Atlanta Homeowners Insurance: A 2026 Buyer's Guide

Author: Justin Bishop · May 11, 2026 · 9 min read

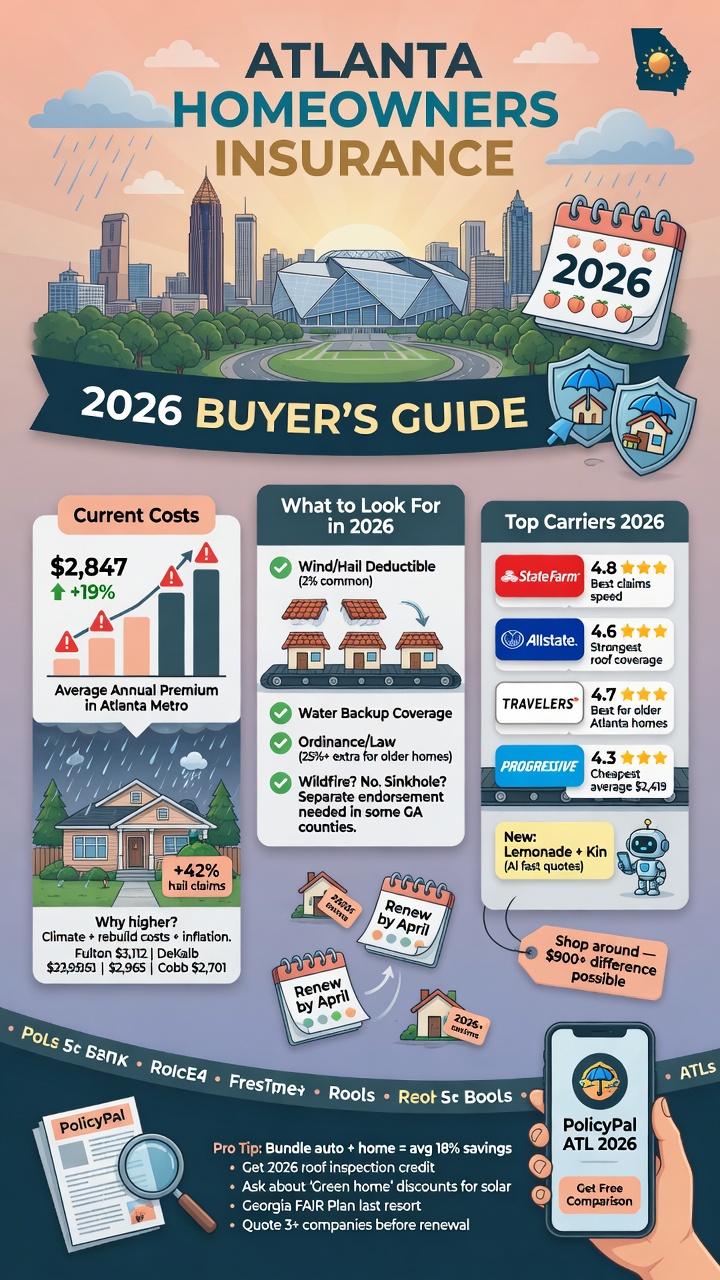

If you bought a home in the Atlanta metro recently — or just got a renewal notice that made your stomach drop — you've already learned that Georgia homeowners insurance isn't cheap. The average Atlanta homeowner now pays $2,000-3,500 per year, well above the national average. Renewal increases of 15-25% have been common for the past three years.

The bigger problem isn't just the cost. It's that most Atlanta homeowners don't fully understand what their policy actually covers, what it doesn't, and what specific coverages they should be adding for the storm and tree-fall risks unique to the Southeast.

This is the plain-English buyer's guide. What homeowners insurance actually covers, what it doesn't, how much coverage you need, the major Georgia carriers, what drives the price in Atlanta specifically, and the specific moves that can knock $300-800/year off your premium.

I'm Justin Bishop, an independent broker in Atlanta. I write homeowners coverage across multiple carriers. Here's the practical breakdown.

The 30-Second Version

Standard HO-3 policy covers 6 things: the structure, other structures, personal property, loss of use, personal liability, and medical payments to others.

It does NOT cover: flood, earthquake, sinkhole, sewer backup, normal wear-and-tear, mold (mostly), or termite damage. Some of these need separate riders or policies.

