Self-Employed in Georgia? The 2026 ACA Subsidy Cliff Is Back. Here's What to Do.

Author: Justin Bishop · April 30, 2026 · 8 min read

If you're self-employed in Georgia and your January 2026 marketplace renewal letter made you genuinely angry, you're not alone — and what happened isn't your insurer's fault.

The federal government turned off a multi-year subsidy expansion on December 31, 2025. The result: marketplace premiums for unsubsidized buyers jumped roughly 114% on average. For self-employed people, who account for about 82% of the people who were claiming the now-expired enhanced subsidies, the impact is concentrated and brutal.

Travel nurses near the cliff: Health Insurance for Travel Nurses guide.

I'm Justin Bishop, an independent broker in Atlanta. I work with a lot of self-employed clients, and the calls I'm getting in 2026 sound the same: "My premium doubled. What happened? What do I do?"

Here's the honest version — what changed, why it matters, and what you can actually do about it.

Mortgage lenders managing rate-driven volatility: Health Insurance for Mortgage Lenders guide

What Actually Changed on January 1, 2026

For four years (2021–2025), the federal government expanded ACA premium tax credits under the American Rescue Plan and the Inflation Reduction Act. Two things made these "enhanced" subsidies different from the original ACA:

They made marketplace plans much cheaper for people earning between 100% and 400% of the federal poverty level (FPL).

They eliminated the "subsidy cliff" entirely — meaning even high earners qualified for help if their premium would otherwise exceed 8.5% of their income.

Both expired December 31, 2025.

Starting January 1, 2026, the rules reverted to the original ACA structure:

Subsidies are still available between 100% and 400% of FPL — but at lower amounts than 2021-2025

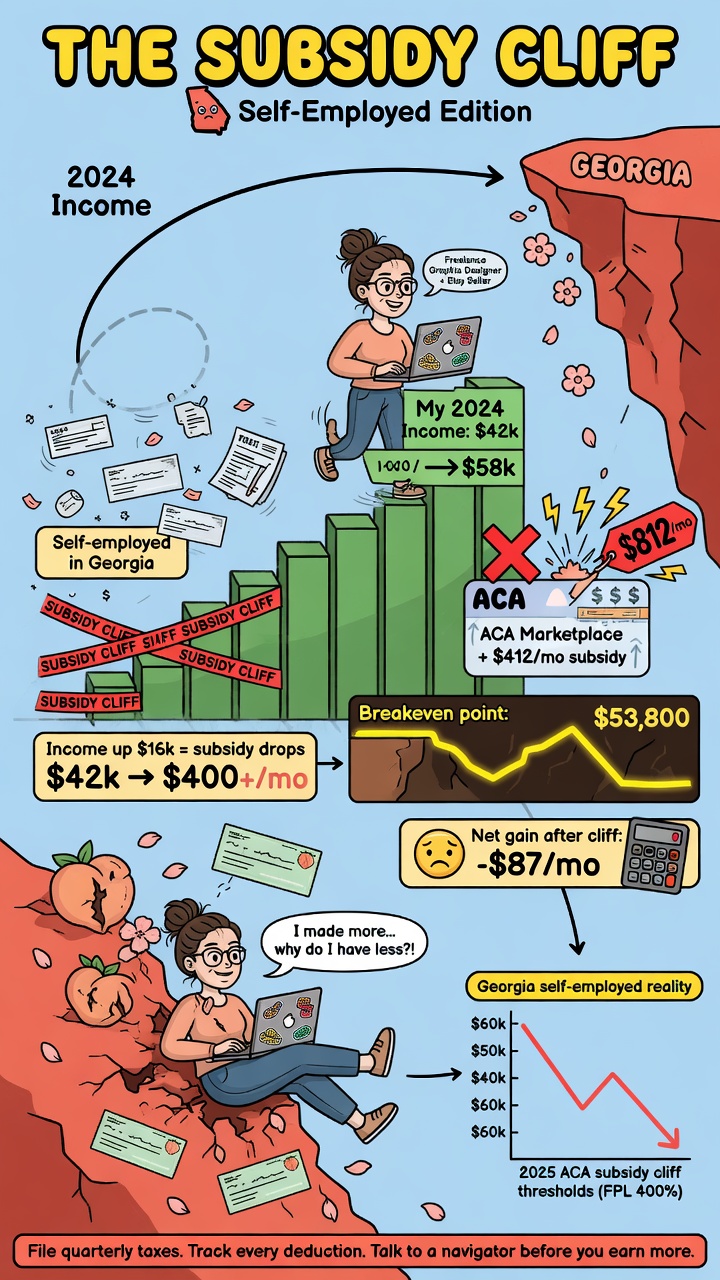

Above 400% FPL, the subsidy cliff is back. Earn one dollar over and you lose all premium tax credits, not just a portion.

