How Much Life Insurance Do You Actually Need in 2026?

Author: Justin Bishop · May 8, 2026 · 7 min read

If you've gotten a life insurance quote in the last year, you've probably been pitched whole life. The agent showed you a beautiful illustration with cash value growing year after year, talked about "guarantees," and the monthly premium was 5-10x what a term policy would have cost. They told you whole life was "an investment" or "a forced savings account" or "the best legacy you can leave."

Most of that pitch is misleading. For the right person in the right situation, whole life is the correct tool. For everyone else — which is most people — term life wins, and it isn't close.

I'm Justin Bishop, an independent broker in Atlanta. Because I'm independent, I get paid the same whether you buy term or whole — so I'll give you the honest comparison.

This is what term and whole life actually are, what they actually cost, when each one wins, and the most common ways Atlanta families get sold the wrong one.

The 30-Second Version

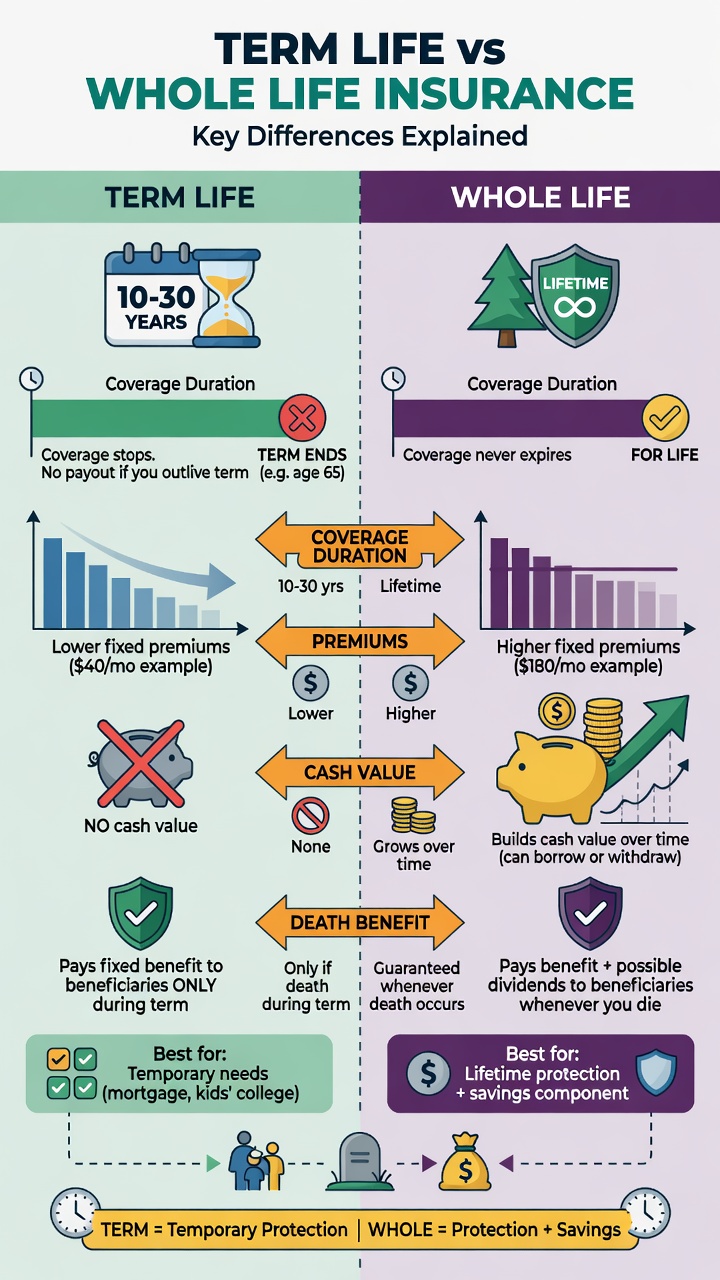

Term life = pure insurance. Pays a death benefit if you die during the policy term. No cash value, no investment component, lowest cost per dollar of coverage. Term wins for most people.

Whole life = insurance + savings/investment combo. Lifetime coverage, builds cash value, costs 5-10x more than term for the same death benefit. Whole wins for specific situations: estate planning, special needs trusts, business buy-sell, and a few other narrow cases.

For 90% of working Atlanta parents: buy as much term as you need (here's how to calculate that) and invest the difference in your 401(k), HSA, or Roth IRA. The math wins almost every time.

If you want the full reasoning, keep reading.

What Term Life Insurance Actually Is

Term life insurance is the simplest financial product on earth:

You pick a coverage amount (e.g., $1,000,000)

You pick a term length (e.g., 20 years)

You pay a level premium each month for the term

If you die during the term, your beneficiaries get the death benefit

If you don't die during the term, the policy expires worthless

That's it. No cash value. No investment. No "borrowing against the policy." It's pure life insurance.

Why it's cheap: because the carrier knows when their risk ends. A 30-year-old buying a 20-year term policy will be 50 when it expires — still well below the average death age. Most 20-year term policies never pay out, which is why the premium is so low.

