How Much Does Homeowners Insurance Cost in Atlanta 2026?

Author: Justin Bishop · May 16, 2026 · 7 min read

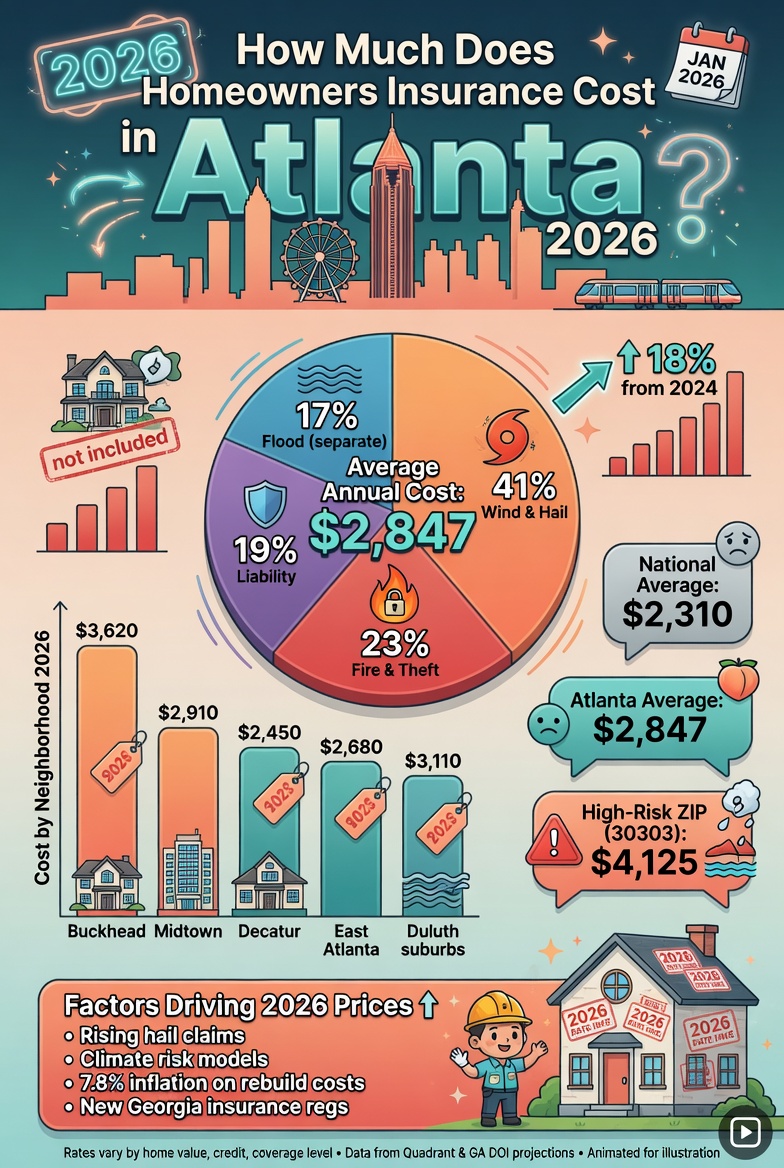

If you just got an Atlanta homeowners insurance renewal that made your jaw hit the floor, here's the context: the average Atlanta homeowner now pays $2,000 to $3,500 per year for typical coverage. Premiums have climbed 15-25% per year for three straight years, and 2026 is on pace for another 8-15% increase.

The cost isn't random. There are very specific factors that drive Atlanta home insurance pricing — ZIP code, roof age, construction type, claims history, credit, and the carrier's recent loss experience in your area. Knowing those factors is how you actually lower your premium without giving up coverage you need.

This post breaks down the real 2026 Atlanta homeowners insurance costs by home profile, what drives the pricing, the major carriers, and the specific moves that knock $300-800/year off your premium.

I'm Justin Bishop, an independent broker in Atlanta. I quote and place homeowners insurance across multiple carriers weekly. Here's the honest breakdown.

The 30-Second Version

Atlanta metro average for typical coverage: $2,000-3,500/year

Cost drivers: ZIP code, dwelling replacement cost, roof age, construction type, your claims history, credit, and wind/hail deductible

Biggest single factor: dwelling coverage amount. Insuring to rebuild cost (not market value) is non-negotiable.

