Do I Need Life Insurance If I'm Self-Employed in Atlanta?

Author: Justin Bishop · June 19, 2026 · 10 min read

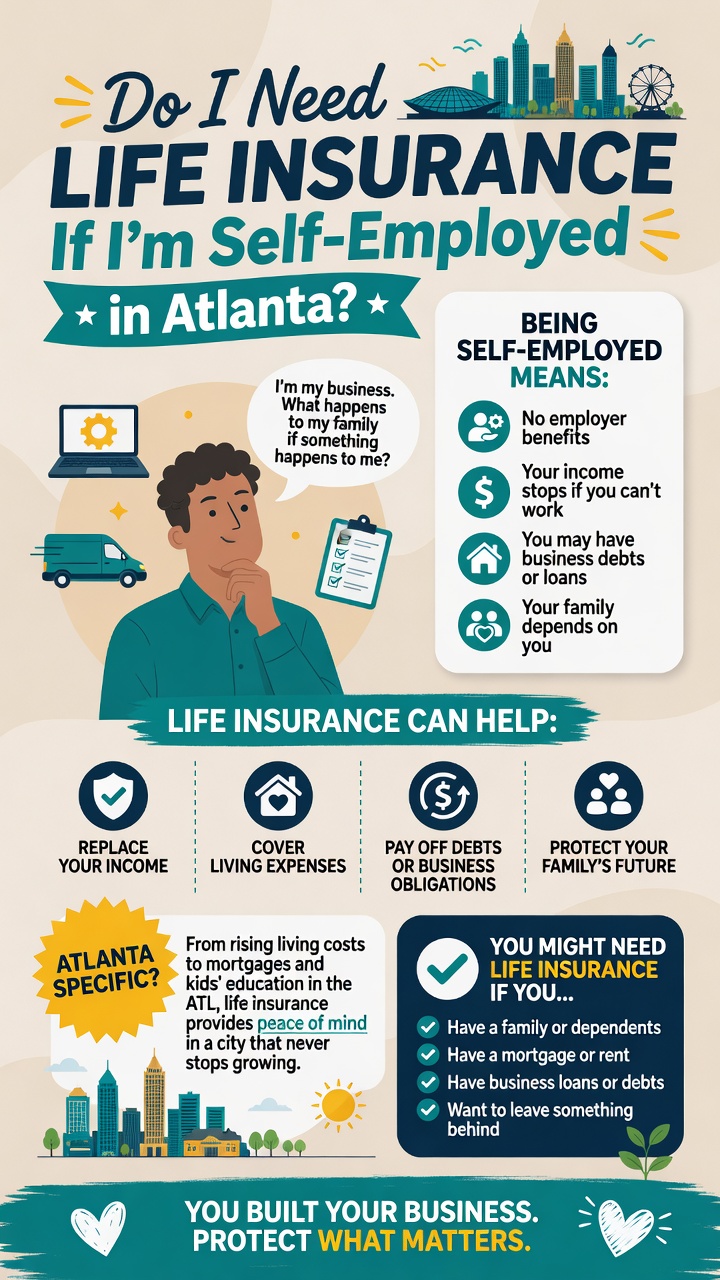

If you are self-employed in Atlanta — whether you run a one-person consulting business, own a 6-person agency in Buckhead, do contract work for tech companies in Tech Square, or have a real estate practice across the metro — you have probably skipped the life insurance conversation. Most self-employed people I talk to fall into one of three groups: they have never seriously thought about it, they thought about it once and got overwhelmed by the choices, or they bought a small policy years ago that no longer fits their actual financial situation.

The honest reality: self-employed people in Atlanta need life insurance more than W-2 employees, not less. A typical W-2 employee gets some employer-provided life coverage as a benefit (usually 1-2x salary). You don't. A typical W-2 employee has reasonably predictable income. Yours fluctuates. A typical W-2 employee has no business debt. You might have SBA loans, lines of credit, equipment financing, or a lease that survives you. And a typical W-2 employee's family has multiple paths to recover financially if something happens to the earner. Your family often has fewer.

This post walks through why self-employed people in Atlanta face unique life insurance considerations, the three real reasons you almost certainly need coverage, term vs whole life for the self-employed buyer, how much you actually need (using the DIME method plus business-specific considerations), the income documentation challenge that catches self-employed applicants off guard, real Atlanta 2026 cost math, and brief notes on key person and buy-sell coverage for those with partners or employees.

