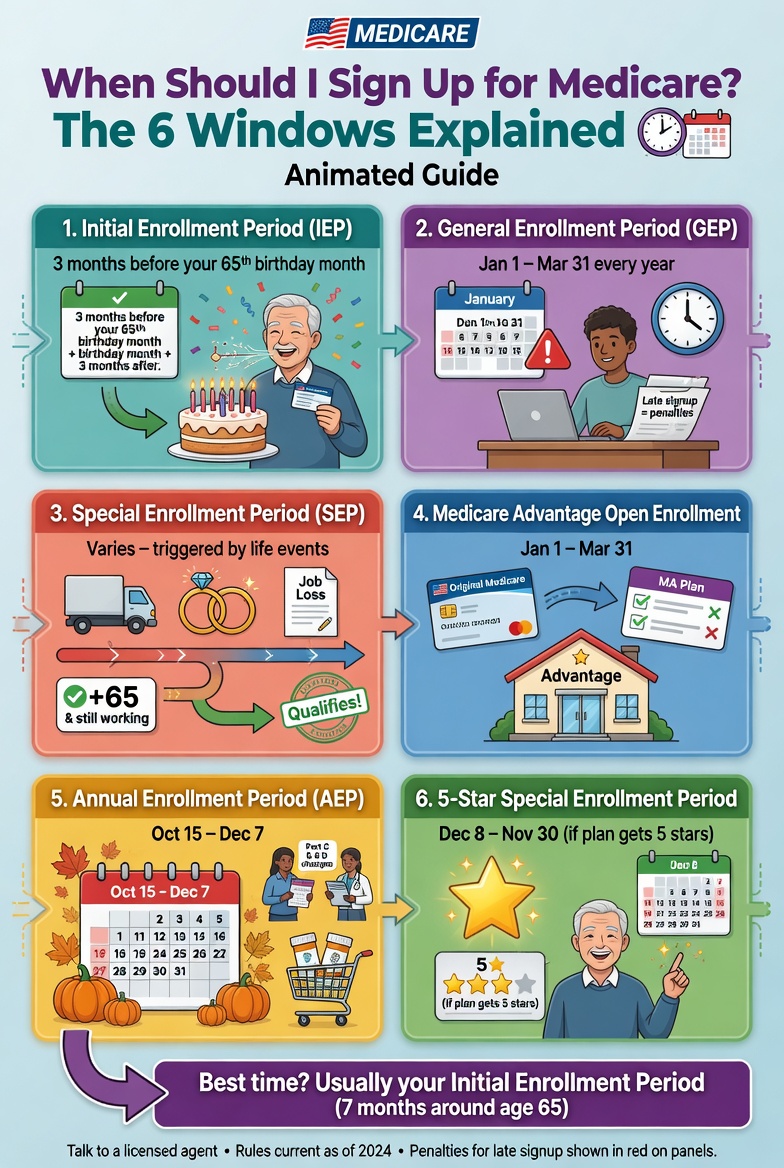

The 6 Medicare enrollment windows:

1. Initial Enrollment Period (IEP): 7 months around your 65th birthday. Your first and most important enrollment window.

2. Special Enrollment Period (SEP): Triggered by life events (losing employer coverage, moving, etc.). 8 months from the trigger event in most cases.

3. General Enrollment Period (GEP): January 1 – March 31 annually. For people who missed IEP and don't qualify for SEP. Penalties apply.

4. Annual Enrollment Period (AEP): October 15 – December 7 annually. Switch Medicare Advantage, Part D, or Medigap plans. This is the biggest annual decision window.

5. Medicare Advantage Open Enrollment Period (MA-OEP): January 1 – March 31 annually. Already on MA? Switch to a different MA plan or back to Original Medicare.

6. 5-Star Special Enrollment Period: December 8 – November 30 annually. Switch to a 5-star rated Medicare Advantage plan once during the year.

Key warning: Part B late enrollment penalty is 10% per year delayed, added to your monthly premium for the rest of your life. Miss your IEP by 3 years and you pay 30% more for Part B forever. This is the most common (and most expensive) Medicare mistake.

