ACA Special Enrollment Periods: When Georgians Can Sign Up Off-Cycle

Author: Justin Bishop · May 1, 2026 · 7 min read

You don't usually call an insurance broker because you're bored. You call because something just changed — you lost your job, got married, had a baby, moved across town, your spouse aged off your plan, you turned 26 and just got kicked off your parents' insurance. And now you need health insurance, and Open Enrollment ended four months ago.

The good news is the system has a release valve for this exact situation. It's called a Special Enrollment Period (SEP), and it lets you enroll in a Georgia Access marketplace plan outside the November-January Open Enrollment window — but only if your situation qualifies, and only if you act inside a specific time window.

I'm Justin Bishop, an independent broker in Atlanta. I write SEPs for clients almost every week of the year. Here's what triggers a SEP, how the 60-day clock works, what documentation you'll need, and the specific traps that catch people who don't know the rules.

The 30-Second Version

A Special Enrollment Period (SEP) lets you sign up for a Georgia Access marketplace health plan outside Open Enrollment.

You qualify if a "Qualifying Life Event" (QLE) happens to you — losing job-based coverage, marriage, divorce, having a baby, aging off a parent's plan, moving, becoming a citizen, etc.

You have 60 days from the QLE to enroll. Miss it and you wait until next Open Enrollment (Nov 1 - Jan 15).

You'll need to prove the QLE — typically with documentation like a termination letter, marriage certificate, lease, or birth certificate.

A licensed broker can help you enroll faster than going alone, and the help is free.

That's the entire framework. The rest of this post is the detail.

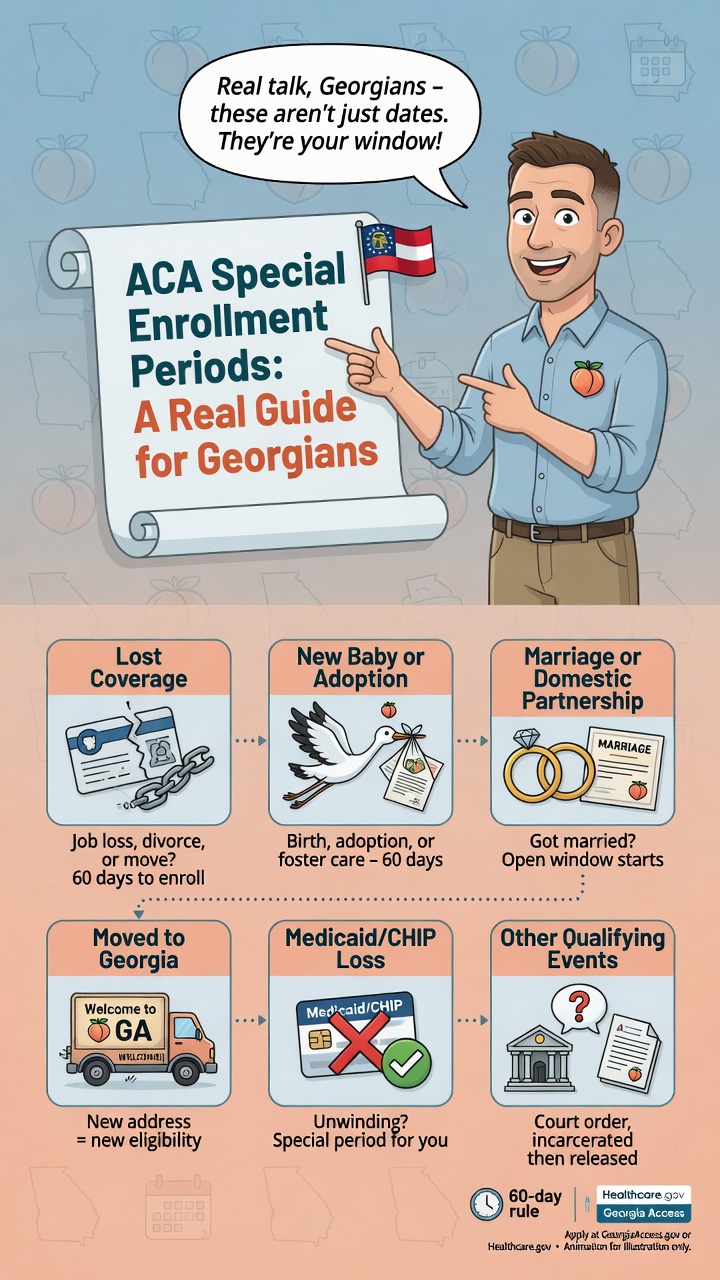

The 11 Qualifying Life Events That Open a SEP

Not every life change qualifies. Here's the full list of events that trigger a Special Enrollment Period under ACA rules in Georgia:

1. Loss of qualifying health coverage

The big one. If you had health insurance and you lost it, you almost certainly qualify. This includes:

Losing a job that provided coverage (whether you quit or were laid off)

Your employer dropped health coverage

Job loss is the most common SEP trigger — see I Just Lost My Job in Atlanta

Aging off a parent's plan at 26

COBRA running out (the natural end of your 18-month window — note: voluntarily dropping COBRA does NOT count)

Losing Medicaid or CHIP eligibility

A spouse losing job coverage that you were dependent on

Aging out of a student plan

A divorce or legal separation that drops you from a spouse's coverage

Trap to watch: quitting your COBRA voluntarily before its 18 months expire does NOT trigger a SEP. The SEP triggers when COBRA ends naturally — not when you choose to drop it.

2. Marriage

Getting married opens a SEP for both spouses. You can enroll in a new joint plan or one spouse can join the other's existing plan. You'll need a marriage certificate.

3. Divorce or legal separation

If the divorce results in loss of coverage (e.g., you were on your spouse's plan), it's a SEP. Divorce alone without coverage loss doesn't always qualify — depends on the specifics.

4. Birth, adoption, or placement of a child for adoption/foster care

A new dependent triggers a SEP. Coverage can typically be backdated to the date of birth or placement, which matters for newborn medical bills.

5. Death of a covered family member

If a death results in loss of coverage for surviving family members, it triggers a SEP.

6. Permanent move to a new ZIP code where different plans are available

Moves typically count if your new ZIP has different marketplace plans available than your old one. Most cross-county or cross-state moves qualify; same-neighborhood moves usually don't.

You also generally need to have had qualifying coverage for at least one of the 60 days before the move (preventing people from gaming the system by moving solely to enroll mid-year).

7. Becoming a U.S. citizen or lawful permanent resident

Once your status changes, you have a SEP to enroll.

8. Release from incarceration

Coverage during incarceration is treated separately from regular health insurance; release triggers a SEP.

9. Change in income that newly qualifies you for premium tax credits

If your income drops or rises into the subsidy-eligible range (currently 100-400% of FPL in 2026, since the enhanced subsidies expired), it can trigger a SEP — but rules here are stricter and require careful documentation.

10. Plan errors or marketplace mistakes

If a Georgia Access enrollment got fouled up by an error on the marketplace's end, the marketplace can grant you a SEP to fix it.

11. Other "complex situations"

A catch-all category for unusual situations — domestic violence/abuse cases, natural disasters in your area, technical issues on the marketplace site that prevented timely enrollment. These typically require a phone call to Georgia Access or a broker to walk through.

For the broader Georgia marketplace overview, see Georgia Health Insurance Marketplace: A 2026 Guide

The 60-Day Clock — Most Important Rule

For most QLEs, you have 60 days from the qualifying event to enroll. That clock starts:

On the day the event happens for marriage, birth, adoption, divorce, etc.

The day coverage ends for loss-of-coverage events (not the day you found out you'd be losing it)

The day of the move for relocation events

Some QLEs (notably loss of coverage and birth/adoption) actually give you a 60-day window on either side — meaning you can enroll up to 60 days before OR after the event. This is helpful if you know coverage is ending soon and want to line up the new plan to avoid a gap.

Miss the 60 days and you wait until Open Enrollment (November 1 - January 15 each year), which can mean going uninsured for months. There are very few extensions to this rule. Set a calendar reminder the day the event happens.

Documentation You'll Need

Georgia Access (and your broker) will ask for proof of the QLE. Typical documentation by event type:

EventAcceptable proofLost job coverageTermination letter, COBRA notice, letter from former employer's HRMarriageMarriage certificate (state-issued)DivorceDivorce decreeBirthBirth certificate, hospital discharge papersAdoptionAdoption decree, foster placement letterMoveUtility bill, lease, mortgage, voter registration with new addressAged off parent's planLetter from parent's insurer, plus your date of birthCOBRA expirationNotice of COBRA termination from former employerCitizenshipNaturalization certificate, green cardIncome changeTax returns, pay stubs, profit/loss statements

Pro tip: gather documentation BEFORE you start the enrollment. Trying to upload documents while a Georgia Access session times out is one of the most frustrating user experiences in healthcare. Have your files ready.