Common term lengths offered in Georgia: 10, 15, 20, 25, and 30 years. Longer terms cost more.

What Whole Life Insurance Actually Is

Whole life is two products bundled into one:

A life insurance policy that lasts your entire life (assuming you keep paying premiums)

A "cash value" account that grows over time inside the policy

The premium is much higher than term because part of it pays for the lifetime insurance and part of it goes into the cash value account. Cash value grows at a guaranteed minimum rate (typically 2-4%), and policies from "mutual" insurance carriers may pay non-guaranteed dividends on top.

You can:

Borrow against the cash value (with interest charges)

Surrender the policy and take the cash value

Use the cash value to pay premiums in later years

Pass the death benefit tax-free to beneficiaries

Why it's expensive: because the carrier has to guarantee a payout (you will eventually die, and they will eventually pay out), and they're managing an investment component.

For a healthy 35-year-old non-smoker in Georgia, $1 million whole life typically costs $700-1,200/month. A 20-year, $1 million term policy for the same person costs $30-50/month. Same death benefit; whole life is roughly 20x more expensive monthly.

The Real Differences That Matter

Let me break down where these products actually differ:

Cost per dollar of coverage: Term wins by 10-20x. Not close.

Duration of coverage: Whole wins. Term ends; whole lasts as long as you pay.

Cash value: Whole has it; term does not.

Premium predictability: Both have level premiums during the policy. Whole's premium is higher but stays the same. Term's premium is lower but stays the same.

Complexity: Term is simple. Whole is complex (illustrations, dividend assumptions, MEC limits, surrender charges, loan rules).

Liquidity: Whole offers cash value access via loans or surrender. Term offers nothing while you're alive.

Investment returns: Whole's cash value grows slowly (~2-5% annually after fees). Term has no investment component at all — but the premium savings can be invested elsewhere at potentially higher returns.

Tax treatment: Death benefits from both are income-tax-free to beneficiaries. Whole life cash value grows tax-deferred. Loans against cash value are tax-free if structured correctly.

Commission structure: Whole life pays the agent 5-10x more commission than term. (This is why captive agents push it so aggressively.)

Where Term Life Wins (Most People, Most of the Time)

Term is the right answer when:

You have a defined need with an end date. You need coverage while the kids are home, while the mortgage is being paid down, while you're still working. After that, the need shrinks. Term matches that exactly.

You have a tight budget. Term gives you the most coverage for the smallest premium. A young family that needs $1 million of protection can afford term. They can't afford whole.

You'd rather invest the difference yourself. The S&P 500's long-run average return is roughly 8-10%. Whole life's cash value grows at 2-5%. If you're disciplined enough to actually invest the premium difference, you almost always come out ahead.

You don't have estate-planning complexity. Most working families don't. Term covers the income-replacement need cleanly.

You want simplicity. Term insurance isn't sold with 30-page illustrations. The math is straightforward.

For about 90% of Atlanta clients I work with, term is the right answer.

Where Whole Life Actually Wins

I'm not anti-whole life. There are real situations where it's the right tool:

Estate planning for high-net-worth families. Estates above the federal estate tax exemption (~$13.6M single, ~$27.2M married in 2026) face significant estate tax. Whole life held in an irrevocable life insurance trust (ILIT) can pass tax-free outside the estate, paying the tax bill without forcing asset sales.

Special needs planning. Funding a special needs trust with whole life ensures permanent, lifelong coverage that doesn't expire — critical when the dependent's need is permanent.

Business buy-sell agreements. Two business partners can use whole life policies on each other to fund a buyout if one dies. Permanent coverage = permanent funding.

Final expense / "burial insurance." Small whole life policies ($10K-25K) make sense for retirees who want guaranteed coverage of funeral costs without medical underwriting.

For the full deep-dive on final expense as a separate product, see Final Expense Insurance: The Policy Most Atlantans Overlook

High earners who max out all other tax-advantaged accounts (401(k), Roth, HSA, mega-backdoor Roth, etc.) and want additional tax-deferred growth. Whole life is a tertiary option here, not a primary one.

People who genuinely won't invest the premium difference. This is the "forced savings" argument. If you'd otherwise spend that money instead of investing it, the modest cash value growth from whole life beats spending it on a depreciating asset.

For maybe 10% of clients, one of these situations applies. For the other 90%, term is better.

The "Cash Value" Pitch — What to Watch For

Cash value is the centerpiece of every whole life sales pitch. Here's what they don't always tell you:

Cash value takes 7-15 years to break even with what you've paid in premiums. Surrender the policy in year 5 and you'll get back significantly less than what you put in.

Dividends are non-guaranteed. Illustrations show "current" dividend assumptions. Carriers reserve the right to lower them. Many have, especially over the last 20 years.

Loans against cash value charge interest (typically 5-8% in 2026). Unpaid loans + interest reduce the death benefit at death.

The "tax-free retirement income" pitch uses policy loans to extract cash value tax-free. This works, but it's complex, requires permanent commitment, and modest underperformance can collapse the strategy.