The cost drivers in Atlanta: wind/hail risk, pine tree exposure, replacement cost of the dwelling, your credit score, your claims history, and the carrier's recent loss experience in your ZIP code.

The fastest ways to save: bundle auto + home, raise your deductible, add storm-resistant features, fix small issues before renewal, and shop carriers every 2-3 years.

The single most important question: is your dwelling coverage based on rebuild cost (right) or market value / mortgage balance (wrong)? This is where most underinsurance happens.

What Atlanta Homeowners Insurance Actually Covers

A standard HO-3 policy (the most common type in Georgia) covers six core areas:

Coverage A — Dwelling: the physical structure of your home. Walls, roof, foundation, attached garage, built-in fixtures.

Coverage B — Other Structures: detached structures on your property — detached garage, shed, fence, pool cabana, gazebo. Typically 10% of Coverage A.

Coverage C — Personal Property: everything inside your home that isn't physically attached. Furniture, electronics, clothes, kitchenware. Typically 50-70% of Coverage A.

Coverage D — Loss of Use: if your home is uninhabitable from a covered loss, this pays for alternative housing, food, and additional expenses. Typically 20-30% of Coverage A.

Coverage E — Personal Liability: if someone gets hurt on your property (or you damage someone else's property), this covers legal defense and judgments up to your policy limit. Standard limits: $100K-500K; recommended for Atlanta: $300K minimum.

Coverage F — Medical Payments to Others: small, no-fault medical bills (typically up to $5K) if someone is injured on your property. Doesn't require a liability claim.

That's the policy structure. The dollar amounts of each coverage are set when you bind the policy.

What Homeowners Insurance Does NOT Cover

This is where most Atlanta homeowners get caught off guard. Standard HO-3 specifically excludes:

Flood damage — separate NFIP policy or private flood policy required. Even in inland Atlanta, river/creek flooding is a real risk in specific ZIP codes.

Earthquake damage — Georgia earthquakes are rare but possible. Separate rider available.

Sinkhole damage — limited coverage in standard policy; rider available for full coverage.

Sewer/water backup — drain or sump pump backup damage. Standard policy excludes; add a rider ($30-80/year) for coverage.

Normal wear and tear — your aging roof, deferred maintenance, gradual deterioration.

Termite/pest damage — separate pest contracts cover this.

Mold damage (mostly) — limited coverage in most HO-3 policies; some carriers offer limited mold riders.

Acts of war, nuclear events, government action — never covered.

Intentional damage by the policyholder — never covered.

The single biggest gap most Atlanta homeowners miss: flood insurance. Standard policies don't cover it, and many Atlanta neighborhoods have hidden flood risk that doesn't show up on basic flood maps.

How Much Coverage You Actually Need

The wrong question is "how much can I afford?" The right question is "what would it cost to fully rebuild my home today?"

For Atlanta-area homes in 2026, rebuild costs typically run:

Standard construction (vinyl siding, asphalt shingle): $140-180 per square foot

Mid-grade construction (brick veneer, architectural shingles): $180-220 per square foot

Higher-end construction (brick, stone, slate, custom features): $220-300+ per square foot

For a 2,200 sq ft Atlanta home of mid-grade construction, that's roughly $400,000-485,000 in dwelling coverage — which is often dramatically higher than the home's market value or your mortgage balance.

This is the single most important number on your policy. If you're under-covered on Coverage A:

Most policies have a coinsurance clause that penalizes underinsurance — you collect a proportional payout, not the full claim

A total loss (fire, tornado) leaves you tens or hundreds of thousands of dollars short

This is the #1 source of catastrophic homeowner financial loss after a major event

For personal property (Coverage C), most Atlanta households need $150,000-300,000 in coverage. Take a 5-minute mental walk through your house — the value adds up faster than you think.

The Major Georgia Carriers

The Atlanta market is competitive but not all carriers are the same. The largest carriers writing homeowners in Georgia 2026 include:

State Farm — largest market share in Georgia. Strong service, captive agent model. Solid baseline pricing.

Allstate — second-largest market share. Aggressive new-customer discounting, sometimes rate increases at renewal.

Travelers — strong on higher-value homes. Good for homes in newer developments.

Farmers — competitive in middle Georgia and Atlanta suburbs. Frequent bundling discounts.

USAA — military families and veterans only. Generally the lowest rates available in this category.

Liberty Mutual — competitive in many Atlanta ZIP codes. Strong online tools.

Nationwide — solid carrier, less aggressive on pricing.