How to Actually Enroll During a SEP

Three paths, in order of speed:

Through a licensed Georgia broker (free). A broker has direct access to the Georgia Access agent portal, can verify your QLE eligibility in 5 minutes, runs subsidy math against your projected MAGI, and submits the enrollment with proper documentation. This is the fastest and least error-prone path. The broker is paid by the carrier — it's free to you.

Directly through Georgia Access (georgiaaccess.gov). Free, public. Slower because you're navigating the system on your own; the consumer interface is improving but still has rough edges. Make sure your QLE eligibility is established before starting the enrollment, or you'll hit dead ends.

Through a Web Broker certified by Georgia Access. Several web brokers (HealthSherpa, Stride, INSXCloud) are approved to enroll Georgia residents through Georgia Access. Decent middle-ground option for confident shoppers.

If you've never enrolled in marketplace coverage before, a broker is genuinely faster. Even people who've enrolled before benefit from a 15-minute call with someone who can run the math against the cliff (which is back in 2026 — see the subsidy cliff guide).

Common Mistakes I See

1. Waiting too long. The 60-day clock runs whether you remember it or not. Several clients have missed it because they assumed they'd "get to it next week" and then it was 70 days later.

2. Voluntarily dropping COBRA early. Doesn't qualify as a QLE. Wait for COBRA to end on its own schedule (or run the math — sometimes COBRA + waiting until Open Enrollment is cheaper than dropping early and going uninsured).

3. Assuming a same-neighborhood move qualifies. Moving from Buckhead to Midtown probably doesn't count if both ZIPs have the same marketplace plans available. Cross-county or cross-state moves are safer.

4. Not getting documentation in advance. I've watched people lose enrollment slots because they couldn't find their old termination letter at 11pm the night before the deadline. Store these documents somewhere you can find them in 60 seconds.

5. Not updating projected income mid-year. If your QLE is income-related (you started self-employment, your spouse lost work, etc.), you need to project realistically — too low and you owe back subsidies at tax time; too high and you don't get help you qualify for.

6. Missing the enhanced 60-day pre-event window. For loss-of-coverage events, you can usually enroll 60 days before coverage ends. If you know coverage is ending in 30 days, start enrollment now to avoid a gap. (See the Atlanta health insurance buyer's guide for the full timing breakdown.)

What If You Don't Qualify for a SEP?

You're not totally stuck. Three options if you've missed the SEP window or don't qualify:

1. Short-term medical insurance. Cheaper monthly premium, but it's NOT ACA-compliant. Doesn't cover pre-existing conditions, has annual benefit caps, can be canceled by the carrier. Useful as a 1-3 month bridge between coverage periods; not a long-term solution.

2. Health share ministries. Cost-sharing arrangements (usually faith-based) that aren't insurance but pay for many medical needs. Works for healthy people without major pre-existing conditions; read the membership guide carefully.

3. Wait for Open Enrollment (November 1 - January 15 each year). For a few months without coverage, this might mean paying out of pocket for any care you need, hoping nothing big happens, and enrolling for January 1 coverage at the start of next year.

If you're in this gap, text me at (706) 988-1930 — I'll walk you through which of the three makes sense for your situation. There's no charge for the conversation.

Want Help Filing Your SEP Enrollment?

If you've had a Qualifying Life Event in the past 60 days and you're ready to enroll, the fastest path is:

Text me at (706) 988-1930 with the event type and date

I'll confirm the QLE qualifies and tell you what documentation to pull together

We'll get you enrolled through Georgia Access — usually within 24-48 hours

Free. Independent broker. No pressure.

I help self-employed Georgians, Atlanta families, and small business owners navigate this stuff every week. The 60-day clock doesn't care about your schedule — but I do, and I can move fast when you need to.

Justin Bishop is the founder of That Young Insurance Guy, an independent insurance brokerage in Atlanta, GA, licensed in 31 states. He writes the Health Coverage Chaos newsletter on LinkedIn.

This post is general education, not tax or legal advice. Marketplace platforms, carriers, and federal rules change.