How Much Life Insurance Do You Actually Need in 2026?

Author: Justin Bishop · May 8, 2026 · 7 min read

If you've ever Googled "how much life insurance do I need," you've probably seen the same answer everywhere: 10 times your annual income. Or maybe 12 times. Some sites say 7. A few say 20.

The honest truth: those rules of thumb are wrong for most people. Some are dramatically over-insured, paying for coverage they don't need. Most are dramatically under-insured, leaving their families exposed to a financial gap they don't even know exists.

According to LIMRA's 2024 Insurance Barometer Study, 41% of Americans say they don't have enough life insurance, and the average coverage gap is over $200,000. That's the number standing between a grieving family and financial stability.

I'm Justin Bishop, an independent broker in Atlanta. I write life insurance every week — for new parents, business owners, soon-to-retirees, single income families, dual income families. Here's how to actually figure out the right number for your situation.

The 30-Second Version

The "10x income" rule of thumb works for some people, but it ignores debts, dependents, and what your family actually needs to maintain their lifestyle.

The better answer is the DIME method: Debt + Income replacement + Mortgage + Education for kids.

For most working parents in Atlanta, the right number is between $500,000 and $2 million.

Term life insurance for the right amount is usually cheaper than people think — a healthy 35-year-old can get $1M of 20-year term for around $30-50/month.

That's the short version. Below is how to actually run your own number.

Why "10x Your Income" Is the Wrong Answer

Here's the problem with rule-of-thumb math:

It ignores your debts. A 35-year-old making $80,000 with a $400,000 mortgage and $40,000 in student loans needs a very different policy than a 35-year-old making $80,000 with no debts.

It ignores your dependents. One kid vs three kids changes the math completely.

It ignores your spouse's income. If your partner earns the same as you, your coverage need is lower. If they don't work, it's much higher.

It ignores how long your kids will need support. A 5-year-old needs 13+ years of support before college. A 17-year-old needs maybe 4 years.

It ignores final expenses. Funeral costs in Georgia run $9,000-15,000 in 2026 — that's not in the "10x income" math.

The 10x rule is a starting point. It is not the answer.