People who were paying $200/month in 2025 with help are paying $400, $600, sometimes $1,200/month in 2026.

That's the whole story. The subsidies didn't get reduced — they got cliffed.

For the broader Georgia marketplace overview, see Georgia Health Insurance Marketplace: A 2026 Guide

The 400% FPL Cliff in 2026 — The Numbers That Matter

Here's where the line falls for 2026:

Household size400% FPL (2026)Above this, no subsidy1 person~$60,240Lose all PTC2 people~$81,760Lose all PTC3 people~$103,280Lose all PTC4 people~$124,800Lose all PTC

(These numbers update annually; the 2026 FPL guidelines were published in early 2026. Verify current figures with your CPA or the federal poverty guidelines if you're close to the cliff.)

A family of four earning $124,799 may pay $0/month in some scenarios. The same family at $124,801 pays the full premium — sometimes $1,800/month.

That's the cliff. Single dollar of income over the threshold, thousands of dollars of consequence.

Why Self-Employed People Get Hit Hardest

Three reasons:

1. Income variability. A W-2 employee at $90K salary is at $90K. A 1099 contractor "expecting" $90K might end up at $110K because Q4 was great. The marketplace site doesn't have a category for "depends." We have to project — and projecting wrong on the high side means owing back subsidies at tax time. Projecting wrong on the low side means paying more for the year.

2. No employer plan as a fallback. A W-2 employee whose subsidy disappears might just shrug and take their employer's group plan. A self-employed person doesn't have that option.

3. The deduction-vs-MAGI math is unique. Self-employed people have specific tools — SEP-IRA, solo 401(k), HSA contributions, the self-employed health insurance deduction itself — that can lower their MAGI to stay under the cliff. But none of that happens automatically. You have to plan for it.

The good news in #3 is also the actionable news. The cliff is harder for self-employed people, but self-employed people also have more levers to pull than W-2 employees do. Most just don't know it.

5 Legal Levers for Staying Under the Cliff

The strategy is simple in theory: get your projected MAGI (modified adjusted gross income) under 400% of FPL, and you keep the subsidy. Every dollar of MAGI you can legitimately reduce — through retirement contributions, HSA, expense timing, or specific deductions — is a dollar that helps.

Here are the five biggest levers, in rough order of leverage:

1. Solo 401(k) or SEP-IRA contributions

If you have business income, contributing to a solo 401(k) or SEP-IRA reduces your MAGI dollar for dollar (for traditional contributions, not Roth). For 2026:

Solo 401(k) — up to $23,500 employee contribution + employer profit sharing (potentially $70,000 total combined). This is the biggest lever for most freelancers and consultants.

SEP-IRA — up to 25% of net self-employment earnings, capped at $70,000.

A consultant earning $90,000 of net self-employment income who contributes $20,000 to a solo 401(k) drops their MAGI to ~$70,000 — well below the single-person cliff at $60,240… well, ok, that's still over. Let me try a real one: a consultant earning $70,000 net who contributes $15,000 to a solo 401(k) drops MAGI to ~$55,000. That keeps them on the marketplace subsidy and may save them $5,000+ in premium over the year — a return on the 401(k) contribution that's separate from the retirement growth.

This is the single most powerful lever for self-employed people near the cliff. Talk to your CPA about whether your situation supports it.

2. HSA contributions (if you have an HSA-eligible plan)

If you're enrolled in an HSA-eligible high-deductible health plan, HSA contributions also reduce MAGI dollar for dollar. 2026 limits:

$4,400 for self-only HDHP coverage

$8,750 for family HDHP coverage

+$1,000 catch-up if you're 55+

Lower premium + tax-deductible savings + triple tax advantage on the account itself + reduces MAGI to keep you under the cliff. Strong combination for self-employed people in good health who don't expect heavy medical spending.

Full breakdown of HSA mechanics, 2026 limits, and the strategic moves: HSA Contribution Limits 2026 guide

3. The self-employed health insurance deduction

If you pay your own health insurance premiums, you can deduct 100% of those premiums as an above-the-line deduction on Schedule 1 of your 1040. This deduction reduces your AGI directly — and AGI is the basis for MAGI.

The math is recursive: the deduction reduces your MAGI, which can keep you eligible for subsidies, which reduces your effective premium, which reduces your deduction, which... It iterates. Most decent CPAs and tax software handle the iteration automatically; if you DIY your taxes, get help on this one specifically.