Window 1: Initial Enrollment Period (IEP) — Your First and Most Important Window

When it happens: 7 months centered on your 65th birthday. Starts 3 months before the month you turn 65, includes your birth month, and ends 3 months after.

Example: If you turn 65 in October, your IEP runs July 1 through January 31.

What you can enroll in during IEP:

Medicare Part A (hospital coverage — usually free if you have 40+ quarters of work history)

Medicare Part B (medical coverage — $185/month standard premium in 2026)

Medicare Part D (prescription drug coverage)

Medicare Advantage Part C (instead of Original Medicare)

Medigap (Medicare Supplement) — note the special 6-month Medigap window below

When coverage starts:

If you enroll BEFORE your birth month: coverage starts the first of your birth month

If you enroll DURING your birth month: coverage starts the first of the next month

If you enroll AFTER your birth month: coverage delayed 1-3 months

Critical: for most Atlanta retirees not on employer coverage, this is the only window without penalties. Miss it and you'll likely face Part B and Part D late enrollment penalties for life.

The Medigap-specific sub-window: when you first sign up for Part B, you get a 6-month Medigap Open Enrollment Period where carriers cannot deny you coverage or charge higher rates based on health history. In Georgia, this is critical — outside this 6-month window, Medigap carriers can use medical underwriting and deny you. Read more in What's the Difference Between Medicare Advantage and Medigap?.

Window 2: Special Enrollment Period (SEP) — Triggered by Life Events

When it happens: When you experience a qualifying life event that affects your Medicare eligibility or current coverage.

Common SEP triggers:

Losing employer health coverage — 8-month SEP starts the month after employment OR coverage ends (whichever is later). This is the most common SEP.

Spouse losing employer coverage that covered you — same 8-month window

Moving outside your Medicare Advantage or Part D plan's service area — 2-month SEP from the month after you notify your plan

Returning to the US after living abroad — 2-month SEP

Being released from incarceration — 2-month SEP

Losing Medicaid eligibility — 3-month SEP

Plan termination or significant change — typically 2-month SEP from notification

Your Medicare Advantage plan loses its contract with Medicare — varies by situation

Your circumstances change in a way that makes a 5-star plan available — see Window 6

What you can enroll in during SEP:

Depends on the trigger. Most triggers allow enrollment in Medicare Parts A, B, C, and D. Some are more limited.

Critical for working Atlantans 65+: if you stay on employer coverage past 65 (and your employer has 20+ employees), you can delay Part B without penalty. But you must enroll in Part B within 8 months of losing that employer coverage or you'll trigger the lifetime Part B penalty. This is the most common mistake working seniors make.

COBRA does NOT count. If you continue employer coverage via COBRA after leaving a job, that does NOT extend your SEP. The SEP clock starts when employment ends, not when COBRA ends. This trips up almost everyone.

Retiree coverage does NOT count. Retiree-provided health coverage is not considered creditable for delaying Part B without penalty.

Window 3: General Enrollment Period (GEP) — The Penalty Window

When it happens: January 1 – March 31 every year.

Who it's for: People who missed their IEP and don't qualify for any SEP. This is the "catch-all" window for late enrollees.

When coverage starts: The first day of the month after you enroll.

The catch: late enrollment penalties almost always apply:

Part B penalty: 10% added to your monthly premium for every 12 months you delayed enrolling. Permanent — lasts the rest of your life. Example: missed Part B for 3 full years = 30% premium increase forever.

Part D penalty: 1% of the national base premium ($36.78 in 2026) for every month you delayed having creditable drug coverage. Permanent.

GEP is a backstop, not a goal. Avoid it by enrolling correctly during IEP or qualifying SEP.

Window 4: Annual Enrollment Period (AEP) — The Biggest Annual Decision Window

When it happens: October 15 – December 7 every year. Coverage changes take effect January 1 of the following year.

Who it's for: Anyone already on Medicare who wants to change plans.