Single fastest savings: bundle home + auto (5-25%), raise deductible ($1,000 → $2,500 saves 10-20%), shop carriers every 2-3 years

Renewal expectation for 2026: 8-15% premium increase from 2025. Plan for it.

The full coverage buyer's guide is here: Atlanta Homeowners Insurance: A 2026 Buyer's Guide. Read it BEFORE comparing quotes — pricing is meaningless without knowing what coverage you actually need.

Real 2026 Atlanta Homeowners Insurance Costs

Here are typical 2026 annual premiums for the Atlanta metro by home and owner profile:

Smaller home (under 2,000 sq ft), basic HO-3 coverage:

$200,000 dwelling coverage, $1,000 deductible: $1,500-2,200/year

$250,000 dwelling, $2,500 deductible: $1,400-2,000/year

$300,000 dwelling, $1,000 deductible: $1,800-2,600/year

Mid-size home (2,000-3,000 sq ft), HO-3 coverage:

$400,000 dwelling, $2,500 deductible: $2,200-3,200/year

$500,000 dwelling, $2,500 deductible: $2,700-3,800/year

$500,000 dwelling, $5,000 deductible: $2,300-3,300/year

Larger home (3,000+ sq ft), HO-3 or HO-5 coverage:

$600,000 dwelling, $2,500 deductible: $3,000-4,200/year

$750,000 dwelling, HO-5, $5,000 deductible: $3,500-5,000/year

$1,000,000+ dwelling, HO-5, premium carrier: $4,500-7,500+/year

Adjustments to apply to the ranges above:

Newer home (built after 2018): subtract 15-25%

Brick construction: subtract 10-15%

Newer roof (under 10 years): subtract 10-20%

Older home (built before 1975): add 15-30%

Poor credit-based insurance score: add 25-40%

One claim in last 3 years: add 15-25%

Two claims in last 5 years: add 30-50% (some carriers will non-renew)

What Actually Drives the Price in Atlanta

Several Atlanta-specific factors push premiums higher than national averages:

Wind and hail risk. Georgia averages 30-40 tornado days per year. Hailstorms cause millions in roof and siding damage annually. Carriers price wind/hail aggressively.

Mature pine trees. Atlanta's tree canopy is beautiful — and a major claim driver. Falling trees in storms cause roof damage, siding damage, and structural claims.

Replacement cost inflation. Construction materials and labor have outpaced general inflation 2x for the past five years. A 2,200 sq ft Atlanta home that cost $300K to rebuild in 2020 now costs $400-485K.

Carrier loss experience by ZIP code. If your specific ZIP has had multiple major storms in recent years, premiums rise faster there. Loss experience is the carrier's biggest pricing input.

Your credit-based insurance score. Georgia allows credit-based pricing. Excellent credit can save 20-40% versus poor credit on the exact same home.

Roof age. Roofs over 15 years old often face premium surcharges or non-renewal. Roofs over 20 years may be uninsurable with standard carriers.

Prior claims history. Every claim in the past 5 years raises premiums. Two claims in 3 years can trigger non-renewal.

Distance from fire hydrant + fire station. Rural and exurban Atlanta-area homes with poor fire protection pay more.

Pool, trampoline, or specific dog breeds. Liability surcharges or outright exclusions apply with most carriers.

Cost by Atlanta-Area ZIP Code

Where you live in the Atlanta metro materially affects your premium. Rough relative pricing on identical homes:

Atlanta city ZIPs (30309, 30312, 30318, 30309, 30307): highest premiums — older housing stock, urban claim density

East Atlanta / Decatur (30030, 30032, 30034): mid-to-high — older homes, mature trees

Marietta / Cobb (30062, 30064, 30068): mid — newer housing mix

Sandy Springs / North Fulton (30328, 30342, 30350): mid — varied housing stock

Alpharetta / Roswell (30022, 30075, 30009): mid-low — newer housing, lower claim density

Johns Creek / Suwanee (30097, 30024): lower — newer construction, strong fire protection

East Cobb / Powder Springs: mid — mixed housing stock

Outer exurbs (Forsyth, Cherokee, Henry): lower premium ranges generally, but may have fire protection class issues

The same $400,000 home can have a $1,000-1,800/year premium difference depending on which Atlanta-area ZIP it's in.