MEC rules (Modified Endowment Contract) limit how fast you can fund the policy without losing tax advantages. Aggressive funding strategies can violate MEC and create taxable events.

The cash value isn't fake — it's real money. But it grows slowly, and accessing it is more constrained than the pitch suggests.

"Buy Term and Invest the Difference" (The Math Most Brokers Don't Show You)

Here's the comparison most whole life pitches skip:

Scenario: 35-year-old healthy non-smoker, $1M coverage need, considering 20-year term ($40/month) vs $1M whole life ($800/month)

Whole life: $800/month × 12 × 20 years = $192,000 in premiums over 20 years. After 20 years, cash value might be $130,000-160,000 depending on dividends.

Term: $40/month × 12 × 20 years = $9,600 in premiums over 20 years. The remaining $760/month invested in an S&P 500 index fund averaging 8% annually = $447,000 at the end of 20 years.

After 20 years, the term-and-invest strategy has roughly $300,000 more than the whole life strategy — and you had the same death benefit the whole time.

If you're disciplined enough to actually invest the difference, the math wins almost every time. The catch: most people aren't disciplined enough. That's the honest case for whole life as "forced savings."

Universal Life and IUL — The Hybrid

You may also see "Universal Life" (UL) or "Indexed Universal Life" (IUL) policies. Quick read:

Universal Life: flexible premium and adjustable death benefit. More flexibility than whole life, less than term + investing. Cash value tied to interest rates.

Indexed Universal Life (IUL): flexible premium with cash value tied to a stock index (e.g., S&P 500) with caps and floors. Marketed as "upside without downside" — the reality is more nuanced. Caps limit upside; fees and cost-of-insurance charges can erode value.

Both are more complex than whole life, more expensive than term, and have specific use cases (executive benefit programs, certain estate strategies). For most Atlanta clients, neither is the right primary policy.

How Most People Get the Term vs Whole Decision Wrong

Patterns I see weekly:

Buying whole life from a captive agent without comparison shopping. The agent at a single carrier only sells that carrier's products. Independent brokers can compare across carriers AND across product types.

Treating whole life as an "investment" rather than insurance. It's primarily insurance. The investment component is secondary and underperforms most other investment options.

Buying small amounts of whole life when much larger amounts of term were affordable. A young family buying $250K of whole life "because it's permanent" when they actually needed $1.5M of coverage is dramatically under-protected. The correct move was $1.5M of term for the same monthly premium.

Believing the "rates will go up if you wait" pressure. Sometimes true, but term life rates have been remarkably stable. Don't let urgency override analysis.

Skipping the term conversion rider. Most term policies allow you to convert to permanent coverage later without medical underwriting. If your situation changes, you can adjust. Confirm this rider is included.

Cancelling term right before it expires without a plan. If you still need coverage at age 55, look at extension options or new policies before letting the original lapse.

Frequently Asked Questions

What if I want coverage forever? Whole life is one option. Another option: 30-year term + a final expense whole life policy at retirement. The combo often costs less than whole life alone over a lifetime.

Can I convert my term policy to whole life later? Most term policies have a conversion rider that lets you convert to permanent coverage without new medical underwriting. The conversion has to happen by a certain age and within the policy term. Confirm this is in your policy.

Is whole life "an investment"? Not really. It's life insurance with a tax-deferred savings component. The savings component grows slower than most other investment options. Don't buy whole life expecting strong investment returns; buy it for permanent insurance with a savings side benefit.

What about a "Roth IRA versus whole life" comparison? Roth IRA wins on flexibility, growth potential, and lower cost. Whole life wins only on (a) permanent insurance bundled in and (b) creditor protection in some states. For pure savings, max your Roth before considering whole life.

Should I buy whole life on my kids? Usually no. Marketed as "lock in low rates while they're young," but the math rarely works. Better to fund a 529 or custodial Roth for them and skip the small whole life policy.

Can I have both term and whole? Yes — and for some Atlanta families it's the right answer. Big term policy for income replacement during working years, plus a small whole life for final expenses or estate planning.

The Bottom Line

For most working Atlanta families, term life wins. Cheaper. Simpler. Right-sized for the actual need. The savings invested elsewhere usually outperform whole life's cash value over the same period.

For a smaller group with specific situations (estate tax, special needs, business buy-sell, final expense), whole life or a hybrid is the right tool.

The mistake I see most: families with a clear term-life need getting sold a small whole life policy because the agent's commission is bigger. They end up under-protected and over-paying.

If you've been pitched whole life and aren't sure if it's right for your situation, book a 15-minute call with me. I'll run the math both ways, show you what the difference actually looks like over 20 years, and give you a straight answer. Costs you nothing — I'm an independent broker paid by carriers, not by you, and I make the same whether you buy term or whole.

Want to keep reading? Start with How Much Life Insurance Do You Actually Need in 2026? (run that calculation first), or Health Insurance for the Self-Employed (because most self-employed Atlantans need both).

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not financial, tax, or legal advice. Life insurance underwriting, premium rates, and IRS rules change