What you can do during AEP:

Switch from Original Medicare to Medicare Advantage (or vice versa)

Switch from one Medicare Advantage plan to another

Switch from one Part D plan to another

Drop your Medicare Advantage plan and return to Original Medicare

Add or drop a Part D plan

What you can NOT do during AEP:

Switch Medigap plans without underwriting (Medigap has its own enrollment rules)

Enroll for the first time if you weren't already eligible

Why AEP matters every year:

Medicare Advantage plans change every January 1 — different premium, copays, formulary, network

Part D plans change every year — drug coverage, tier pricing, pharmacy network

The plan that worked for you in 2025 may not be the best in 2026

Most retirees never re-shop and overpay year after year

For Atlanta retirees: this is the year-over-year cost optimization window. A 30-minute review with an independent broker during AEP often saves $500-1,500/year compared to letting your current plan auto-renew.

Window 5: Medicare Advantage Open Enrollment Period (MA-OEP)

When it happens: January 1 – March 31 every year.

Who it's for: People already enrolled in a Medicare Advantage plan as of January 1.

What you can do:

Switch to a different Medicare Advantage plan

Drop your MA plan and return to Original Medicare + Part D

Add a Part D plan if returning to Original Medicare

What you can NOT do:

Switch FROM Original Medicare TO Medicare Advantage (MA-OEP is for current MA enrollees only)

Change Medigap plans (Medigap has its own rules)

Important limit: you only get one plan change during MA-OEP. Pick carefully.

This window is a safety net — if you enrolled in an MA plan during AEP and discovered it doesn't fit (network issues, prior auth problems, drug coverage gaps), MA-OEP gives you a 3-month do-over.

Window 6: 5-Star Special Enrollment Period

When it happens: December 8 – November 30 every year (essentially all year except the AEP-to-January window).

Who it's for: Anyone wanting to switch to a Medicare Advantage plan that has earned a 5-star quality rating from Medicare.

What you can do:

Switch to a 5-star Medicare Advantage plan in your area (if one exists)

Switch to a 5-star Part D plan in your area

Use this SEP once per year

Why it exists: Medicare rewards high-quality plans by letting beneficiaries switch into them outside the standard windows.

Reality check: 5-star MA plans are rare. In the Atlanta metro for 2026, only a handful of plans earn 5-star ratings — if any. The window exists, but the available plans are limited. Worth checking annually.

The Late Enrollment Penalties (Why Timing Matters)

This is the part that costs Atlanta retirees the most money over a lifetime:

Part B Late Enrollment Penalty:

10% added to your monthly premium for every full 12 months you delayed enrolling

Permanent — lasts as long as you have Medicare

Calculated against the standard premium ($185 in 2026, increases over time)

Example: 3-year delay = 30% penalty = $55.50 added to monthly premium forever = $666+/year for life

Part D Late Enrollment Penalty:

1% of national base premium ($36.78 in 2026) per month you went without creditable drug coverage

Permanent — lasts as long as you have Part D

Example: 24-month delay = 24% × $36.78 = $8.83 added to monthly Part D premium forever

Part A Late Enrollment Penalty (rare):

Applies only to people who don't qualify for free Part A (didn't have 40 work quarters)

10% added to premium for twice the years delayed

The math compounds over a 20-year Medicare lifespan. A 30% Part B penalty over 20 years = $13,000+ in lifetime overpayment. Compared to enrolling on time? Free

The "Still Working at 65" Question (Most Confusing Scenario)

The biggest source of Medicare timing confusion: what if you're still working at 65 with employer health insurance?

Rule of thumb: if your employer has 20+ full-time employees, your employer plan is "primary" and Medicare is "secondary." You can delay Part B without penalty as long as you keep that employer coverage.

Specific rules:

Employer with 20+ employees: delay Part B without penalty. Enroll in Part B within 8 months of losing employer coverage to avoid Part B penalty.

Employer with fewer than 20 employees: Medicare becomes primary at 65. You should enroll in Part A and B at 65 — your employer plan becomes secondary and may not pay for things Medicare would have covered.

Spouse's employer coverage: counts as creditable if the spouse's employer has 20+ employees AND you're covered as a spouse.

COBRA: does NOT count as creditable. The Part B SEP clock starts when employment ends, not when COBRA ends.

Retiree health insurance: does NOT count as creditable. If you retire and have retiree benefits, you should still enroll in Part B.

Specific to Part D: as long as your employer drug coverage is "creditable" (meets Medicare's minimum standards — which most employer plans do), you can delay Part D without penalty. Your employer must give you an annual notice confirming creditable status.