I'm Justin Bishop, an independent broker in Atlanta. I write life insurance for self-employed Atlantans every week — and the conversation often starts with "do I even need this?" Here's the honest framework.

The 30-Second Version

Yes, you almost certainly need life insurance if you have a spouse, children, or anyone financially dependent on your income, AND/OR you have business debt or a lease/loan that does not extinguish on your death.

The three real reasons self-employed Atlantans need it more than W-2 workers: No employer-provided coverage (you have to buy your own, period) Business debt and obligations (SBA loans, lines of credit, equipment financing, leases — these don't disappear if you do) Family income protection (your family loses your full income, not a salary that maybe gets replaced)

Term vs whole life for self-employed: Term: cheaper, covers a specific window (10-30 years), most self-employed people start here. Right answer for most. Whole life or permanent: more expensive, lasts your lifetime, builds cash value. Useful for specific situations (estate planning, buy-sell funding, supplemental retirement vehicle). For most self-employed Atlantans under 50, a 20- or 30-year term policy is the foundation. Add permanent coverage strategically if specific needs justify it.

How much you need: Standard methodology is the DIME method (Debt + Income replacement + Mortgage + Education) — for self-employed, add business debt and lease obligations. Most working-age self-employed Atlantans land at $500K-2M of total coverage.

The income documentation challenge: carriers want to see 2-3 years of tax returns showing income. Self-employed people with new businesses, recent income jumps, or significant deductions can face underwriting friction. Plan ahead.

Atlanta 2026 term life pricing benchmarks: a healthy 35-year-old non-smoker can typically buy $1M of 20-year term for $35-55/month. A 45-year-old runs $75-125/month for the same coverage. Smoking, health conditions, or risky hobbies materially change the math.

The most common mistake: waiting until "the business is stable" or "I make more money." Premiums go up every year you wait. Your health can change. The right time to buy is now, while you are healthy and rates are lowest.

The right move for most self-employed Atlantans: a 20- or 30-year term policy sized using the DIME method plus business debt, layered with a small permanent policy only if specific estate/business needs justify it.

Why Self-Employed People Need Life Insurance More Than W-2 Workers

This framing surprises most self-employed people, but the structural realities are clear once you compare side-by-side.

W-2 employees typically have:

Employer-provided life insurance (usually 1-2x salary at no cost to the employee, plus the option to buy more at group rates)

Reasonably predictable income that the family can plan around

Limited business debt (their personal liability is mostly mortgage and credit cards)

A clear path to disability or unemployment benefits if something happens

A spouse who can plan around the dependent income with reasonable certainty

Self-employed people typically have:

Zero employer coverage. Every dollar of life insurance is a dollar they have to fund themselves.

Variable income. Family planning around a $200K average year is harder when the actual range is $130K-280K.

Real business debt and obligations. SBA loans (often with personal guarantees), equipment financing, office leases, line-of-credit balances, contractor payments owed at any given moment. These do not extinguish on death — they become claims against your estate.

No safety net. No employer disability, no unemployment benefits in the traditional sense, no group plan that continues for a window after they stop earning.

A spouse who often has zero visibility into the business's actual financial picture day-to-day. The administrative cleanup if something happens is dramatically harder when the spouse hasn't been involved.

The structural deficit means a self-employed person with the same income as a W-2 employee should typically carry more life insurance, not less. The math is not subtle.

The Three Real Reasons Self-Employed Atlantans Need Life Insurance

Reason 1: No Employer-Provided Coverage

A typical Atlanta W-2 employee with a $100K salary often has $100K-200K of employer-provided life insurance at no out-of-pocket cost. Many companies also offer voluntary supplemental coverage at group rates that are well below individual market pricing.

You have none of that. Every dollar of life insurance you carry is one you buy and pay for individually. Most self-employed people skip this entirely because they don't see the obvious benefit deduction the way W-2 workers see their employer paying.