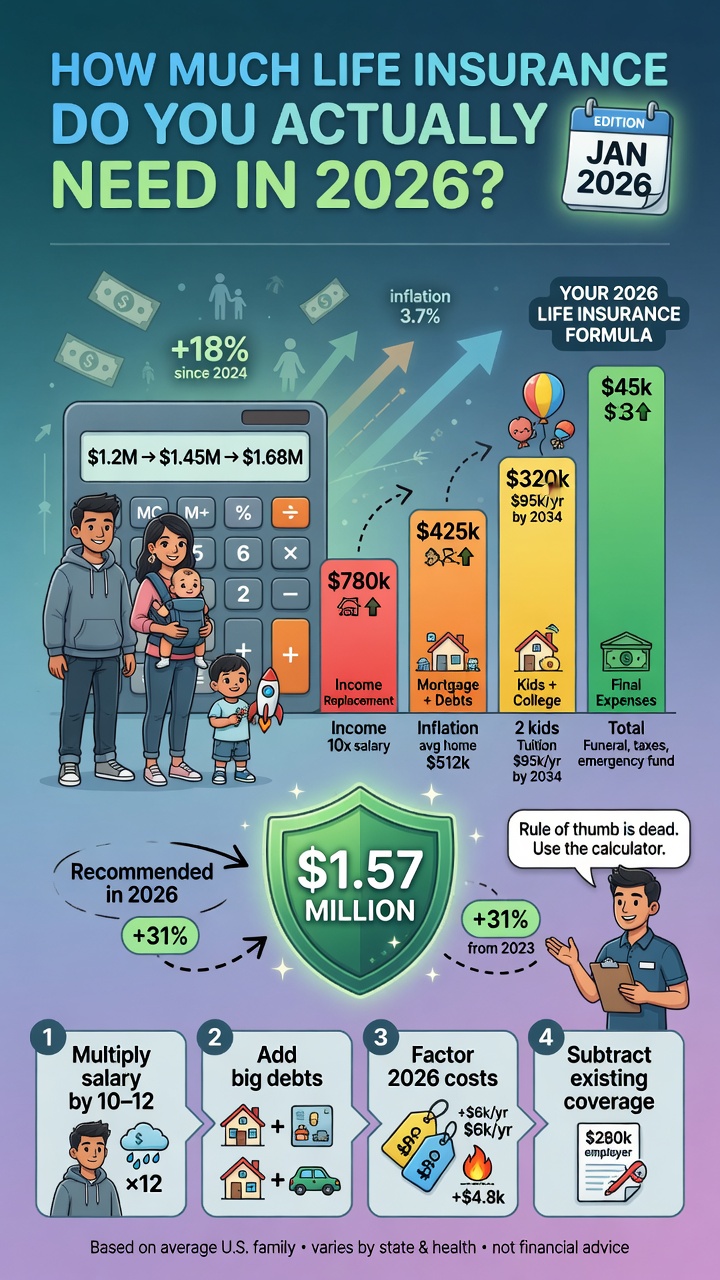

The DIME Method: How to Actually Calculate Your Need

DIME is the standard framework most independent brokers use, and it's the one I walk Atlanta clients through. Here's how it works:

D — Debt

Add up everything you owe except the mortgage:

Credit card balances

Auto loans

Student loans

Personal loans

Outstanding business debts (if you're an owner)

This is what would need to be paid off so your family isn't carrying it.

I — Income Replacement

Multiply your annual income by the number of years your family needs support. The standard is 10 years as a baseline. Adjust based on:

Younger kids = more years. If your youngest is 3, 15+ years is reasonable.

Older kids = fewer years. If your youngest is 17, 5 years may be enough.

Working spouse with similar income = fewer years. Maybe 5-7.

Single-income household = more years. Sometimes 15-20.

For an Atlanta parent making $90,000 with two young kids, 10-12 years is typical. That's $900,000-1,080,000 just for income replacement.

M — Mortgage

The remaining balance on your home loan. The goal is for your family to be able to pay off the house and never worry about losing it. For an Atlanta family with a typical $400,000 mortgage and $300,000 remaining, that's $300,000.

E — Education

What it would cost to fund your kids' college education. Rough 2026 numbers:

In-state public (UGA, Georgia Tech, Georgia State): ~$30,000/year, 4 years = $120,000 per kid

Private or out-of-state: $60,000-80,000/year, 4 years = $240,000-320,000 per kid

Trade school or community college: $20,000-40,000 total

For two kids both going to in-state public, you'd budget $240,000.

Add It All Up

For our example Atlanta parent — $90K income, two young kids, $300K mortgage remaining, $25K of consumer debt, plus 10 years income replacement at $90K, plus $240K for two kids' in-state college:

Debt: $25,000

Income: $900,000

Mortgage: $300,000

Education: $240,000

Total need: ~$1.46 million

That's about 16x annual income. The "10x" rule of thumb would have under-insured this person by $560,000.

Variables That Change the Math

Real life is messy. Here are the most common variables I see with Atlanta clients:

Stay-at-home parent: add the cost of childcare, housekeeping, and household management. The economic value of a stay-at-home parent is roughly $80,000-100,000/year. Calculate that into the income replacement portion.

Business owner: add buy-sell agreement coverage, key-person coverage, and business debt obligations. Personal life insurance and business life insurance are different policies.

Plans to retire early: if you plan to retire at 55, your life insurance need drops dramatically once you hit that age. Term insurance is usually the right tool because the need has an end date.

Significant existing assets: if you've already saved $500,000 in retirement accounts plus equity in your home, your life insurance need is reduced because there's already a financial cushion.