Common Medicare Timing Mistakes

Patterns I see weekly with Atlanta clients:

Missing the IEP by relying on automatic enrollment. If you're already receiving Social Security at 65, you're auto-enrolled in Parts A and B. If you're not yet on Social Security, you must manually enroll. Many Atlantans miss this.

Assuming COBRA extends the Part B SEP window. It doesn't. SEP clock starts at end of employment, not end of COBRA.

Delaying Part B because spouse's coverage continues. Only works if spouse's employer has 20+ employees AND you're covered as a spouse.

Enrolling in Part B and then trying to switch to Medigap later in Georgia. Outside the initial 6-month Medigap window, Georgia carriers can use medical underwriting. Plan your Medigap enrollment during your initial window.

Letting Medicare Advantage plans auto-renew without re-shopping during AEP. Plans change every year. The 2025 best plan rarely stays the 2026 best plan.

Missing AEP because "everything was fine last year." Drug costs increase, networks change, premiums rise. Always review during AEP.

Trying to enroll in Medicare Advantage outside AEP if you're on Original Medicare. MA-OEP is for current MA enrollees only — not for those switching FROM Original Medicare TO MA.

Not coordinating with Social Security. Some Medicare decisions interact with Social Security claiming timing. Talk to both a broker AND a financial advisor for complex cases.

Frequently Asked Questions

Do I have to enroll in Medicare at 65? No, not if you have qualifying employer coverage. But for most people without employer coverage at 65, enrolling during IEP is the right move.

What if I'm covered under my spouse's plan and they're still working? If your spouse's employer has 20+ employees and the plan covers you, you can delay Part B without penalty. Their plan is primary. Once they retire or you lose that coverage, your 8-month SEP starts.

Can I enroll in Medicare online? Yes — through SSA.gov. Sign up via Social Security 3 months before you turn 65 to time coverage correctly.

What's the difference between AEP and MA-OEP? AEP (Oct 15-Dec 7) is for everyone making annual changes. MA-OEP (Jan 1-Mar 31) is only for people already on Medicare Advantage who want a do-over.

What if I missed my IEP? You can enroll during the next General Enrollment Period (Jan 1-Mar 31) or if a Special Enrollment Period applies. Late penalties likely apply.

Are there penalties for late Medigap enrollment? No specific "late enrollment penalty" like Part B/D — but in Georgia, missing your initial 6-month Medigap window means carriers can use medical underwriting outside that window. Outside the window, you may be denied or charged higher rates based on health.

What happens if I'm still working past 65 and don't sign up? If your employer has 20+ employees and provides creditable coverage, no penalties — but you must enroll within 8 months of losing employer coverage. Confirm your employer's status with HR.

Can I delay Part A? You can, but most people shouldn't. Part A is free for anyone with 40+ work quarters and provides hospital coverage. The only reason to delay Part A is if you're contributing to an HSA (HSA contributions stop once you enroll in Medicare).

The Bottom Line

The single most consequential Medicare decision isn't which plan to pick — it's when to enroll. Missing your initial enrollment window creates lifetime penalties that compound over 20 years of Medicare coverage. Getting the timing right is free; getting it wrong is forever.

For most Atlanta retirees, the right approach is:

3-4 months before turning 65: Start the Medicare research. Decide between Medicare Advantage and Medigap.

3 months before turning 65: IEP opens. Enroll in Part A, Part B, and either MA or Medigap + Part D.

Every year October-December: Review your plan during AEP. Re-shop annually.

If you're approaching 65 and don't know where to start, or you've been working past 65 and aren't sure when to enroll, book a 15-minute call with me. I'll walk through your specific timing — your current coverage, your retirement date, your spouse situation — and tell you exactly when to enroll and what to enroll in. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out What's the Difference Between Medicare Advantage and Medigap?, or Final Expense Insurance: The Policy Most Atlantans Overlook (same retiree audience). The cost-specific Medicare breakdown publishes Monday May 25.

Once you've decided when to enroll, the next question is what it actually costs. See What Does Medicare Cost in 2026?

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not medical, tax, or legal advice. Medicare rules, premium amounts, penalty calculations, and Georgia-specific Medigap rules change.