The cost of not having coverage shows up only after you can't fix it. Family members of self-employed people who died without coverage typically face:

A mortgage they can no longer afford

Business debts that wipe out savings

A scramble to find income replacement (with no employer pension or 401(k) match continuing)

Estate complications when the business needs to be sold or wound down

Reason 2: Business Debt and Obligations Don't Disappear

If you have an SBA loan, line of credit, equipment financing, or a meaningful office or storefront lease, those obligations survive you. Specifically:

SBA loans typically include personal guarantees. If you die with an outstanding SBA loan balance, the lender comes after your estate. Your family loses assets to satisfy the debt.

Lines of credit at banks are usually personally guaranteed. Same dynamic — your estate is on the hook.

Equipment financing for vehicles, machinery, computers, or office furniture continues until paid off. Your business may not be able to keep operating to generate the income to keep paying.

Office or retail leases can run 3-5 years remaining at any moment. Your estate is responsible for the remaining term unless a sublease can be arranged.

Contractor and vendor balances owed at the moment of death become claims against your estate.

A typical Atlanta small business owner has $50K-300K of business obligations that would land on their family if something happened tomorrow. Life insurance specifically sized to cover these obligations protects the family from having to liquidate personal assets.

Reason 3: Your Family Loses Your Full Income, Not a Replaceable Salary

When a W-2 employee dies, the family loses one salary but can often find similar employment in the same industry at similar pay (assuming the surviving spouse is in the workforce). The salary is the income.

When a self-employed person dies, the family loses the entire economic engine — not just a salary, but the business itself, the client relationships, the equity in the business, the future earning potential, and any business asset value that was tied up in personal sweat equity.

The replacement math is brutal. A spouse who has never run the business cannot pick it up where you left off. A new owner buying the business pays for assets and goodwill, not for what you would have earned if you kept running it for 15 more years.

For most self-employed Atlantans, the income protection alone — 10-15 years of household income replacement — drives the need for substantial coverage.

Term vs Whole Life for the Self-Employed Buyer

This decision is covered in depth in What's the Difference Between Term Life and Whole Life? — the short version specifically for self-employed buyers:

Term life (the foundation for most self-employed Atlantans):

Covers a specific window — 10, 15, 20, or 30 years

Significantly cheaper than permanent coverage (often 5-15x cheaper for the same death benefit)

No cash value or investment component

Right answer for the income-replacement and debt-coverage needs that drive most self-employed life insurance purchases

Best matched to the working years when your family is dependent on your income and your business has debt

Whole life or permanent (specific use cases only):

Lasts your entire life as long as premiums are paid

Builds cash value over time (slowly at first, more meaningfully after 10-15 years)

Costs 5-15x more than equivalent term coverage

Right answer for specific situations: estate planning when you have meaningful assets, buy-sell funding for partnerships, supplemental retirement vehicle for high earners who have already maxed retirement accounts

Often oversold by commissioned salespeople to people who would be better served by term plus separate investing

For most self-employed Atlantans:

Start with a 20- or 30-year term policy sized to your DIME-plus-business-debt total

Add permanent coverage only if you have specific needs that term cannot solve (partnership buy-sell, estate liquidity, dependent care for a special needs child, etc.)

Avoid the trap of buying whole life as a savings vehicle when you have not yet maxed retirement accounts — for most self-employed people, an HSA-eligible health plan and SEP-IRA or solo 401(k) wins for retirement savings, not life insurance cash value

How Much Life Insurance Do You Actually Need?

The standard methodology is the DIME method, covered in depth in How Much Life Insurance Do You Actually Need in 2026?. For self-employed buyers, add business obligations on top.

DIME for self-employed Atlantans:

D — Debt. All personal debt (mortgage excluded, that's covered separately) plus business debt (SBA loans, lines of credit, equipment financing, lease obligations). For self-employed, business debt often doubles or triples the personal debt figure.

I — Income replacement. 10-15 years of your typical annual household income. For variable-income self-employed people, use a 3-year average or a conservative estimate. If your typical year is $150K, that's $1.5M-$2.25M of income replacement need.

M — Mortgage. Your remaining mortgage balance. Atlanta median home values mean this often runs $200K-500K.

E — Education. $100K-200K per child for college (Georgia in-state) or more if you're targeting private universities.

Add for self-employed:

Business wind-down costs. Funds to pay employees through a transition, satisfy contractor balances, settle the lease, and close the business cleanly. Typically $50K-200K depending on business size.