The Wind/Hail Deductible (The Hidden Cost)

Many Atlanta-area carriers now apply a separate percentage-based deductible for wind and hail losses — typically 1-5% of your dwelling coverage. This is in addition to your standard "all other perils" deductible.

What this looks like in practice:

Dwelling coverage: $400,000

Standard deductible: $2,500 (applies to most claim types)

Wind/hail deductible: 2% of dwelling = $8,000 (applies to hail, tornado, wind damage)

So if a hailstorm damages your roof, you pay the first $8,000 out of pocket before insurance pays — not the $2,500 you'd expect.

This is the #1 surprise for Atlanta homeowners filing their first wind/hail claim. Always know your wind/hail deductible percentage and dollar amount before you need to file.

Some carriers offer a flat-dollar wind/hail deductible (e.g., $2,500 instead of 2%) for a small premium increase. Worth comparing.

How Roof Age Changes Your Premium

Atlanta carriers scrutinize roof age more than almost any other factor right now:

Roof 0-10 years old: baseline pricing (often discount available)

Roof 10-15 years old: standard pricing, some carriers will still write

Roof 15-20 years old: premium surcharge, fewer carriers willing

Roof 20+ years old: non-renewal risk, very limited carrier options

Roof 25+ years old: likely uninsurable through standard market (GUA only)

Why this matters: if your roof is approaching 15 years and you're getting close to renewal, replacing it before the next renewal often pays back in premium savings within 2-3 years AND keeps you eligible with standard carriers.

For Atlanta homeowners with older roofs, the math often supports proactive replacement — both for insurance pricing and to avoid a potential mid-year non-renewal.

The Major Atlanta Homeowners Carriers in 2026

Carriers actively writing homeowners insurance in Atlanta for 2026:

State Farm — largest market share in Georgia. Strong service, captive agent model. Competitive on standard profiles.

Allstate — second-largest market share. Aggressive new-customer discounts; renewals can climb.

Travelers — strong for higher-value homes and newer construction.

Farmers — competitive in middle Georgia and Atlanta suburbs. Strong bundling.

USAA — military and veterans only. Generally lowest rates in this category.

Liberty Mutual — competitive in many ZIP codes.

Nationwide — solid baseline coverage.

Progressive — growing market share, often paired with auto bundles.

Cincinnati Insurance — strong claims service, premium pricing.

Auto-Owners — competitive for newer suburbs.

Georgia Underwriting Association (GUA) — last-resort market for homes that can't get standard coverage. Higher premiums, narrower coverage.

No single carrier is "cheapest" for everyone. Your specific combination of ZIP, home age, roof age, claims history, and credit determines who wins. Shopping across 5-7 carriers is the only way to know.

How to Actually Lower Your Atlanta Homeowners Premium

Real moves that work:

Bundle home and auto. Typical savings 5-25% across both policies. Almost always the easiest win.

Raise your standard deductible. Going from $1,000 to $2,500 saves 10-20% in premium. Going to $5,000 saves more if you can absorb it.

Choose a flat-dollar wind/hail deductible instead of percentage-based, if available. May cost slightly more in premium but caps your storm exposure.

Replace an aging roof. Roofs over 15 years old often pay back in 2-3 years of premium savings.

Add storm-resistant features. Impact-resistant shingles, hurricane shutters, wind mitigation upgrades can earn 5-15% discounts.

Maintain or improve your credit. Georgia allows credit-based pricing. Credit improvement directly reduces premium.

Add a monitored security system. 5-10% discount with most carriers.

Don't file claims under $1,500-2,000. Premium increases from a claim usually exceed the claim payout over 3-5 years.

Maintain claim-free for 3+ years. Many carriers reward loss-free history with 5-10% discount.

Shop carriers every 2-3 years. Loyalty doesn't pay; renewal pricing is rarely the most competitive available.

Review and right-size your liability limit. Going from $100K to $300K liability typically adds only $50-100/year — cheap protection.