4. Expense timing for cash-basis filers

If you file cash basis (most freelancers do), you can sometimes shift income or expenses across year-end to manage MAGI. Common moves:

Pay business expenses before December 31 to lower current-year income (computer, professional services, education, business travel, equipment, etc.)

Defer billing/collection for late-year work into the following year (only if your client is willing — don't strain a client relationship for this)

Accelerate charitable giving (if you itemize, which fewer self-employed people do post-TCJA)

These are smaller-impact moves than 401(k) contributions but they stack with everything else.

5. Spouse-on-payroll structure (if you're an LLC or S-corp)

Specific to certain business structures: if you have an LLC or S-corp and your spouse has been doing legitimate work in the business, putting them on actual W-2 payroll (with real wages, real W-2, real work) opens up additional retirement contribution capacity through their compensation, can offer them health benefits separately, and in some configurations qualifies the business for small-group health insurance instead of marketplace coverage entirely.

This isn't a generic "spouse on payroll" hack — it has to be a real employment arrangement, and the IRS scrutinizes these. But if it fits your real situation, it can be the difference between marketplace headaches and group coverage you control.

Talk to your CPA before doing this. Don't just decide based on a blog post.

What If You're Already Over the Cliff?

If your MAGI is genuinely going to be over $60K single / $80K couple / $105K family of four, and the levers above can't get you under, you're not stuck — but the marketplace is no longer your cheapest option. Here are the alternatives:

Spouse's employer plan. If your spouse has W-2 coverage available, run the numbers. Spouse coverage is often the cheapest path for high-earning self-employed couples.

"Group of one" via your LLC. Putting your spouse on real W-2 payroll can sometimes qualify the business for small-group health insurance, which doesn't have a subsidy cliff. Specific eligibility varies by carrier.

Off-marketplace plans. Same insurance products as marketplace plans, sometimes priced differently, no subsidy involved either way. Worth comparing if you're paying full freight anyway.

Health share ministries. Not insurance, but a real cost-sharing alternative for healthy people. Read the membership guide carefully — pre-existing conditions, mental health, and maternity often have major restrictions.

Short-term medical (limited use case). Cheaper monthly premium but not ACA-compliant; doesn't cover pre-existing conditions, has annual benefit caps. Useful as a 2-3 month bridge if you're between jobs or aging into Medicare; not a long-term solution.

I write more about all five paths on the self-employed health insurance page — that's where the deep version lives.

Real estate agents over the cliff: Health Insurance for Real Estate Agents guide.

What to Do Right Now (Action Items)

If you're self-employed in Georgia and worried about your 2026 coverage, here's the order of operations:

Project your 2026 MAGI carefully. Not your gross revenue. MAGI — after business expenses, retirement contributions, HSA, the self-employed health insurance deduction, half your self-employment tax. If you don't know how to calculate this, that's the first thing to fix.

Compare projected MAGI to the cliff for your household size. Are you under, over, or close enough that one good Q4 puts you over?

If you're under the cliff: keep your marketplace plan. Update Georgia Access with your current projected income before any major income changes. Don't let a Q4 surge silently push you into clawback territory.

If you're close to the cliff: plan retirement contributions and HSA contributions strategically. A few thousand dollars of solo 401(k) at the right time can keep you on the subsidy and pay for itself.

If you're already over: stop paying full freight on a marketplace plan you're not getting subsidized for. Compare off-marketplace plans, group-of-one structures, and your spouse's employer plan.

Run this analysis with help. A 30-minute call with a broker who understands the marketplace + a coordinated conversation with your CPA can save you thousands. The math is genuinely complicated; that's the whole reason this post exists.

For a full breakdown of every legitimate affordable path in Georgia, see Affordable Health Insurance Options in Georgia for 2026.

For the deeper question of which tier to actually pick, see Bronze vs Silver vs Gold: Which Plan Do You Actually Need?.

Newer to Georgia Access? Here's the platform-vs-Healthcare.gov explainer.

If your QLE was income-related (started self-employment, lost a job): see the SEP guide

Gig worker specifically? See the gig worker guide.

Want a Real Number for Your Situation?

If you're self-employed in Georgia and you want to know exactly where you stand on the cliff — text me your projected 2026 MAGI and household size at (706) 988-1930, and I'll come back with where you are, what you'd qualify for, and which lever I'd pull first.

Free. No pressure. No follow-up sequence.

I help self-employed Georgians navigate the marketplace every week. Most people I quote qualify for help they didn't know existed — or have one specific lever they could pull that they didn't realize was an option.

If you have W-2 employees in your LLC...": "Group plans for small businesses: Atlanta Group Health Cost Guide

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, serving self-employed clients across 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not tax or legal advice. Talk to your CPA for your specific situation. Premiums and subsidy thresholds change — call us for current numbers.