Family administrative buffer. Cash for the surviving spouse to keep household running while estate is settled. Typically 6-12 months of household expenses.

The typical Atlanta self-employed person's number:

Solo consultant or freelancer, no employees, no business debt, two kids under 12: $500K-1M total coverage

5-person agency owner, modest SBA loan, two kids: $1M-2M total coverage

15-person business owner with significant business assets and debt, three kids: $2M-4M total coverage

Multi-business owner with substantial debt and equity-locked-up wealth: $3M-7M+ total coverage

These are starting points. Real situations get refined through a 20-minute conversation about your specific business and family setup.

Atlanta 2026 Term Life Pricing Benchmarks

Real numbers for $1M of 20-year level term policy, healthy non-smoker, average build:

30-year-old: $25-40/month

35-year-old: $35-55/month

40-year-old: $50-80/month

45-year-old: $75-125/month

50-year-old: $130-220/month

55-year-old: $230-380/month

Variations that materially change pricing:

Smoking or recent nicotine use (vaping included on most carriers): often 2-3x the non-smoker rate

Health conditions (managed diabetes, controlled hypertension, treated cardiac history): 25-100% premium increases depending on severity and control

Risky hobbies (private piloting, scuba diving, motorcycle riding, certain rock climbing): 10-40% surcharges or specific exclusions

Higher coverage amounts: $2M and above qualify for better per-thousand pricing in some bands, so the per-million cost can actually drop slightly

Permanent coverage benchmark for context:

A $250K whole life policy on a 40-year-old healthy non-smoker typically runs $250-400/month — roughly 5-8x the cost of a comparable term policy. The cost difference is why most working-age self-employed Atlantans should start with term and add permanent only for specific needs.

Key Person and Buy-Sell Coverage (Brief Notes for Specific Situations)

Two specialized use cases worth mentioning for self-employed buyers with employees or partners.

Key person life insurance:

If your business has employees who depend on the business continuing to operate, key person coverage on you (or on a critical employee) protects the business from losing its core revenue generator unexpectedly.

The business owns the policy, pays the premium, and is the beneficiary

The death benefit gives the business cash to recruit a replacement, satisfy obligations during the transition, or wind down cleanly

Common amounts: $500K-2M for a typical Atlanta small business

Tax treatment: premiums are not deductible, death benefit is generally received tax-free

Buy-sell life insurance:

If you have a business partner (in an LLC, S-corp, or partnership), a buy-sell agreement funded by life insurance ensures that if either partner dies, the surviving partner has the cash to buy out the deceased partner's family.

Each partner takes out a policy on the other (or the business takes them out on each partner)

The death benefit funds the buyout per the partnership agreement

Prevents the surviving partner from being forced into business with the deceased partner's spouse or heirs

Common amounts: equal to each partner's estimated equity value in the business

Often paired with a formal buy-sell agreement drafted by an attorney

Both are specialized topics that deserve their own posts. For most solo self-employed Atlantans, neither applies — you only need personal coverage for income replacement and debt protection. For business owners with partners or employees, the conversation gets more layered.

Common Mistakes Self-Employed Atlantans Make Buying Life Insurance

Patterns I see weekly:

Waiting until "the business is stable." Premiums go up every year you age. Your health can change. The right time to buy is when you are healthy, not when the business looks "ready"

Buying too little. A $250K policy sounds like a lot until you compare it to actual household needs (income replacement + business debt + mortgage + education). Most self-employed buyers under-buy

Buying through the wrong broker. Captive agents who can only sell one carrier's products often can't get you the best price or the best underwriting decision. Independent brokers who shop multiple carriers serve self-employed buyers better

Skipping the medical exam to save time. No-exam policies are convenient but cost 20-40% more for the same coverage. For most healthy applicants, taking the exam saves real money

Buying whole life when you don't need permanent coverage. Salespeople paid on whole life commission have a structural incentive to sell whole life. For most self-employed buyers under 55, term covers the actual need at a fraction of the cost

Not updating beneficiaries after life changes. Divorces, marriages, kids born, business partnerships dissolved — beneficiary designations need to keep up. Stale designations create estate problems

Not coordinating personal and business coverage. If you have a partner, your personal policy and any business policies should be designed together, not separately

Ignoring the underwriting class. "Standard" rates are 20-40% higher than "Preferred" or "Preferred Plus" rates. Working with a broker who knows how to position your application matters