Common Atlanta Homeowner Insurance Mistakes

Patterns I see weekly:

Insuring to mortgage balance instead of rebuild cost. Catastrophic underinsurance. Always insure to current rebuild cost ($140-300/sq ft in Atlanta 2026), not what you owe.

Not knowing the wind/hail deductible. Surprising number of homeowners file a hail claim, then discover they owe $8K-15K before insurance pays anything.

Picking the lowest-premium carrier without checking complaint ratios. Cheap carriers often have slow or contested claims service.

Filing every small claim. A $1,500 claim raises premium $200-400/year for 3-5 years. You collect $1,500, pay back $750-1,500+ in surcharges.

Letting an aging roof linger. A 17-year-old roof costs more in premium increases than replacing it would have cost.

Accepting actual cash value on personal property. Replacement cost is usually worth the small upcharge.

Ignoring flood insurance. Standard policies exclude flood. ~20% of flood claims happen outside designated zones. If you have a basement or live near any water, you need separate flood coverage.

Auto-renewing without shopping. Carrier renewal pricing rarely beats new-customer pricing elsewhere.

Forgetting dog breed disclosures. Some carriers exclude or surcharge specific breeds. Failing to disclose can void claims.

Frequently Asked Questions

Why did my premium go up at renewal even though nothing changed? Multiple factors: replacement cost inflation, your carrier's loss experience in your ZIP, statewide rate filings, and natural premium pressure. 8-15% renewal increases are common in 2026 even with no changes on your end.

Can I switch carriers mid-year? Yes. Coverage transitions on the effective date you specify. No penalty for canceling mid-policy — you get a prorated refund. The trick is timing the new policy's effective date to match the old one's cancellation date.

How much homeowners insurance do I really need? Cover the rebuild cost of your home (not market value, not mortgage balance). For an Atlanta 2,200 sq ft home in 2026, rebuild cost is typically $400-485K. Personal property typically 50-70% of dwelling.

What does HO-3 vs HO-5 mean? HO-3 (standard) is open-peril for the dwelling, named-peril for contents. HO-5 (broader) is open-peril for both. HO-5 costs 10-15% more but offers significantly broader coverage on personal property.

Will my carrier drop me after one claim? Usually not for a single claim under $5K. Two claims in 3 years can trigger non-renewal with most carriers. Three claims puts you in the surplus / non-standard market.

Is flood insurance required for my Atlanta home? Only if you have a federally-backed mortgage AND your home is in a designated flood zone. But flood damage is not covered by homeowners insurance — separate NFIP or private flood policy required. Recommended even outside designated flood zones for many Atlanta homes.

What's the cheapest legal homeowners insurance I can get? Georgia doesn't legally require homeowners insurance. But your mortgage lender does. The cheapest mortgage-acceptable coverage is typically a basic HO-3 policy at the highest deductible the lender allows.

The Bottom Line

Atlanta homeowners insurance in 2026 is more expensive than most metros for real, structural reasons — wind/hail risk, mature pine tree exposure, replacement cost inflation, and carrier loss experience. You can't fix the market, but you can shop it.

The single most important fix: insure to actual rebuild cost. Underinsurance is the catastrophic mistake. Once that's right, the rest is about matching your specific ZIP, home, and risk profile to the carrier that prices best for that combination.

If your renewal just came in or you're shopping for a new policy, book a 15-minute call with me. I'll run quotes across the major Atlanta carriers in one shot, identify gaps in your current coverage, and tell you which carrier wins for your specific situation. Costs you nothing — I'm paid by carriers, not by you.

Want to keep reading? Start with the Atlanta Homeowners Insurance: A 2026 Buyer's Guide (what coverage you actually need), or check How Much Does Car Insurance Cost in Atlanta in 2026? (bundle partner — typical savings 5-25%).

Coverages to Consider Adding

For homeowners with significant equity, umbrella is the cheapest way to add $1M-5M of additional liability protection. See What Is an Umbrella Policy?

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn — and yes, he answers his own texts.

This post is general education, not legal, tax, or financial advice. Homeowners insurance premiums, deductible structures, carrier underwriting rules, and Georgia rate filings change.