Progressive — growing market share in Georgia homeowners. Often paired with auto bundling.

Georgia Underwriting Association (GUA) — Georgia's "last resort" market for homeowners who can't get coverage elsewhere (often after multiple claims or high-risk properties). More expensive, narrower coverage.

The right carrier varies by ZIP code, home characteristics, and your claims/credit profile. No single carrier is "best" for everyone in Atlanta. Shopping across 5-7 carriers is the only way to know.

What Actually Drives the Price in Atlanta

Georgia homeowners premiums have grown faster than national averages for several reasons:

Wind and hail losses — Georgia averages 30-40 tornado days per year and significant hail losses. Carriers price wind/hail aggressively.

Pine tree exposure — mature pine trees on Atlanta properties are a major covered-loss driver. Falling trees in storms cause millions in damage annually.

Replacement cost inflation — construction materials and labor have outpaced general inflation 2x for the past five years.

Carrier loss experience in your ZIP code — if your area has had multiple major storms in recent years, premiums in that ZIP rise faster.

Your credit-based insurance score — Georgia allows credit-based pricing. Excellent credit can save 20-40% vs poor credit on the same home.

Your prior claims history — every claim in the past 5 years raises premiums. Two claims in 3 years can make some carriers refuse to renew.

The age of your roof and other major systems — roofs over 15 years old, HVAC over 20 years, plumbing over 30 years all push premiums up.

Dog breed — yes, this is real. Many carriers exclude or surcharge for specific breeds (pit bulls, Rottweilers, German shepherds, etc.).

For specific 2026 pricing by home size and Atlanta ZIP, see How Much Does Homeowners Insurance Cost in Atlanta in 2026?

Atlanta-Specific Coverages You Should Consider Adding

Beyond the standard HO-3, these riders are worth considering for Atlanta:

Replacement cost endorsement on personal property — without this, contents are paid at actual cash value (depreciated). The endorsement pays what it costs to replace today. Typically adds $40-80/year and is almost always worth it.

Sewer/water backup rider — covers backup from drains or sump pump failure. Common Atlanta issue with old sewer lines and heavy rains. $30-80/year.

Service line coverage — covers buried water, sewer, gas, and electrical service lines on your property. Atlanta soil and pine trees damage these regularly. $30-50/year.

Equipment breakdown coverage — covers HVAC, water heater, kitchen appliances when they fail from internal mechanical issues. $30-60/year.

Ordinance or law coverage — covers the additional cost to rebuild to current building code after a covered loss. Atlanta-area code changes have made this increasingly important. Sometimes built into HO-3; verify.

Higher liability limits — go to $500K or $1M umbrella for very modest cost. Swimming pools, dogs, teen drivers all elevate liability exposure.

Flood insurance — separate NFIP or private flood policy. If you have a basement or live near any water (creek, river, retention pond), you need this. Many flooded homes in Atlanta were "not in a flood zone."

For the deep-dive on adding $1M-5M of extra liability protection above standard home limits, see What Is an Umbrella Policy?

How to Lower Your Atlanta Homeowners Premium

Real moves that work:

Bundle auto and home — typical savings 5-25% across both policies. Almost always the easiest win.

For the matching auto coverage decision, see Should I Get Liability or Full Coverage for My Car in Atlanta?

Raise your deductible — going from $1,000 to $2,500 typically saves 10-20% in premium. Worth it if you can comfortably cover the higher deductible from cash savings.

Add storm-resistant features — impact-resistant shingles, hurricane shutters, wind mitigation can earn discounts of 5-15% with some carriers.

Improve your roof — newer roofs (under 10 years) often get a discount. If your roof is over 15 years old, replacing it before renewal can pay back in premium savings within 2-3 years on its own.

Address claims-history triggers — small claims under $1,500-2,000 often aren't worth filing (premium increase exceeds claim payout over 3 years).

Maintain good credit — Georgia allows credit-based insurance scoring. Credit improvement directly reduces premium.

Shop every 2-3 years — carrier pricing changes; your renewal premium is rarely the most competitive rate available.

Add a security system — central station monitored systems often earn 5-10% discount.

Loss-free discounts — many carriers reward 3+ years claim-free with 5-10% premium reduction.

Common Atlanta Homeowner Insurance Mistakes

Patterns I see weekly:

Insuring to mortgage balance instead of rebuild cost. Catastrophic underinsurance. Always insure to current rebuild cost, not what you owe.