Forgetting about disability coverage. Life insurance protects against death; disability insurance protects against the more common scenario of being unable to work due to injury or illness. Different products, both relevant for self-employed people

Letting the policy lapse during a slow business year. A missed premium can lock out re-underwriting at the same rate. Set up automatic payments and treat the premium as non-negotiable

Frequently Asked Questions

Can I deduct life insurance premiums as a business expense if I'm self-employed? Generally no for personal coverage where you or your family are the beneficiary. Yes in specific business contexts — key person coverage premiums are generally not deductible to the business, but the death benefit is received tax-free. Group term life provided to employees up to $50,000 is deductible to the business. Talk to your CPA about your specific situation.

Do I have to take a medical exam? For most policies, yes. The exam is straightforward — height, weight, blood pressure, blood and urine samples — and usually done at your home or office. For smaller policies (under $500K) some carriers offer no-exam underwriting at a price premium of 20-40%. Most healthy self-employed applicants save money by taking the exam.

How long does the application process take? Typically 4-8 weeks from application submission to policy issued, including medical exam scheduling, lab results processing, and underwriting review. Faster turnarounds are possible (some no-exam policies issue in 24-72 hours) at higher cost.

What if I have a pre-existing health condition? Depends on the condition. Managed conditions like controlled hypertension, treated thyroid issues, or stable diabetes typically qualify for coverage at modified rates. More serious conditions (recent cancer, untreated mental health issues, recent cardiac events) may require waiting periods or face higher premiums or coverage limits. Working with an independent broker who shops multiple carriers is essential — underwriting decisions vary significantly across carriers for the same applicant.

Can my spouse get coverage too if she doesn't work outside the home? Yes. Stay-at-home spouses still have significant economic value to the household (childcare, household management, eldercare). Most carriers will write coverage on a non-working spouse equal to a multiple of the working spouse's income. Don't skip this — losing a stay-at-home spouse creates substantial new household expenses.

What happens to my policy if I close my business and become a W-2 employee later? Nothing — your personal policy is yours regardless of how you earn income. The premium and coverage stay the same. The opposite is also true: a W-2 employee who becomes self-employed keeps any existing personal coverage. This is exactly why the right time to buy is now, while you are healthy, not later when the business situation changes.

Should I buy a policy for my children? Generally no for income protection (children don't generate household income). Some buyers consider small permanent policies on children as a way to lock in their insurability at low rates — debatable value, often oversold. Focus the family's life insurance budget on the income earners first.

What if I die owing the IRS or other government debt? Personal income tax debt is collectable from your estate, and life insurance death benefits paid to your estate are subject to estate creditor claims. To protect the death benefit from creditor claims, the policy can be owned by an irrevocable trust or named to beneficiaries directly. This is an estate planning conversation as much as an insurance conversation.

The Bottom Line

If you are self-employed in Atlanta and you have a spouse, children, or anyone financially dependent on your income — or you have business debt or lease obligations that survive you — you almost certainly need life insurance. The structural realities of self-employment make life insurance more important for you than for a typical W-2 employee, not less.

The right starting point for most self-employed Atlantans is a 20- or 30-year level term policy sized using the DIME method plus your specific business debt and obligations. For most working-age self-employed people, this lands somewhere between $500K and $3M of total coverage at $50-200/month in premium depending on age and health.

Add permanent coverage only if you have specific needs that term cannot solve — partnership buy-sell funding, estate liquidity, supplemental retirement vehicle for high earners with maxed retirement accounts.

The single most important thing: don't wait. Premiums go up every year you age. Your health can change. The cheapest policy you will ever buy is the one you buy this week.

If you are a self-employed Atlantan trying to figure out whether you need coverage, how much, and which carrier to apply with — book a 15-minute call with me. I'll walk through your specific situation, run the DIME math, and quote across multiple carriers to find the best price for your underwriting profile. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out How Much Life Insurance Do You Actually Need in 2026? for the deeper DIME methodology, What's the Difference Between Term Life and Whole Life? for the term-vs-permanent decision, or The 2026 ACA Subsidy Cliff for Self-Employed Georgians for related self-employed financial planning.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal, tax, or financial advice. Life insurance pricing, underwriting standards, and tax treatment can change.