Special needs dependent: lifetime support requirements change everything. Coverage often needs to be much higher and structured differently (special needs trust, permanent insurance, etc.). This requires a specialist.

How Much Does That Coverage Actually Cost?

Here's the part that surprises most Atlanta parents: term life insurance for the right amount is usually way cheaper than people think.

Sample 2026 monthly premiums for healthy non-smokers (Georgia rates, 20-year term):

30-year-old, $500,000: $20-30/month

35-year-old, $1 million: $30-50/month

40-year-old, $1 million: $50-75/month

45-year-old, $1 million: $90-130/month

50-year-old, $500,000: $80-110/month

Whole life insurance and universal life cost 5-10x more than term. There are good reasons to use them in specific cases (estate planning, business buy-sell, special needs trusts), but for income replacement, term wins almost every time.

Now that you know the amount, decide which type: What's the Difference Between Term Life and Whole Life?.

How Most People Get This Wrong

Patterns I see weekly with Atlanta clients:

Buying coverage equal to their employer-sponsored group life policy — usually 1-2x salary. That's not enough for anyone with a family or mortgage.

Using a "10x income" calculator and stopping there — leaves out the mortgage and education numbers most families need.

Skipping coverage entirely because "it's expensive" — without ever getting a real quote. Most people overestimate the cost by 3-4x.

Letting an employer plan be their entire life insurance — that coverage disappears when you change jobs.

Overbuying whole life when term would do the job for 1/8 the price — common for high-income professionals upsold by captive agents.

Not updating coverage after major life events — new baby, new house, new business, divorce. Each is a coverage trigger.

Waiting until they're "in better shape" to buy — then getting diagnosed with something that makes coverage 5x more expensive or unavailable.

Frequently Asked Questions

Should I count my employer's life insurance toward my total? Partially. Group life insurance through work usually disappears when you leave the job. Treat it as a bonus, not a foundation.

What if I'm single with no kids? Your need is much lower. Most single, no-dependent adults need just enough to cover final expenses ($15,000-25,000) and any outstanding debts. A small whole life or final expense policy often makes more sense than a large term policy.

Does Social Security pay survivor benefits to my family? Yes — and you should factor those in. A surviving spouse with kids under 16 typically receives meaningful Social Security survivor benefits. A licensed agent can help you account for that.

Can I buy life insurance through the marketplace like health insurance? No. Life insurance is sold separately by carriers (or through brokers), not on the ACA marketplace. The application process involves health questions, sometimes a medical exam, and underwriting that typically takes 2-6 weeks.

Do I need a medical exam? Sometimes. Many carriers now offer "no-exam" policies for healthy applicants under 50, with quick approval. For larger face amounts or older applicants, an exam is usually required. The exam is free and usually takes 20 minutes.

What if my health changes after I get coverage? Term life insurance locks in the rate for the policy term (10, 20, 30 years). If your health changes during that period, the rate doesn't change. That's why buying earlier — when you're healthier — usually saves money long-term.

For older adults whose primary need is funeral and burial costs (not income replacement), see Final Expense Insurance: The Policy Most Atlantans Overlook.

The Bottom Line

The right amount of life insurance is the amount that lets your family stay in the house, keep the lifestyle, send the kids to college, and not worry about money if something happens to you.

For most working Atlanta parents, that's somewhere between $500,000 and $2 million of term coverage. For high-earners, business owners, or families with multiple kids, it can be more.

Skip the rule-of-thumb math. Run the DIME calculation. Get a real quote. The number will probably surprise you in both directions — most people are paying too much for too little coverage and don't realize how cheap enough coverage actually is.

If you want a real number for your specific situation, book a 15-minute call with me. I'll walk through DIME with you, pull quotes from 5-7 carriers, and tell you the realistic monthly cost. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out Health Insurance for the Self-Employed (because most self-employed Atlantans are also under-insured on life), or Meet Justin for context on how I work.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not financial, tax, or legal advice. Life insurance underwriting, premium rates, and IRS rules change