Skipping flood insurance because "I'm not in a flood zone." Most flooded homes weren't in mapped flood zones.

Filing every small claim. A $1,200 claim raises your premium $150/year for 3-5 years — that's $750+ in premium increases to collect $1,200. Not always worth it.

Accepting actual cash value on personal property. Replacement cost is usually worth the $40-80/year upgrade.

Auto-renewing every year without shopping. Carrier pricing is competitive but only at new-customer acquisition. Loyalty doesn't pay in homeowners insurance.

Not raising liability limits. $100K liability on a $400K home is dangerously low. $300K minimum, $500K-1M with umbrella is reasonable for Atlanta.

Forgetting the dog breed exclusion. Some carriers will deny a claim involving a specific breed. Always disclose dog breeds at binding.

Letting a roof age past 15-20 years. Many carriers won't renew at older roof ages. Replace before renewal forces it.

Choosing the cheapest carrier without checking claims service. A 15% premium savings is worthless if claims take 6 months to settle.

Frequently Asked Questions

Is homeowners insurance required by law in Georgia? No — Georgia law doesn't require homeowners insurance. But your mortgage lender will require it as a condition of the loan. If you own outright, technically optional, but going without is financial suicide.

What's the difference between HO-3 and HO-5? HO-3 (standard) is open-peril for dwelling, named-peril for contents. HO-5 (broader) is open-peril for both. HO-5 costs roughly 10-15% more but offers significantly broader coverage on personal property. Worth it for homes with high-value contents.

Do I need flood insurance if I'm not in a flood zone? Probably yes. Roughly 20% of all flood claims happen outside designated flood zones. Atlanta has multiple ZIP codes with hidden flood exposure from creeks, storm drains, and aging infrastructure.

How fast can I switch carriers? You can switch any time — coverage transitions on the effective date you specify. There's no penalty for canceling mid-policy; you'll get a prorated refund. The trick is timing the new policy's effective date to match your old policy's cancellation date so there's no gap.

Will my insurance pay for tree removal after a storm? If the tree fell on a covered structure (house, detached garage, etc.), tree removal is usually covered up to a sublimit ($500-1,500). If the tree just fell in your yard without hitting anything, removal usually isn't covered.

Does my homeowners cover items I take outside the home (like a stolen laptop from my car)? Yes, but at reduced coverage limits. Personal property coverage extends to your possessions worldwide, but theft from a vehicle often has a sublimit. Read your policy carefully.

What does a "wind/hail deductible" mean? Many Atlanta-area carriers now apply a separate, percentage-based deductible for wind and hail losses (typically 1-5% of dwelling coverage). On a $400K home, that's $4,000-20,000 out-of-pocket on a hail claim before insurance pays. Critical to know before a claim happens.

The Bottom Line

Atlanta homeowners insurance in 2026 is more expensive than most states for real reasons — storm exposure, replacement cost inflation, and carrier loss experience. You can't make the market cheaper, but you can:

Insure to actual rebuild cost (not mortgage balance)

Add the riders that fill real gaps (flood, sewer backup, replacement cost on contents)

Raise your deductible to lower premium if you can absorb the higher out-of-pocket

Shop across multiple carriers every 2-3 years

Work with an independent broker who can compare carriers in one shot

If you're staring at a renewal notice that doesn't make sense or you just bought a home and don't know where to start, book a 15-minute call with me. I'll run quotes across the major Georgia carriers, identify gaps in your current coverage, and tell you exactly what's worth paying for and what to skip. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Check out coverage cost specifics in How Much Does Homeowners Insurance Cost in Atlanta in 2026? (next post in this cluster, publishing May 16), or Renters Insurance in Atlanta (May 20). For cross-cluster context, see Why Is Health Insurance So Expensive in Georgia? — same structural cost dynamics apply to home insurance.

For retirees in Atlanta also navigating Medicare, see What's the Difference Between Medicare Advantage and Medigap?

Bundle/Savings

Bundle savings between home and auto are real. See How Much Does Car Insurance Cost in Atlanta in 2026? for typical auto pricing in 2026

Bundling auto with homeowners is one of the 4 actionable ways to lower an expensive Atlanta auto premium. See Why Is Car Insurance So Expensive in Atlanta? for the rest

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal, tax, or HR advice. COBRA and Georgia Mini-COBRA rules, notice requirements, and penalties change.